Navigating the Recovery Trade Is Getting a Whole Lot Trickier

Wall Street More Split on Markets as Easy Recovery Bets Run Out

(Bloomberg) -- The easy part of the recovery trade may be over.

Global markets look to have reached a turning point in their rebound from pandemic lows. In previous phases there was an unusual cohesion of views around havens like gold and the stay-at-home trade, followed by bets on a value rotation and steepening yield curve. What comes next is much less clear.

Take the debate between value and growth. Societe Generale SA and JPMorgan Chase & Co. say value shares will keep outperforming at this stage of the market cycle. Prudential Financial Inc. and AlphaOmega Advisors LLC say the sector is due for a pullback. There is just as much as divergence over the fate of the dollar, and on the next move in Treasuries.

Much of the growing uncertainty stems from the pivotal point reached in the fight against the coronavirus. The rollout of vaccines is raising the prospect the pandemic will eventually be contained, but the fact that cases are rising in many countries still leaves plenty of room for things to go wrong. At the same time, there is concern the recovery will peter out once stimulus is withdrawn.

“The pent up demand will likely fuel the recovery of cyclical sectors that have been hurt the most by the pandemic, but that could prove be short-lived as stimulus fades and investors have to look beyond the recovery to the new post-pandemic world,” said Charlie Ripley, senior investment strategist at Allianz Investment Management based near Minneapolis. “The landscape could become difficult to navigate.”

U.S. President Joe Biden’s proposed $2.25 trillion infrastructure package may throw another wild card into the system, depending on exactly what spending and tax increases end up being implemented.

Value Versus Growth

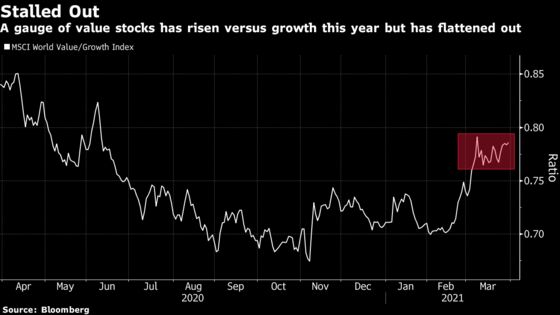

By far the biggest debate among strategists is over the respective merits of value and growth. Value has been a tearaway winner this year as the recovery has gathered pace, with the Russell 1000 Value Index rising 11% since the end of 2020, while the same provider’s Growth Index has gained less than 1%. In recent weeks though this outperformance has shown signs of stalling.

SocGen sees further gains in value as just a matter of time. “Value (and more generally cyclicals) still command significant valuation advantage to the rest of the market,” said Solomon Tadesse, head of North American equity quant research in New York. “Distressed out-of-favor assets tend to gain from potential multiple expansion at this point of the market cycle.”

JPMorgan Chase is also staying positive, arguing value will benefit from rising interest rates and a steeper yield curve.

“Value remains an outsized beneficiary of reopening, which is still in its early stages,” strategists led by Dubravko Lakos-Bujas in New York wrote in a note Friday. Still, “while we believe value and reopening trade still has room for upside, we would emphasize focusing on higher quality companies with greater staying power, for example retail and energy.”

Prudential Financial has a completely different view.

The reflation trade is “frothy” and “waiting for a pullback is prudent,” said Quincy Krosby, chief market strategist at the insurer in Newark, New Jersey. Stocks have moved quickly to price in a potential U.S. infrastructure package and any signs of difficulty in getting the legislation passed could instigate a selloff, she said, adding that such a dip may offer a good entry point.

AlphaOmega Advisors is also losing its enthusiasm for value shares.

“It’s time to take money off the table now,” said Peter Cecchini, founder and chief strategist of the independent research and consulting firm in New York. “Perhaps the latest round of stimulus will keep the cyclicals trade alive a bit longer, but I just don’t see the cycle turning for good as we might expect after a normal recession,” he wrote in a research note Friday. “Staying tactical and nimble seems prudent.”

Treasury Bulls and Bears

The uncertain global outlook is also becoming evident in the Treasury market.

JPMorgan Asset Management is among the bears, saying the “proper place” for U.S. 10-year note yields to settle is around 2% following the recent bond-market volatility. This is likely to take place after some consolidation in the area of 1.5% to 1.75% around quarter-end, according to Bob Michele, chief investment officer at the money manager in New York.

HSBC Holdings Plc has a different take. Treasury 10-year yields will fall to 1% by year-end as an economic recovery based on stimulus won’t be enough to set off a lasting return of price pressures, London-based head of fixed income research Steven Major said last week. A proper inflationary shock would need pent-up consumer demand to boost economic output for “many years to come,” he said.

The benchmark 10-year yield rose to a 14-month high of 1.77% on Tuesday before dipping back.

Dollar Dispute

No less of a divergence can be seen over the burgeoning rebound in the dollar.

The currency’s uptick won’t last as it’s just a “countertrend rally within a broader bear market,” Morgan Stanley Wealth Management strategists led by Lisa Shalett in New York wrote in a research note Monday. “The reasons for a bear market remain: surging fiscal and trade deficits, growing government debt issuance, rising probabilities of anti-dollar regulatory and tax policies, ultra-dovish accommodation by the Fed, and increasing competition for foreign currency reserves.”

American Century Investments is bullish on the greenback, citing rising Treasury yields and a superior economic-growth outlook.

“What matters is the growth differentials -- and the growth differentials this year are in favor of the U.S.,” said Abdelak Adjriou, a portfolio manager at the money manager in London. He turned bullish on the dollar earlier this year when 10-year yields climbed above 1%, he said.

‘Massive Run’

The simple fact that risk assets have had a major rally is another reason for doubts to set in.

“Any time you’ve had this massive run in risk assets -- crude, copper, Russell 2000, currency trades –- it becomes harder because positioning gets one-sided,” said Michael Purves, chief executive officer at Tallbacken Capital Advisors LLC in New York. “In the beginning it’s just easier -- the risk/return is better. Once they become more obvious trades, they become not-as-good trades.”

©2021 Bloomberg L.P.