Wall Street's Bet on Global Currencies Is Bloodied With the Dollar Soaring

Wall Street's Bet on Global Currencies Is Bloodied With the Dollar Soaring

(Bloomberg) -- Politics have foiled the best-laid plans of Wall Street’s currency strategists.

Turmoil in Turkey as well as strife between Italian leaders and the European Union have forced dollar bears to throw in the towel on bets that the rest of the world’s currencies would continue to play catch-up with the greenback in 2018. A continued flight to safety propelled the Bloomberg Dollar Spot Index to a 13-month high on Monday.

The advance prompted TD Securities to close the G10 foreign exchange convergence trade recommended in its 2018 outlook after losses of more than 4 percent. The team targeted 10 percent upside in going long the euro, Swedish krona, and New Zealand dollar relative to the U.S. and Swiss currencies. In early Tuesday trading, the Bloomberg Dollar Spot Index eased 0.2 percent.

“The soft patch in global growth and the emergence of Italian political tumult curtailed this thesis even though the ECB signaled the end of QE this year,” writes Mazen Issa, TD’s senior foreign-exchange strategist.

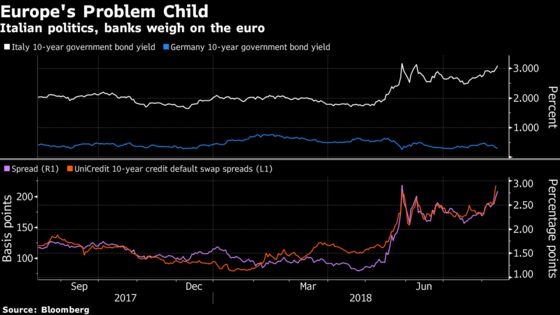

Italian Risk

A looming budget showdown between Italy’s governing coalition and the EU has dimmed demand for euro-denominated assets even as the region’s economic surprise index has narrowed the gap with its U.S. counterpart.

George Goncalves, head of Americas fixed-income strategy for Nomura Securities, flagged data showing that a combination of higher U.S. rates and political uncertainty catalyzed by Italy since May could be resulting in Japanese flows pivoting back to the U.S. and away from the EU.

UniCredit SpA’s exposure to Turkey could spark further risk-aversion -- and boost the dollar in its wake -- by serving to amplify a so-called sovereign doom loop for the embattled Italian lender, in which a government bond sell-off weighs on domestic financial institutions.

Intellectus Partners’ chief economist Ben Emons highlighted the connection between BTP-Bund spread and Italian bank credit default spreads as indicative of additional contagion from Turkey weighing on the euro bloc.

Declining share prices of Italian banks can be detrimental to capital positions. Should investors begin to fear the banks may need support from the government, a decline in the value of Italian bonds held by Italian banks could follow, thereby further crimping their capital cushions.

“Europe is obviously more vulnerable to shockwaves, economically and politically, than the U.S. is,” according to Kit Juckes, global fixed-income strategist at Societe Generale, who sees a risk that the euro could fall to 1.10 versus the dollar. “There’s nothing to stop the current slide continuing this week and beyond.”

Desynchronized Growth

Cracks in synchronized global output have also spurred a shift among Morgan Stanley strategists, erstwhile dollar bears across most currency pairs.

An enduring rift in economic momentum -- trade tensions, Chinese growth headwinds, tighter U.S. liquidity -- will add more fuel to the dollar over emerging-market currencies, according to Hans Redeker and his team at Morgan Stanley. However, they expect the euro, as well as the yen and Swiss franc, to hold up better.

“The economic decoupling story: The U.S. continues to absorb global capital, rendering capital-import-requiring EM economies vulnerable,” the analysts wrote in a Aug. 9 note.

It’s a shift in emphasis for the Wall Street bank, noted for its bearish dollar outlook, citing twin U.S. deficits among other factors. Now, a cross-asset spike in volatility is judged more likely than a return to the 2017’s international growth story.

The sting in the tail: U.S. assets can’t defy economic gravity overseas for too long thanks to the globalization of credit and equity cycles.

“The consensus suggests that the U.S. will stay immune to the rest of the world slowing down, ignoring the lessons provided by 2007 that market interlinkages are strong,” the strategists wrote. “The problem is that trade and financial integration has progressed for decades, making it increasingly difficult to insulate economies from foreign shocks.”

To contact the reporters on this story: Luke Kawa in New York at lkawa@bloomberg.net;Sid Verma in London at sverma100@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Andrew Dunn, Dave Liedtka

©2018 Bloomberg L.P.