Treasuries Buying Wave Triggers First Curve Inversion Since 2007

U.S. Treasury Yield Curve Inverts for First Time Since 2007

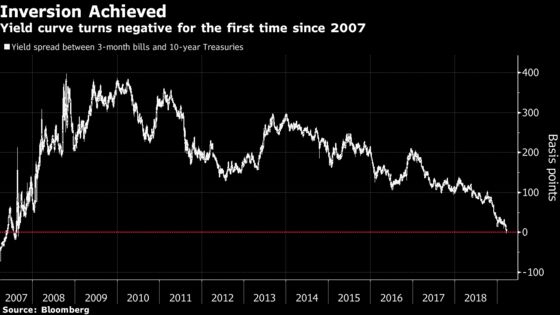

(Bloomberg) -- The Treasury yield curve inverted for the first time since the last crisis Friday, triggering the first reliable market signal of an impending recession and rate-cutting cycle.

The gap between the three-month and 10-year yields vanished as a surge of buying pushed the latter to a 14-month low of 2.416 percent. Inversion is considered a reliable harbinger of recession in the U.S., within roughly the next 18 months.

Demand for government bonds gained momentum Wednesday, when U.S. central bank policy makers lowered both their growth projections and their interest-rate outlook. The majority of officials now envisages no hikes this year, down from a median call of two at their December meeting. Traders took that dovish shift as their cue to dig into positions for a Fed easing cycle, pricing in a cut by the end of 2020 and a one-in-two chance of a reduction as soon as this year.

“It looks like the global slowdown worries have been confirmed and the market is beginning to price in Fed easing, potential recession down the road,” said Kathy Jones, chief fixed-income strategist at Charles Schwab & Co. “It’s clearly a sign that the market is worried about growth and moving into Treasuries from riskier asset classes.”

The wave of buying that’s cut the 10-year yield by nearly 20 basis points in the last couple of days has global catalysts, too. Weaker-than-expected European factory data that helped drive benchmark German yields back below zero on Friday also supported the move.

An upended 3-month to 10-year curve is widely favored as an indicator that the economy is within a couple of years of recession. And Friday’s move is an extension of the inversion at the front end of the curve that happened in December. The gap between the 2-year and 10-year yields has also narrowed, to around 11 basis points.

That said, many downplay the curve’s predictive powers. Some argue that technical factors have distorted the curve’s shape and signaling capacity, particularly as crisis-era policy has tethered yields for the past decade. A downturn may be drawing near after what has been close to the longest expansion on record, however the market provides no precision on when it will happen.

While the 3-month to 10-year spread “has a relatively decent track record of predicting recessions, it suffers from a timing problem,” said TD Securities U.S. rates strategist Gennadiy Goldberg. “Its inversion can suggest a recession occurred six months ago or will occur two years from now.”

--With assistance from Misyrlena Egkolfopoulou.

To contact the reporters on this story: Emily Barrett in New York at ebarrett25@bloomberg.net;Katherine Greifeld in New York at kgreifeld@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Elizabeth Stanton

©2019 Bloomberg L.P.