Wall Street Is Rethinking the Treasury Threat to Big Tech Stocks

Wall Street Is Rethinking the Treasury Threat to Big Tech Stocks

(Bloomberg) -- Don’t fear Treasury yields killing off the stock market’s golden goose just yet.

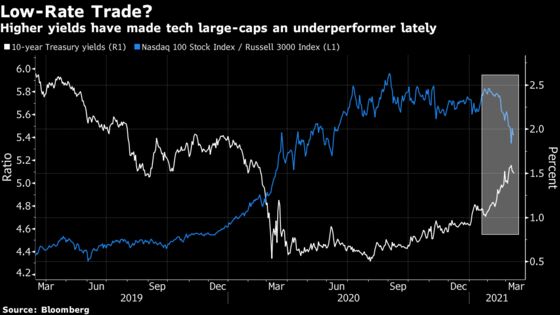

As the Nasdaq 100 Index recovers from a $1.5 trillion rout, there’s good reason to think technology shares can defy machinations in U.S. bonds.

Studies from Deutsche Bank AG and Goldman Sachs Group Inc. show the world’s biggest equity sector has a fickle relationship with Treasuries, if it has one at all. Quant powerhouse AQR Capital Management has found little evidence that yields drive how expensive megacaps trade relative to their cheaper counterparts.

And of course, secular economic trends have been powering the likes of Facebook Inc. and Amazon.com Inc. for years now -- when benchmark rates were far higher than current levels.

All that makes the Treasury-stock link more complex than it seems.

Put another way, while the recent Treasury selloff has pummeled Big Tech, that doesn’t mean bonds are a natural foe for a sector hitched to secular trends from 5G to automation.

“Many tech companies will continue to benefit for many years from very strong themes that will result in outsized earnings growth,” said Terry Ewing, head of equities at Mediolanum International Funds, which oversees about $54 billion. “The dilemma for portfolio managers running a balanced mandate is that actually the de-rating we’ve seen in growth stocks has put them at a much more attractive level.”

Ewing’s funds began offloading a handful of tech stocks for cyclical names from the third quarter, just as rising expectations for an economic re-opening pushed yields higher in the world’s biggest bond market.

As the U.S. yield curve steepened last month, $1.5 trillion of value was wiped off tech shares, while assets deemed less sensitive to duration risk like value stocks -- banks, oil drillers and commodity producers -- surged.

The Nasdaq 100 jumped nearly 2% on Thursday morning in New York, as 10-year Treasury yields traded little changed around 1.5%.

Quant Perspective

From the perspective of quants who dissect equities by their factors, there are a few ways to explain the last month’s rotation.

Technology companies are typically dubbed growth stocks thanks to their strong expected profit expansion, often far into the future. That’s in contrast to value shares, which trade with lower multiples due to their riskier businesses.

When rates fall, economic growth is typically muted. That makes a company like Netflix Inc. look like a a safer bet since it’s riding the secular trend of streaming rather than ups and downs of the business cycle. Meanwhile the likes of Exxon Mobil Corp., tied to oil demand, look riskier.

In the post-crisis era of monetary easing, that’s how the valuation dynamic played out: Netflix’s long-term earnings were discounted at lower rates -- making it more expensive.

Now, opposing forces are in play. Rising yields are making the near-term cash flows of cheaper equities like Exxon Mobil more attractive.

“Sooner or later we will see pretty decent economic growth,” said Georg Elsaesser, a quant portfolio manager at Invesco. “I would be more than surprised if that wouldn’t be favorable for high-risk factors like value.”

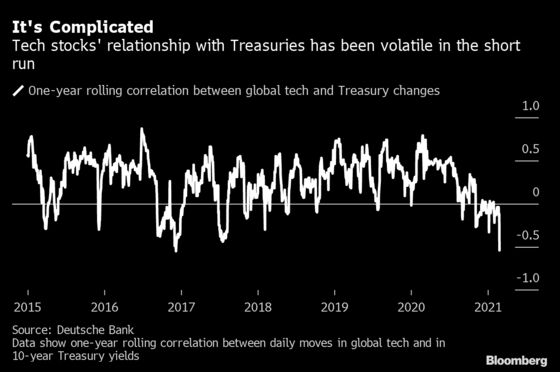

Yet all these relationships are volatile -- and have far less explanatory power than commonly asserted.

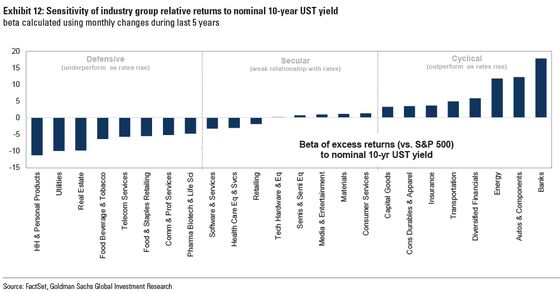

Interest-rate changes only explain 19% of the returns posted by the growth factor versus value since 2018, Goldman Sachs strategists wrote in a note last month. That compares with 54% for cyclicals versus defensive.

In other words, industry-specific trends, not bonds, seem to be driving this tech-heavy part of the market.

Similarly Deutsche Bank’s quants find a zero beta, or sensitivity, between bonds and tech since 2015. In contrast, financials and energy had the most positive links with yields, and utilities and real estate the most negative.

According to Andreas Farmakas, a quantitative strategist at Deutsche Bank, this shows how the tech sector and Treasuries lack a direct and consistent link. In fact, these stocks in the past often rose with rates, with the latter seen as a sign of economic strength that could benefit corporate earnings.

That’s not to say there isn’t reason to fret recent co-movements.

“Given the ties between technology, the overbought Covid trade and ultimately equity indices -- they take up a large chunk –- the correlation flipped,” Farmakas said.

In other words, bonds have lately turned from friend to foe -- and that’s why quants like Invesco’s Elsaesser are so reluctant to time markets.

For its part, AQR last year called the link between interest rates and value -- which involves a bet against growth -- “suspect” since it varies greatly depending on the period, the markets and measurements studied.

All this suggests that once the initial reflation frenzy settles, there’s no reason to fear bond yields will necessarily doom the tech trade. In fact Ewing at Mediolanum is eyeing some bargains in the months ahead.

“Somewhere along the second-half of this year going into next year it’ll be prudent for investors to start considering moving to higher-quality names rather than cyclical recovery,” he said.

©2021 Bloomberg L.P.