Wall Street Profit Optimism Requires a Crazy-Good End to 2019

Wall Street Profit Optimism Requires a Crazy-Good End to 2019

(Bloomberg) -- The fourth quarter failed Wall Street’s equity bulls in 2018. This year, strategists are counting on earnings growth in the last three months of the year to save them.

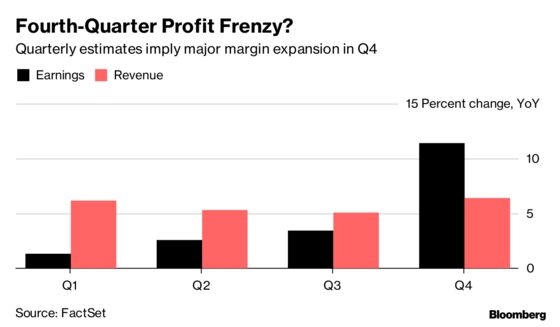

An examination of analysts’ profit forecasts for S&P 500 Index members reveals a major outlier in expected results at year-end, according to DataTrek research co-founder Nicholas Colas. Estimates call for profit growth of about 6 percent in 2019, but the figure is skewed by a fourth quarter that’s expected to deliver double-digit annual growth in earnings -- the lone period of the year in which there’s a projected profitability pick-up.

“This whole-year 2019 estimate is based on a hockey-stick increase in both earnings growth and margin leverage in Q3 and especially in Q4,’’ Colas wrote, citing data from FactSet.

Does it matter when earnings growth comes? Probably not. The issue is the believability of the forecasts. Logically, it’s easier to get next quarter right than one nine months hence. But an investor banking on analyst calls for solid earnings growth in 2019 is dependent on the soundness of their most distant projections.

Estimates compiled by Bloomberg also indicate that revenue growth is expected to outpace earnings growth in each of the first three quarters of 2019, but trail for the year as a whole.

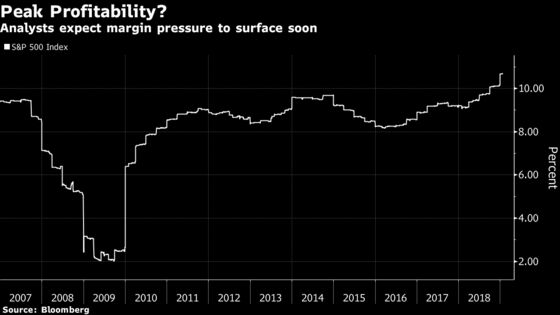

This implied reduction in profit margins in the first three quarters, which comes after years of expansion, “is a typical late-cycle problem as labor/input costs (plus tariffs/slowing global growth, in today’s world) take their toll,’’ Colas writes.

Colas’ observation feeds into one of the hottest debates on Wall Street right now: the extent to which expected earnings will come under the knife as companies deliver their fourth-quarter results and issue guidance for the year ahead. So far, full-year estimates have been trimmed by 1.8 percent since the start of the year to $168.75. Profit forecasts for energy companies have been cut by the most so far in 2019, a delayed reaction to the prior plunge in oil prices, followed by the utilities and technology sectors.

HSBC’s Max Kettner thinks the end of dollar strength might prompt an end to negative earnings revisions for global equities. Conversely, Morgan Stanley’s Mike Wilson sees the vast breadth of forecast cuts across sectors as an indication that an earnings recession is on the horizon.

Put Colas closer to Wilson’s camp, as he calls the prospect of contracting earnings in 2019 a “distinct possibility.”

From mid-October to mid-January, first-half profit forecasts have been slashed by 4.5 percent, compared to an average year-ahead trim of 2.5 percent over the past 15 years, he notes, a sign that stalled earnings momentum is top-of-mind across Wall Street.

This year’s “estimates are still too optimistic unless we get a speedy trade resolution that drives a re-acceleration in global economic growth, and we would expect them to continue to decline as Q4 earnings season unfolds in the coming weeks,’’ he wrote. “While we remain generally positive on U.S. stocks, we expect more churn ahead as markets wrestle with an earnings recession offset by hopes for a trade resolution.’’

--With assistance from Reade Pickert.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Brendan Walsh, Randall Jensen

©2019 Bloomberg L.P.