Volatility Crushed Like It's 2009 as ‘Pale Green Lights’ Flash

Volatility Crushed Like It's 2009 as ‘Pale Green Lights’ Flash

(Bloomberg) -- On Christmas, U.S. markets were given a gift as calm showed the first signs of overcoming panic.

During December’s market mayhem, the daylight hours were traders’ worst nightmares. On average, the S&P 500 Index would slump marginally overnight, but tumble 1.1 percent from the U.S. open to the close of regular trading hours. That changed after Dec. 25.

A breakdown of this pattern since then points to renewed risk appetite. Stocks are still averaging a slightly larger drop overnight, but the benchmark index is climbing 0.8 percent on average from the open until the closing bell sounds.

“You start with the market weaker and you ended up rallying through the day, grinding higher in sort of a 2017 deja vu,’’ said Mayank Seksaria, chief macro strategist at Macro Risk Advisors, in an interview on Bloomberg TV late Friday.

Despite the S&P 500’s inability to break through 2,600, the healthy tape is “a pretty good sign, and more important personally, than certain levels,’’ he added.

The resilience is best seen in the Cboe Volatility Index, a measure of the 30-day implied volatility of U.S. stocks that’s also known as the VIX or “fear gauge.” The VIX has fallen from open-to-close for 13 straight sessions, matching the April 2009 record based on data going back to 1992.

“While that may sound pretty bullish, the statistics on similar spread compressions are not necessarily positive in the very near term,” caution analysts at Bespoke Investment Group, noting that median one-week forward S&P 500 return after the VIX falls for at least 10 consecutive sessions has been negative.

Clearing Hurdles

The stretch has been marked by a renewed ability to shake off potentially negative catalysts.

During the first trading session of 2019, traders took in stride poor manufacturing data, especially from China, with stocks posting a tiny gain. Likewise, damage associated with weak performance by retailers like Macy’s and Kohl’s has faded and weak outlooks from airlines like American Airlines and Delta Air didn’t linger for long. The only session the S&P 500 has fallen from open to close this year was on the heels of Apple’s first negative revenue revision in nearly two decades and the blowup of leveraged yen sellers -- and still the VIX fell from 3:15 a.m. New York time until 4:15 p.m. that day.

“’Because the December drop was so relentless I think VIX was initially resistant to the idea that the market would move up in a straight line and kept waiting for another risk-off day, but it just hasn’t come,’’ said Dave Roberts, a Washington-based independent trader of volatility options and products. “So it would begin the morning firm; and then just drift lower because stocks have cleared every hurdle to this point.’’

To be sure, it’s far from all-clear for equities. The early-year advance in stocks could be primarily a function of short-covering, with little enthusiastic marginal buying by institutional or retail investors.

Pale Green Lights

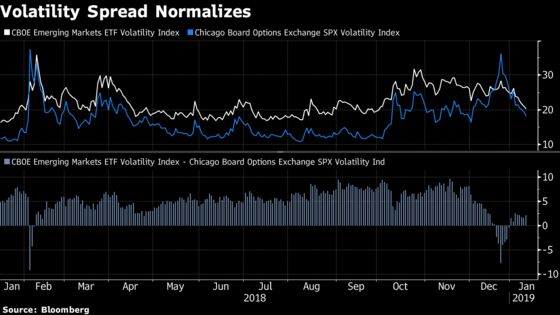

Michael Purves, chief global strategist at Weeden & Co., is looking for normal historical relationships in volatility, which became distorted amid the turmoil, like the shape of the VIX futures curve and the relationship between U.S. and emerging market implied volatility, to revert to a more typical state.

Most of the VIX curve is in contango — the upward-sloping term structure that reflects higher uncertainty about the long-term rather than the near-term for equities. The third month future is still more expensive than longer-dated contract, however, as a range of event risks from the Federal Reserve, to trade, to the U.S. debt loom large.

In a rare twist, emerging-market equity volatility was priced more cheaply than its U.S. counterpart in the last few sessions of 2018. It is no longer.

“You’ve still got the Q1 kink but the general direction of this curve is still pretty constructive,’’ he said. “If that spread starts normalizing again while the VIX and EM VIX are coming down, those are two more pale green light signs that things are getting back to normal again.’’

And pale green lights might be the brightest risk-on signals that investors receive, he notes, as the floor for VIX might not be too far below current levels should realized volatility remain relatively elevated.

Earnings Approach

In addition, there are many technical reasons why the VIX is falling. Implied correlations among S&P 500 constituents have come in rapidly despite realized correlations remaining high. That’s because of the dawn of earnings season, a time when stocks tend to move for company-specific reasons.

The VIX is based on out-of-the-money rather than at the money options, and there’s been little demand for contracts at the tails of the distribution even when stocks were at their most chaotic. That, plus the dearth of intraday reversals, realized volatility drop-off in recent sessions, and onset of earnings season, has proved a powerful palliative force for market-implied equity volatility.

In addition, it’s theoretically normal for the VIX to fall from the open to the close, since it’s calculated using one-month options that tend to decay — that is, lose value — a bit as the day passes.

But little of this encouraging market mechanics will end up mattering if Corporate America’s financial performance and outlook fail to meet expectations.

Shawn P. Quigg, equity derivatives strategist at JPMorgan, notes that there’s an element of complacency embedded in single-stock options.

“Despite the broader market volatility, recent damage to sentiment/technicals, and weight this earnings season may have for the direction of the market, earnings-related implied volatility does not appear overly rich as one might expect,’’ he writes.

The same is true at the index level for investors looking for to bet on a breakout or breakdown of U.S. stocks during earnings season, notes Wells Fargo equity derivatives strategist Pravit Chintawongvanich.

“Regardless of what happens to vol, near dated options have gotten so cheap that it’s worth buying them outright for a break in either direction,’’ he writes. “Upside calls in particular are very cheap, but puts outright are also worth considering as a hedge.’’

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Dave Liedtka, Brendan Walsh

©2019 Bloomberg L.P.