Market Braced for ‘Too Close to Call’ Georgia Runoffs

Volatility Market Braced for ‘Too Close to Call’ Georgia Runoffs

(Bloomberg) -- Investors aren’t quite ready to put this chaotic year behind them just yet. There’s one more lingering risk event to fret over: the final races of the 2020 elections that have spilled into next year.

While not as pronounced as the hedging seen around Election Day last month, options and volatility futures do signal elevated concern over potential market turbulence resulting from the results of the Jan. 5 runoff races in Georgia that will determine whether Republicans maintain control of the Senate.

Prior to the November vote, many considered a Democratic sweep of the elections to be among the most bullish possible outcomes for U.S. equities. Since then, however, the market has shown it’s grown comfortable with a potential continued split control of the government -- a backdrop that historically has produced strong returns.

“There’s no doubt, if you go from red to blue, you’ve got to price in something that looks less favorable because of markets liking gridlock, markets liking status quo,” said Phil Camporeale, managing director of multi-asset solutions for JPMorgan Asset Management.

The focus on the runoff -- and demand for hedges to protect against turbulence in its aftermath -- is centered on uncertainty over how exactly investors should position themselves ahead of a Joe Biden presidency. He needs Democratic control of the Senate to execute on an agenda that would boost green-energy companies at the expense of fossil-fuel producers, while likely leading to more economic relief packages and infrastructure spending. Yet it could also help him raise the corporate tax rate and heighten regulatory scrutiny.

“It is impossible to overstate how important these elections are for the size, scale, and speed of 2021 fiscal, tax, and regulatory policy,” Cowen analyst Chris Krueger wrote in a note on Dec. 21.

Hedges in Place

There are potential winners and losers in both scenarios and it’s debatable which would be a better scenario for the overall stock market over the longer term. But traders appear to be hedging against volatility that could erupt in the short-term if the Georgia results cause investors to pile into the perceived beneficiaries of the outcome and dump the perceived losers.

The hedging likely also reflects concern that even small surprises could create turbulence in an equity market that needs the general public to keep on investing after a spectacular run. The S&P 500 has surged 65% from its low in March, with an assortment of valuation metrics at their highest in a decade or more.

“The idea that fiscal policy and public buying could matter more than earnings and revenues -- sounds a lot like 2020, doesn’t it? -- is instinctively uncomfortable and supports above normal volatility persisting,” Julian Emanuel, equity strategist at brokerage BTIG, wrote in a recent note.

The runoffs in Georgia were triggered after no candidates for the state’s two Senate seats clinched a majority of the vote. Republican David Perdue is running for re-election against Jon Ossoff, while Senator Kelly Loeffler faces Democrat Raphael Warnock. Polls show a tight contest between the Republican and Democratic contenders, while the PredictIt betting market shows a small advantage to the Republicans. President Donald Trump’s last-minute demand for bigger payments to Americans as part of a Covid-19 relief package is also a wildcard that may affect the vote.

The closeness of the races has kept investors from getting too confident about what to expect in the early part of a Biden administration. If Democrats win both races, it gives them control of the Senate with help of a tie-breaking votes from Vice President-elect Kamala Harris. (Two independent senators caucus with the Democrats.)

“We view both elections as too close to call,” said Tom Hainlin, strategist at U.S. Bank Wealth Management’s Ascent Private Wealth Group, adding that “some short-term market volatility is possible” after the vote if Democrats take both seats.

Strategists at Evercore ISI say the Cboe Volatility Index’s futures curve remains “notably steep” due to the Georgia events, similar to the situation heading into the November races.

Meanwhile, skew in S&P 500’s one-month puts, or a measure of cost in the bearish options, stood at the 92th percentile of a historic range, according to data compiled by Nomura Securities. “Focus turns to protection after one hell of a run, and ahead of the macro-regime-change risk from the nearing Georgia Senate run-off,” Charlie McElligott, a cross-asset strategist at Nomura, wrote in a recent note to clients.

Many in the market assume the Republican candidates will keep both seats, said Ryan Detrick, chief market strategist for LPL Financial, so any surprises “could upset the apple cart.”

Upset Things

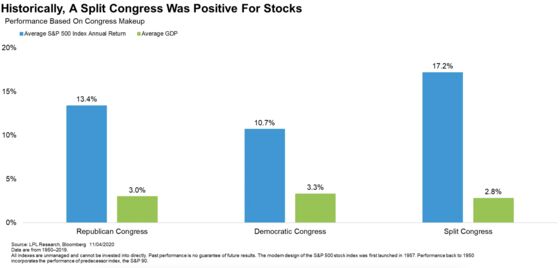

Research from LPL has found that a divided Congress has historically been good for the stock market -- over the last seven decades, the S&P 500 has returned an average of 17.2% annually when power was split between the two parties. That compares with an advance of 10.7% when Democrats were in charge and 13.4% with Republicans at the helm of both chambers.

{kind=link}

Activity is also heating up in the Treasury options market, highlighted by a contrarian wager that emerged late Monday. The bet was against the potential for aggressive fiscal stimulus to spur a rout in the long end of the bond market, and it stands to pay out if any climb in yields is capped around 10 basis points from current levels for roughly the next month.The wager leans against a theme that’s been gaining momentum in Treasury options -- that the Georgia selloff could trigger a sharp selloff in Treasuries.

Treasury Options Market Springs to Life as Georgia Runoffs Near

To be sure, many on Wall Street don’t foresee the Georgia races as too much of a game changer. A slim Senate majority for Democrats might not necessarily mean an immediate ushering in of new policies, including a revamp of tax rates, according to Art Hogan, chief market strategist at National Securities Corp.

“I just don’t think it’s playing into this idea of, ‘Oh my god, higher corporate taxes immediately and grandiose changes.’ I think it’s much more a centrist mentality that we might have some gradual changes,” said Hogan by phone. “The market narrative shifted pretty quickly, too, post the election, saying, ‘Hey, wait a minute, we didn’t get the blue wave but we’ve got a new president and with that comes probably a calmer presence around international relations and tariffs and trade and more normalization.’ I think the market has settled into that concept.”

©2020 Bloomberg L.P.