VIX Underpricing Volatility Risk by Almost 40%, Macro Risk Says

VIX Underpricing Volatility Risk by Almost 40%, Macro Risk Says

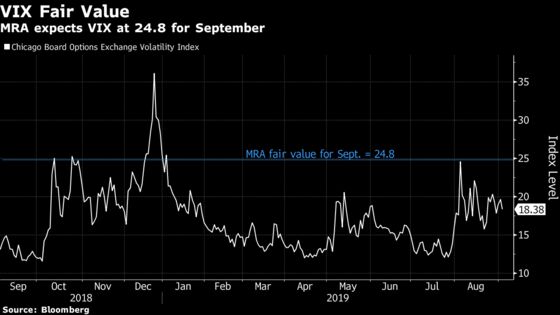

(Bloomberg) -- The Cboe Volatility Index, trading about a point above its one-year average after a tumultuous month for equities, is sending a false signal of calm for the market, a Macro Risk Advisors analysis shows.

Commonly known as the VIX, the gauge uses options prices to track the 30-day implied volatility for S&P 500 Index stocks. It’s currently at around 18. The fair value for this month should be closer to 25, the highest for any September since 2012, Macro Risk Advisors derivatives and quantitative strategist Maxwell Grinacoff wrote in a research note.

Grinacoff joins a growing chorus of analysts and strategists underscoring the relatively low level of implied volatility in the stock market after a jarring August. Historical 30-day volatility in the S&P 500 Index last month peaked at the highest level since February. Stock prices swung wildly on every apparent bust-up and breakthrough in the U.S.-China trade showdown. At the same time, Federal Reserve policy makers were giving mixed messages about how aggressive they’ll be in cutting interest rates to support economic growth.

“We are concerned that U.S. equity prices may not reflect the potential that economic and political headwinds impinge corporate profits going forward,” Grinacoff wrote. “Our backtest results clearly indicate lower, more volatile equity returns in the near-term.”

Grinacoff recommends a defensive strategy using options on the SPDR S&P 500 ETF Trust. Specifically, he advises buying the December $275 puts and selling the December $305 calls for about $3.18 versus a stock reference price of $290.74.

Macro Risk’s fair-value model for the VIX has risen for four months in a row, driven for the last two months by a falling Purchasing Managers Index in the U.S., Grinacoff said.

To contact the reporter on this story: Gregory Calderone in New York at gcalderone7@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Richard Richtmyer, Rita Nazareth

©2019 Bloomberg L.P.