Volatility Hedge Funds Hit by Market Woes in All Directions

Volatility Hedge Funds Hit by Market Horrors in All Directions

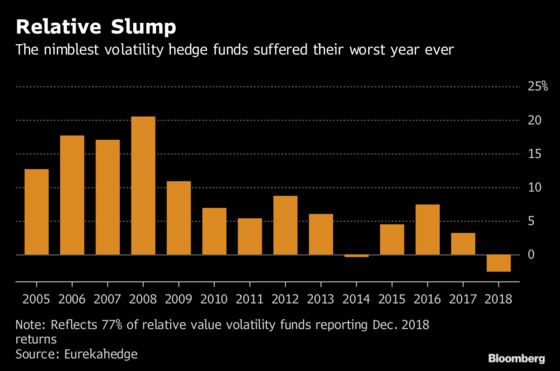

(Bloomberg) -- Some of the nimblest hedge-funds that trade volatility are hoping history doesn’t repeat after suffering their worst year in over a decade.

Managers famed for posting steady profits from relative-value strategies, which shuffle between long- and short-volatility bets, lost a record 2.5 percent in 2018, according to Cboe Eurekahedge data.

You’d think funds that profit from swings would thrive from crazed markets. But these rarefied players were sunk instead by erratic moves in implied volatility and an outsized spike in U.S. equity angst versus the rest of the world.

The question now is whether these obstacles will continue to confound market-neutral trades.

“Higher volatility is positive, but erratic spikes can prove difficult to navigate for volatility-sensitive strategies,” strategists Karim Cherif and Georg Weidlich at UBS Global Wealth Management wrote in a report.

In December, Wall Street’s “fear gauge” posted relatively subdued readings on average despite the worst end-of-the-year slump for U.S. stocks since the Great Depression. February, by contrast, proved hugely disruptive when the VIX staged a violent spike, roiling traders of all stripes.

Risky Business

Money managers are hoping the market won’t prove similarly capricious in the months ahead.

Now, the question is whether the VIX will clock in at relatively muted levels if stocks take a downturn, a phenomenon that hit arbitrage strategies at the tail end of last year.

December’s implied volatility proved too low for traders selling S&P 500 puts while buying VIX futures, according to Grant Melson at Houndstooth Capital Management in Austin, Texas. Those wagering that the equity contracts were over-priced relative to futures on the fear gauge struggled.

“The S&P was plummeting but VIX futures were not pulling their weight to protect the other component of the trade,” he said.

Right now, a potentially uneasy calm has returned to the VIX, defying the $5 trillion stock turmoil last month. Easing correlations and muted demand for downside hedges are helping to offset fears over the growth outlook, intransigence in Washington and trade policy. Since Christmas Eve, the gauge has fallen in 12 out of 16 sessions.

If equity markets do blow up again, Melson expects it will be business as usual. “We’d be surprised if vol continues to be suppressed relative to equity markets,” he said.

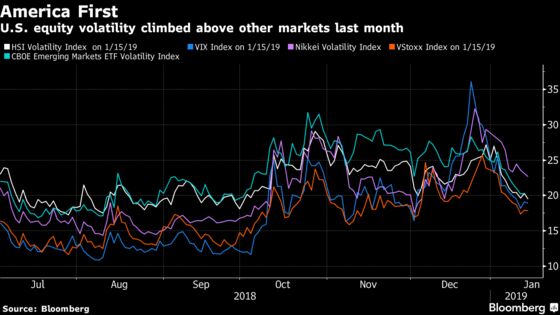

‘America First’

Yet another dynamic that’s vexed relative-value strategies: American stocks are serving as the epicenter for developed-market angst.

With the U.S. business cycle long in the tooth and faith in momentum equities unraveling, hedge funds have been bruised by outsized S&P swings versus overseas benchmarks.

A popular trade for relative value funds is “continuously purchasing volatility -- mostly to the downside -- in Asia and selling volatility in the U.S.,” according to Tobias Hekster of True Partner Capital, whose vol fund gained an estimated 2 percent last month.

“With U.S. movement significant compared to other markets, the longs against a U.S. short simply would not sufficiently contribute to make up for that,” he said.

Call it a perfect storm. As U.S. equities flashed recession fears last year, traders that bet on interest-rate, currency and credit gyrations to rise in sympathy were also largely left disappointed.

“The consensus, concentrated short position in S&P volatility got hit and many popular longs -- e.g. rates volatility -- didn’t move,” said Benn Eifert, chief investment officer of QVR Advisors, an investment adviser specializing in such strategies.

With equity swings expected to remain elevated, perhaps the best strategy will prove the simplest: Funds that go long volatility notched a gain in 2018 after three years in the red.

--With assistance from Justina Lee.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Todd White

©2019 Bloomberg L.P.