Wall Street's Darkening Trade-War Gloom Means Tossing Old Advice

Wall Street is coming to terms with a trade war that is here to stay.

(Bloomberg) -- More than three weeks have passed since President Donald Trump’s tweets fanned the tariff fire. Now, Wall Street is coming to terms with a trade war that is here to stay.

“A trade war is now everyone’s base case,” said Peter Tchir, head of macro strategy at Academy Securities. “The reality of a trade war is finally sinking in. Little or no progress seems to be occurring. If anything, both sides seem to be digging in their heels.”

Strategists are getting granular with their advice. Prior calls were more broad-brushed, targeting asset classes or regions of the world to bet on or against. Now they’re more specific.

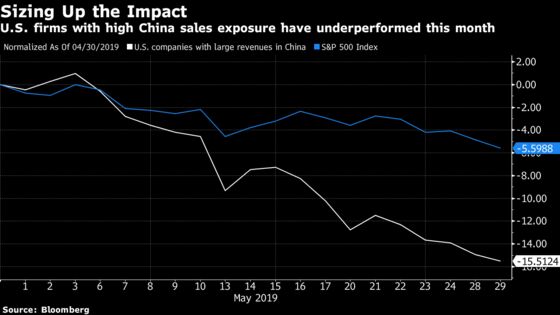

How much of a company’s sales come from China? What are executives saying on earnings calls? Which ones can pass through higher costs? They’re all questions being asked of U.S. firms -- and for good reason. While the S&P 500 Index has held up pretty well since the start of the month, selling pressure is getting stiffer, with major support levels under threat.

Here’s the latest advice:

Splitting Up by Sector

Over at RBC Capital Markets, the U.S. equity strategy team has been working to quantify trade risk sector by sector. After scouring earnings calls for commentary and surveying analysts, the clear losers under a worst-case China trade war scenario would be consumer discretionary, technology, industrials and materials, according to Lori Calvasina, the firm’s head of U.S. equity strategy.

Moving down the list, consumer staples and energy stocks carry risk, but less than those aforementioned. At the safety end of the spectrum, utilities, REITs, and communication services companies are the least exposed.

“Our favorite ways to add defensive exposure remain Consumer Staples (which we’ve been overweight) and Utilities (which we’ve been neutral on, but have highlighted as a tactical opportunity over the past few weeks),” Calvasina wrote in a note to clients. “For both, China tariff/trade war risks are lower than other sectors, valuations have looked more reasonable than other defensive sectors, and we see little risk from the 2020 elections (the market’s next big political test).”

Breaking Down by Name

Company analysts at RBC also highlighted the individual firms they believe to be most at risk from higher tariffs, taking into account both the outlook for margins and demand. Below is the list of stocks that analysts deemed most (and least) at risk in the industries where they see the trade war impact as “very negative.”

- Autos & Auto Parts: ADNT, VC, ALV, APTV, DLPH, BWA (AXL, MTOR)

- Chemicals: EMN, CE, HUN, OLN, WLK, CC, VNTR, DWDP, FMC (DOW)

- Coatings: SEE, OI (CCK, BLL, GPK)

- Department Stores & Specialty Softlines: AEO, URBN (VFC, LULU)

- Railroads: UNP (CSX, NSX)

Goldman Sachs Group Inc. has also been tracking U.S. companies with high revenue exposure to China. Global policy uncertainty stands near record highs, according to strategists at the firm, and “many aspects of the U.S.-China trade dispute are difficult to resolve.”

Here are some of the numbers:

- Only 1% of S&P 500 sales come explicitly from China

- Skyworks Solutions Inc., Wynn Resorts Ltd., Qualcomm Inc., Broadcom Inc., Qorvo Inc., and Micron Technology Inc. all get more than half of their revenue from China

After all, U.S. companies that receive at least 15% of their sales from the Asian nation have seen outsize pain this month -- down 10% more than the broader S&P 500.

Embrace Risk

Forget loading up on defensives and bond proxies. Instead, investors should use the next bout of market volatility to move further into risk. That’s the advice coming from Chris Harvey, head of equity strategy at Wells Fargo Securities. Any market stress should force the Federal Reserve to accommodate even further.

“We expect equities to move lower before they go higher and we don’t think you’ll need to wait too long. Our best guess is the equity markets will experience more stress or choppiness rather quickly (days/weeks) and risk will be for sale,” Harvey wrote to clients. “Looking forward, now is the time to figure out next steps and we don’t think its risk aversion. On the next leg down, we expect to shift around portfolio exposures and recommendations along risk and duration axes.”

--With assistance from Rita Nazareth and Randall Jensen.

To contact the reporter on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.