Volatility Markets Flash Warning Sign That Preceded Prior Routs

Volatility Markets Flash Warning Sign That Preceded Prior Routs

(Bloomberg) -- Volatility markets are signaling elevated risks for equities, flashing a warning sign that portended some of the major market meltdowns in recent memory.

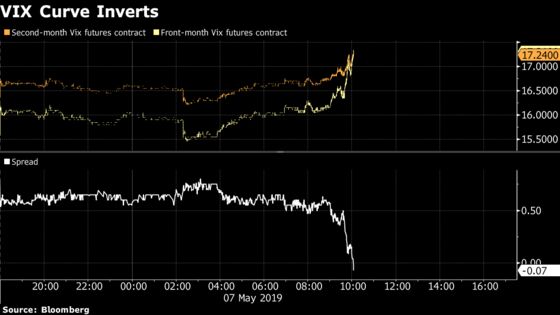

The front-month VIX futures curve traded above the second-month future shortly after 10 a.m. New York Time as the retreat in the S&P 500 Index intensified. The inversion was spurred by a second wave of selling following comments from U.S. Trade Representative Robert Lighthizer late Monday, when he affirmed that President Donald Trump’s vow that the U.S. would hike tariffs on China wasn’t empty. Those comments delivered a blow to traders who hoped the president’s weekend tweets were mere posturing.

The market turmoil seen this week comes after a long period of calm and steady gains for U.S. equities, spurred by investors’ conviction that a trade deal with China was inevitable and the Federal Reserve might even move toward easing rates in a bid to boost price pressures. Volatility fell by almost half this year through the end of last week as the S&P 500 Index surged 18 percent.

VIX futures are linked to the Cboe Volatility Index, which tracks the 30-day implied volatility for the S&P 500 Index and is often called Wall Street’s “fear gauge.” The underlying volatility gauge surged to 19.3 Tuesday, touching the highest since October, as the benchmark U.S. equity measure tumbled 1.4 percent for the biggest sell-off in six weeks.

Typically, the VIX futures curve is upward-sloping (in so-called contango) because the outlook for U.S. equities is more uncertain over the long run than the short run. When the curve is downward-sloping (in backwardation), it shows investors are acutely concerned with the near-term risks to U.S. equities.

“The fact that inversion occurred with futures expiration still over two weeks away gives us confidence that this move isn’t just noise (the front of the curve can be volatile near futures expiration) but is actually showing a demand for protection in the market,” said Vinay Viswanathan, an equity derivatives strategist at Macro Risk Advisors.

The curve closed in inverted territory on Feb. 2, 2018, following a non-farm payrolls report that suggested inflationary pressures emanating from the labor market were heating up. The next session, the VIX posted a record jump, which felled several exchange-traded products that let investors bet on enduring market calm.

It also inverted in the fourth quarter days after Federal Reserve Chair Jerome Powell indicated that rates were a “long way” from neutral, remarks which helped accelerate the drubbing in U.S. equities that sent the S&P 500 Index to the edge of a bear market.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Brendan Walsh, Randall Jensen

©2019 Bloomberg L.P.