Battered and Bruised, Wall Street Makes Peace With Volatility

Wall Street Is Making Peace With the New Era of Stock Volatility

(Bloomberg) -- Wall Street is making peace with the new normal of higher volatility as stocks careen between agonizing sell-offs and sudden rallies.

After the gut-wrenching $2.5 trillion wipeout in the S&P 500 since early October, traders are resting at relative ease as they prep for market bumps down the road.

A measure of expected changes in the Cboe Volatility Index is sitting near its lowest level since 2016 versus the underlying fear gauge, while demand to hedge tail risks is at multi-year lows.

Markets are “beginning to accept a shift in the volatility regime back to more historically average levels,” said Patrick Hennessy, head trader at IPS Strategic Capital in Denver, Colorado.

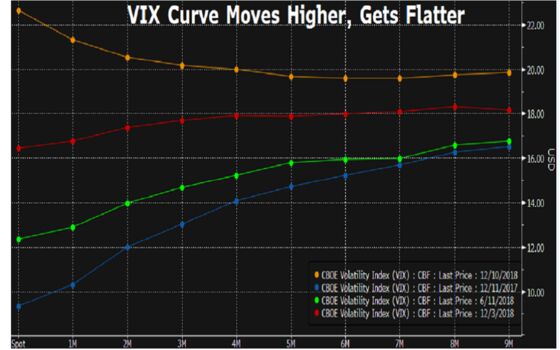

‘Flat as a Pancake’

Even as all manner of fears -- a U.S. recession, a credit crisis, a peak in earnings -- stalk the aging bull market, they’re flashing a bullish signal that the VIX will stay range-bound.

Take the price of futures contracts on the VIX, which allow investors to buy or sell the index at a given time. While futures traders have been paying a premium for nearer-dated contracts -- a sign of stress that typically accompanies market spikes -- the back half of the VIX curve is “flat as a pancake,” said Yannis Couletsis, director at Credence Capital Management Ltd.

The difference in the price between contracts on expected price swings in U.S. stocks in nine months time versus four is a mere seven cents -- far tighter than the average spread of $1.53 over the past five years.

Put simply, market players are wagering the gauge will remain higher for longer -- but they also reckon it will be little changed down the line.

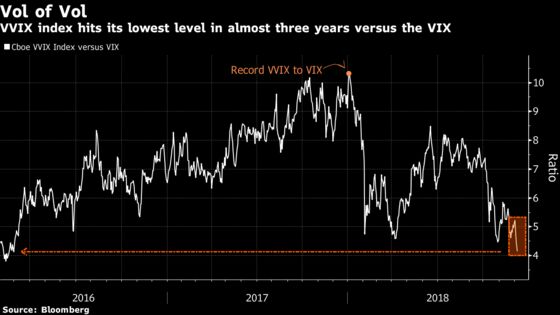

Vol of Vol

Another sign investors aren’t expecting a fresh breakout in price moves from current levels: A measure of expected volatility of the VIX has hit its lowest level in nearly three years versus the referenced gauge.

Cboe’s VVIX reflects the price of options mostly used for tail protection, so the low reading underscores the lack of demand for protective hedges even after bulls get steamrolled after weeks of disruptive selling.

In other words, derivative traders aren’t piling into options that would pay off handsomely in the grip of an equity storm -- suggesting they are holding their nerve, or at least betting that the worst of the turbulence is over.

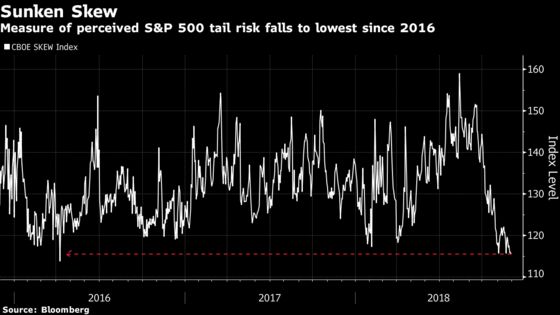

Call Mania

Lack of demand for protective hedges is also showing up in CBOE’s SKEW Index, which purports to measure expectations of a tail event. The measure hit its lowest in more than two years Friday.

The gauge is calculated by comparing the implied volatility for put options on the S&P 500 Index relative to call contracts. Put another way, speculators are effectively crowding out hedgers by the most since April 2016.

The low reading suggests markets have “shifted into a higher volatility regime,” according to Wells Fargo equity derivatives strategist Pravit Chintawongvanich. One way of thinking about it is that it’s cheaper to hedge a spike in equity volatility if current levels have edged up.

“If vol has reset higher, skew doesn’t necessarily need to be as high,” he wrote in a note.

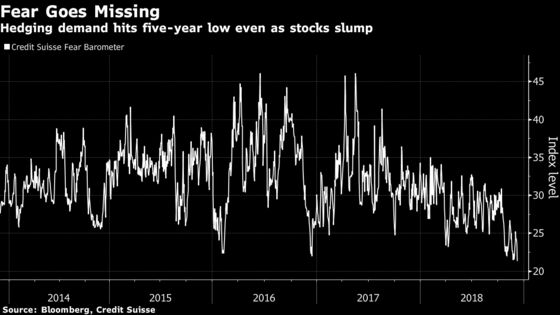

Credit Suisse’s barometer of fear also shows muted demand for protective hedges relative to bullish options.

The index, which tracks the cost of downside three-month protection relative to upside options, is at its lowest level since May 2013. The higher the level, the greater the fear.

In the complex world of options trading, no indicator is clear-cut. While signals suggesting little panic on the horizon provide bulls with ammo, there’s a more pessimistic read.

Lack of demand for protection may suggest investors are merely dumping stocks while they buy calls for fear of missing out on a Christmas rally, according to Chintawongvanich. “Managers may be choosing to de-risk by selling equities rather than buying additional hedges,” he wrote in an email.

While that may suggest investors aren’t all at ease with the prospect of higher stock swings, they’re adjusting however grudgingly, according to Hennessy at IPS Strategic Capital.

“I think we’re finally seeing acceptance of a higher VIX regime going forward,” he said.

--With assistance from Cecile Vannucci.

To contact the reporters on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net;Dani Burger in London at dburger7@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.