Unicorns Are About to Chew an $80 Billion Hole in the Surface of Stocks

Unicorns Are About to Chew an $80 Billion Hole in the Surface of Stocks

(Bloomberg) -- Investors have lived through a lot lately, from the Christmas week apocalypse to last year’s Volmaggedon. Now they’ll see if they can survive a new threat: rampaging unicorns.

It’s a question of resilience -- will markets hold up when their increasingly delicate surface is burdened with a cargo of new supply? Bloomberg data shows sales of equity are set to surge in 2019, a deluge with the potential to create more stress for the longest bull run ever.

It’s been a while since anyone cared about dilution in equities, and to be sure, nothing happening this year is more than a drop in the bucket next to the market’s overall value, its daily turnover or volume of buybacks. Still, in a world where valuations are stretched and the slightest hint of trouble can induce panic, the arrival of tens of billions of dollars worth of companies -- many of them mature ones -- strikes some as a recipe for volatility.

“Cycles end when everything looks great, but the point at which supply overwhelms demand,” said Michael Shaoul, chief executive officer at Marketfield Asset Management LLC. “That was true in 2000 with technology, it was true in 2005 in housing, it was true in 2008 and then again in 2011 with commodities.”

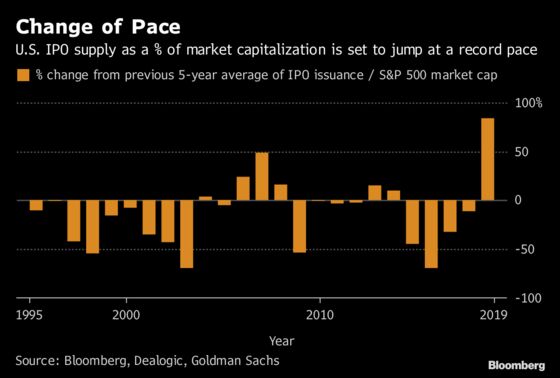

Total U.S. IPO supply as a percent of S&P 500 market capitalization is expected to almost double the average over the last five years, according to data compiled by Bloomberg using inputs from Dealogic and Goldman Sachs. An increase that big would be the largest since at least 1995, and more than three times the average yearly change over the period.

Everywhere you look, unicorns are getting restless. From ride-sharing networks Uber Technologies Inc. and Lyft Inc. to online home-rental service Airbnb Inc., 2019 is poised to see a lot of giant companies transferred to public hands. Whether markets can handle it comes down to textbook economics -- an exercise in supply and demand.

Whether there’s enough risk appetite for the deals is one question. How all the bloat affects the market at large is a much bigger one.

For Shaoul, the issue is as much share supply as the excesses it may bespeak, coming after two years in which $1.5 trillion was added to the value of five Faang companies and two reached valuations never before seen in the U.S. market. While the arrival of a bunch more Internet-powered behemoths doesn’t doom the rally, it’s another in a lengthening list of things to worry about.

“We don’t have a magic crystal to tell us having multi-trillion dollar companies listed on the Nasdaq was the high point, but it certainly might’ve been,” Shaoul said. “October and December’s sell-off was concentrated around U.S. technology in a way that no other sell-off has been. I would be critical at this point, rather than necessarily outright fearful.”

Goldman Sachs estimates that the value of IPOs in the U.S. will reach $80 billion this year, double the yearly average since 1990. To get to the forecast, the firm takes into account six unicorn tech companies that may go public whose combined valuation adds up to $150 billion. If 20 percent of that hits public markets, the value of U.S. tech IPOs alone could be $30 billion, just under the yearly average. Then there’s the rest.

“Aggregate IPO activity has generally been elevated towards the end of the cycle as companies seek valuations at high multiples,” Goldman strategists including David Kostin wrote in a note in November.

Take 2007 for example, just before the financial crisis. About 290 new companies listed on U.S. exchanges with a combined deal value of $65 billion, data from Dealogic show. Both numbers were the highest since 2000. And leading up to the dot-com rout, IPO activity was elevated for years, with deal value jumping above $100 billion in 1999 and 2000.

