VIX Could Go Much Lower Just as Hedge Funds Bet on Its Futures

VIX Could Go Much Lower Just as Hedge Funds Bet on Its Futures

(Bloomberg) -- U.S. stock volatility may be ripe for significant declines.

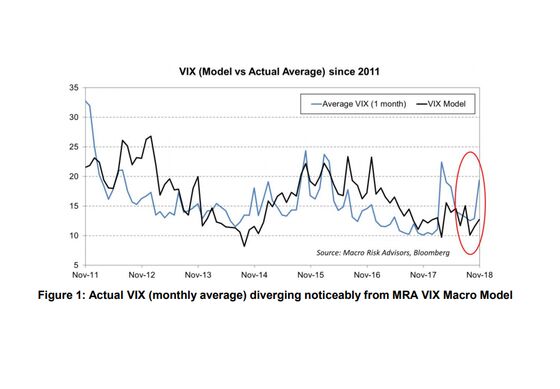

A fair-value model based on economic fundamentals suggests that the Cboe Volatility Index -- the equity market’s “fear gauge” -- should be at a much lower level, according to Vinay Viswanathan and Dean Curnutt of Macro Risk Advisors.

“If business conditions for manufacturers and profitability for S&P 500 companies remain healthy, we expect the VIX to revert much lower,” MRA wrote in report Monday. “The premium of average monthly spot VIX to the MRA Macro Model’s value (6.6 points) is the second-highest it’s been since 2011 (only exceeded by February 2018).”

Todd Salamone of Schaeffer’s Investment Research agrees the VIX could fall, citing data from the Nov. 2 Commitment of Traders report showing that large speculators are now just slightly net long VIX futures.

“Going long VIX futures is considered an extreme for this group,” Salamone wrote in a note on Monday, “and given how they have been dead wrong at extremes, it would not be a bad bet to speculate on declining volatility.”

“The risk is this group being correct for once,” he added.

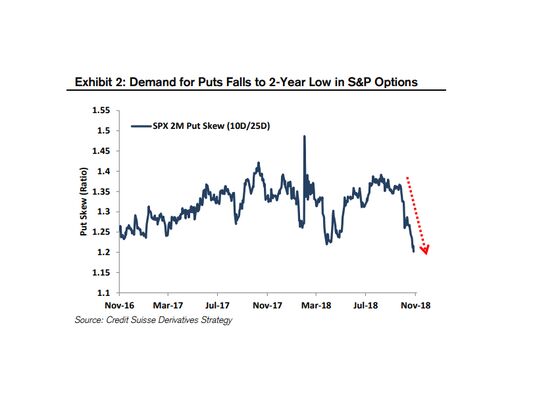

Credit Suisse strategist Mandy Xu, on the other hand, sees more potential for a market decline and a volatility upswing.

“There is very little downside risk priced into the equity options market right now, with skew falling toward year-to-date lows on lack of put demand,” Xu wrote in a note Monday. “A hawkish Fed compounded by lack of progress on the trade front could lead to another leg lower in equities -- something investors seem to be discounting.”

“For investors looking to hedge against the aforementioned scenario, consider buying an S&P put contingent on rates going higher,” she wrote.

MRA, unsurprisingly, has a different tack in mind: buying November 35/32 put spreads on the iPath S&P 500 VIX Short-Term Futures ETN (ticker VXX), or purchasing VIX December 15/13.5 1x2 put spreads, to bet on a decline.

“The current macro backdrop should sustain political uncertainty higher, with a potential floor to making a 1x2 put spread optimal,” MRA wrote.

To contact the reporter on this story: Joanna Ossinger in New York at jossinger@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Andrew Dunn, Randall Jensen

©2018 Bloomberg L.P.