Value Rotation Was the Last Thing Big Funds Thought Would Happen

Value Rotation Was the Last Thing Big Funds Thought Would Happen

(Bloomberg) -- Investor sentiment has turned abruptly in favor of beaten-down stocks as recovery bets mount. It’s something professional stock investors failed to foresee.

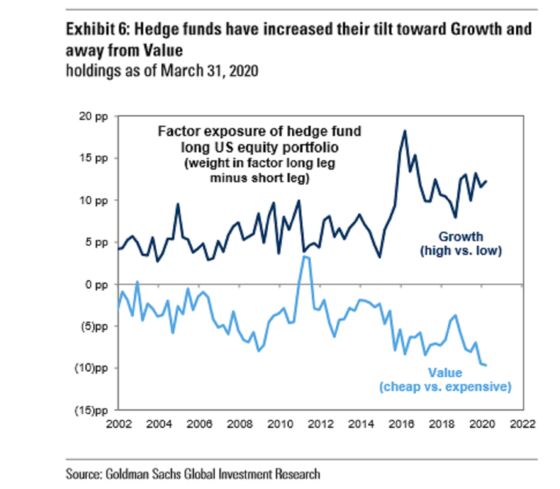

Skepticism toward stocks that are rated cheap relative to metrics like earnings reached a 13-year high among money managers in a Bank of America survey this month. And hedge funds chopped exposure to value shares to the lowest level ever in Goldman Sachs data that starts in 2002.

Those bets are now under pressure amid a rotation out of rally leaders such as technology and into banks and energy companies, an about-face generally credited to budding optimism on the economy. Prevailing aversion among managers may help explain why the shift has been so swift and sudden. Up 5.2% this week, value stocks in the Russell 1000 Index are poised to beat their growth counterparts by the most in 11years.

“Value is under-owned across the broad. From hedge funds’ point, they may actually be short,” Mark Freeman, chief investment officer at Socorro Asset Management LP in Dallas, said by phone. “It doesn’t take much if you get a rotation into that and investors all of a sudden think it’s sustainable. That can create a strong buying support.”

The resurgence of value stocks is part of a risk-on rally that has broadened the market’s leadership from tech megacaps to include financials and small-caps. The Russell 1000 Value index climbed 1.3% Wednesday, compared with a loss of 0.1% for the growth cohort. Viewed by a wider lens, however, the gap in returns remains wide. In 2020, value is down 17%, versus an advance of almost 3% for growth.

Investors favoring growth are sticking with a strategy that has worked persistently for more than a decade, particularly this year amid a flight to safety. In BofA’s latest monthly survey, a net 23% of money managers believed cheap stocks would trail fast-growers, the most since 2007.

Until about a week ago, those bets were winners, with technology and health-care stocks showing resilience and value plays such as banks, energy and materials companies struggling. As optimism about the economy perked up this week, that trade flipped.

“A lot of people I talked to did try to get positioned for a recovery, but it’s just not the kind of stuff they want to be in long term that’s doing well right now,” Lori Calvasina, head of U.S. equity strategy at RBC Capital Markets in an interview on Bloomberg Television. “That creates additional layer of frustration.”

While it’s still too early to determine whether the shift to value can last, the pace of the economic recovery is likely to set the tone for the value-versus-growth trade in coming weeks, according to Socorro’s Freeman.

“It ultimately comes back to investors’ confidence of the duration of the pandemic, and how long it takes for the economy to rebound quickly,” Freeman said. “On the days when the market feels like the duration is going to be short than what’s expected, then value and small will outperform. On the days when maybe it’s going to take longer than expected, then everybody reverts back to megacap growth.”

©2020 Bloomberg L.P.