Vanguard and Nuveen See Dimmer 2022 Muni Outlook

Vanguard and Nuveen See Dimmer 2022 Muni Outlook

(Bloomberg) -- The two biggest muni managers during last year’s record breaking wave of issuance and demand expect the next 12 months to be less sunny.

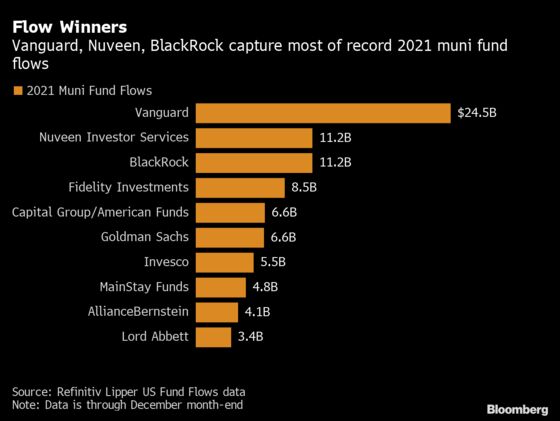

“This year could be a little bit tougher than last year when we had the wind at our backs,” said John Miller, head of municipals at Nuveen, which captured $11.2 billion of muni fund flows in 2021.

Already the $4 trillion municipal bond market looks to be off to its worst start in more than two decades. While January is typically a strong month for munis, the asset class has been hit by the dramatic rise in Treasury yields, spurred by expectations the Federal Reserve will start to raise interest rates as soon as March.

The sharp increase in yields and a more hawkish Fed will be the “biggest headwind” for municipal bonds, Miller said in an interview.

Moreover, those tensions are likely to last for much of the year, with munis unlikely to match their 2021 outperformance, said Paul Malloy, head of municipals at Vanguard Group, which saw $24.5 billion in muni fund flows last year.

“Treasuries are really in the driver’s seat,” said Malloy. “While fundamentals are really good, we expect munis to move alongside Treasuries.”

Combined, Nuveen and Vanguard captured more than a third of last year’s muni fund flows, or money added to state and local-government debt funds, according to Refinitiv Lipper U.S. Fund Flows data.

Unprecedented demand, driven in part by investors’ fear of higher tax rates, helped drive strong muni returns that bested nearly every other fixed income asset class in 2021. But now, with funds flush with cash and valuations still richer than historical average, Vanguard is turning “back to basics,” Malloy said.

“It’s the kind of market, with everything compressed, we like better quality,” said Malloy, who oversees Vanguard’s $267 billion of municipal debt. “We don’t believe this is the time to go bottom feeding at these valuation levels. We are relying on credits with strong long-run fundamentals.”

That includes states and local governments that have continued fully funding their pension payments and bonds sold by colleges with strong endowments.

“Last year we were more aggressive in what we call the mediocre middle,” he said. “This is an environment where there is no need to pursue something that you don’t love for the long run.”

Likewise, Vanguard is avoiding the lowest-quality bonds.

“Anything that we’re not touching is really the lowest quality. The stuff that gets done because there’s not a lot of yield elsewhere and you look at it and go ‘wow, everything has to go 100% right,’ those are the characteristics of what we’re avoiding,” Malloy said, detailing that they’re “not keen” on the more speculative project finance names.

Miller -- who oversees Nuveen’s $223 billion of state and local debt -- said he’s favoring “credit exposure” over pure interest rate risk.

“We are looking at couponing and other structural characteristics that can provide some cushion should rates continue to migrate higher,” he said. Additionally, the Chicago-based manager continues to be positive on major Illinois-based credits, like the City of Chicago and the state’s general obligation bonds. “There is still a little further to run there,” he said.

Miller runs the muni market’s largest high-yield fund, which returned 9.7% in 2021, besting the junk muni benchmark and 98% of peers over the last year, according to data compiled by Bloomberg. High-yield municipals returned almost 8% last year, outperforming the overall muni market by more than 6 percentage points. But, he said those kind of gains are unlikely a second year in a row. One-hundred to 200 basis points of outperformance “would be pretty good compensation for the risk of high yield just to moderate those expectations a bit this year.”

Both fund managers called the recent surge in coronavirus cases a “blip” and said they aren’t changing their portfolio positions because of the omicron variant.

“People, including myself, are trying to look at this as a short-term blip as far as economic impact,” Miller said.

It’s “nothing that changes our long-run fundamental view,” Malloy added.

©2022 Bloomberg L.P.