Part of the reason this year’s estimate is so high is because of the maturity of companies and high valuations. It’s not inconceivable Uber fetches $120 billion, while bankers have told Lyft it could be valued at up to $30 billion and Airbnb was last valued at about $31 billion. The last time three U.S. tech companies worth more than $10 billion went public in the same year was 2000.

For Kathleen Smith, principal at Renaissance Capital, a provider of IPO-focused institutional research and exchange-traded funds, there’s a fair chance this year’s take will exceed Goldman’s estimate. Could that much issuance shock the market and cause volatility? “There’s no doubt about it,” she said.

A few things augur poorly for orderly absorption, among them changes in the market’s contour since the dot-com bubble, according to Smith. One is the growth of passive investing and decline of active management, which removed potential buyers. Individual investors don’t participate as much in IPOs now as they did 20 years ago, and private markets have ballooned.

“If you look at what it took to have a robust $100 billion plus IPO market, we don’t have a lot of those dynamics now,” Smith said. “You have the extra issue of, oh my gosh, look at all this supply. And we’re in a much different market. Where’s the demand? ”

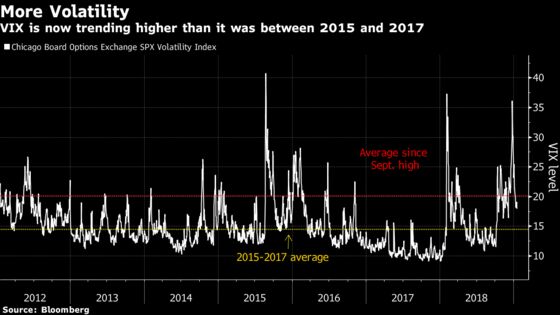

And then there’s the latest market convulsions that raise a question for all the giant private companies: why’d you wait so long? After all, between 2015 and 2017, the Cboe Volatility Index averaged 14.5 -- 25 percent below the long-term average and even further from the average since the S&P 500’s September record. Yet, IPO issuance was the quietest in years.

“We’re in a completely different dynamic and the market’s just come off of a terrible correction,” said Smith. “It amazes me that all these companies have stayed private so long. My mother would say, ‘You need your head examined for not coming out in the market in 2017.”’

The push-and-pull between passive and active management is on track to reach a tipping point in 2019, with passive funds set to hold more assets than their active counterparts by year-end. While ETFs can incorporate newly public companies in their holdings, they often take longer to do so. Take Spotify Technology S.A. for example, which went public last April -- of more than 1,500 U.S. listed equity ETFs, only 1 percent hold it, according to data compiled by Bloomberg.

Should the market come down with IPO indigestion, it could be a bad omen for stock prices. Typically, investors like to look to similar, already public companies for an idea of proper valuation. If the market is lower, IPOs will price lower. Meanwhile, if an investor in a similar sector wants to buy the newly public firm but has no extra cash to do so, they may sell out of existing holdings to make room.

“It’s a little bit of a self-fulfilling prophecy because it’s going to put downward pressure on the comps, which potentially puts downward pressure on the valuation of the IPO itself,” said Erin Browne, managing director and portfolio manager for asset allocation at PIMCO. “The overhang of supply on markets can be a deterrent for global equity markets, but you see it less here in the U.S. Because of the depth of the U.S. market, it can handle a pretty robust supply as long as economic conditions are fairly robust and equity markets are doing well.”

With economic output in the U.S. set to increase 2.5 percent this year and earnings forecast to grow 6.7 percent, there’s reason for optimism. But after December’s near bear market encounter, even with the subsequent comeback, nerves remain.

“Everything changed in the fourth quarter of 2018 -- now sentiment seems to be much more fragile around these concerns about macro things. So we’ll see if it actually affects IPO activity,” said David Ethridge, U.S. IPO services leader at PricewaterhouseCoopers. But even if a large amount of issuance materializes, “when I look at that and think about real impact on the larger public market, it strikes me as sort of a ripple rather than a tidal wave.”

To contact the reporter on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.