Wall Street Picks the Next Domino to Fall in Trade-War Rout

Wall Street Picks the Next Domino to Fall in Trade-War Rout

(Bloomberg) -- Wall Street analysts have picked the next domino that they think will fall in financial markets as an escalation of the trade war continues to upend global equities.

Strategists at Weeden & Co., Cantor Fitzgerald & Co. and Macro Risk Advisors are taking one more step down the risk ladder and turning bearish on a junk-bond exchange-traded fund. High-yield debt may come under more stress as focus turns to the negative impacts the newest clash over cross-border commerce will have on American activity, according to analysts. And options that offer exposure to downside are cheaper in junk bonds than U.S. equities.

Investors are prepping for the worst-case scenario in trade -- a derailment of talks -- after the Trump Administration jacked up tariffs on Chinese goods and the Asian nation said it would retaliate, helping to push this week’s slide in equities to around 3%, the biggest decline since December.

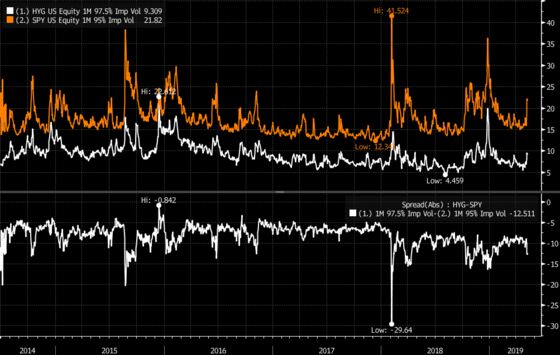

“Equity volatility is once again highly dislocated versus high-yield credit spreads,’’ writes Peter Cecchini, global chief market strategist at Cantor Fitzgerald, who estimates that S&P 500 Index’s implied fluctuations are two standard deviations rich relative to their typical spread to swings in the junk space.

Thus, long-volatility strategies on the iShares iBoxx High Yield Corporate Bond ETF are attractive as “a way to hedge high-yield exposure or even as an outright bet to play the reversion of credit spreads to equity volatility.’’

On Thursday, Cecchini recommended a put spread trade that breaks even if the junk bond product falls 2.7% from its latest close by June 21, and has a maximum payout of nearly 10 times the premium paid should HYG fall 7% over that span.

Bank of America strategists said poor market conditions for individual corporate bonds can lead to more acute stress for assets that are more frequently traded, specifically, junk-linked exchange-traded funds.

“Times of significant market stress are associated with above-average discounts in ETFs, ranging from 0.15pts in late 2015 to 0.25pts in late 2018,’’ wrote Oleg Melentyev, head of U.S. credit strategy at Bank of America Merrill Lynch.

‘Catch Up’

Equity volatility has been more sensitive to the retreat in U.S. stocks than it was in the fourth quarter. In October, the S&P 500 was nearly 5% off record highs the first time the VIX cracked 20. This time, losses reach a little more than 2% before that threshold was breached. And it wasn’t until early December that the implied one-month correlation among index constituents hit 0.49. It only took two sessions into the current pull back until traders were already similarly scared about the prospects of everything tumbling at the same time.

“If trade tensions persist, high yield will ‘catch up’ with equities,’’ said Michael Purves, chief global strategist at Weeden & Co. In the fourth quarter, the pick-up in credit volatility and spread widening were relatively slow to occur because economic fundamentals remained fairly robust, he wrote in an note, but “as volatility persisted, it was only a matter of time until pan-asset de-risking caught up with the dramatic de-risking in equities.’’

No Dry Spell

For most of the fourth quarter, demand for options that benefited from a 5% retreat in the S&P 500 relative to a 2.5% in the junk-bond product was even more extreme than it is now, a dynamic which may pose a risk to bets on a reversion in volatility between the two asset classes.

The high-yield primary market isn’t looking anything like it did in December, which was the first month without a deal pricing since November 2008. This has been the busiest week since September 2017, with around around $12 billion in issuance. While companies may be worried that a window is closing, new issues have remained oversubscribed with mixed results on pricing.

This isn’t the first time China-linked scares have helped narrow the spread between high-yield debt and equity relative volatility. Downside in the junk bond fund was relatively bid compared with S&P 500 puts during the fourth quarter of 2015 and first quarter of 2016. Back then, there where lingering fears of a hard landing in China following the shock devaluation of its currency, soft oil prices, and the initiation of the Federal Reserve’s tightening cycle combined to roil markets.

Vinay Viswanathan, a derivatives strategist at Macro Risk Advisors, made one of the first bearish calls on HYG Wednesday, writing that “the potential impact to the credit market from concrete tariffs on Chinese imports announced this Friday’’ made short-dated puts attractive.

--With assistance from Cecile Gutscher, Yakob Peterseil and Gowri Gurumurthy.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Randall Jensen, Rita Nazareth

©2019 Bloomberg L.P.