U.S. Stocks Don’t Need to Fall on Economic Damage, Goldman Says

U.S. Stocks Don’t Need to Fall on Economic Damage, Goldman Says

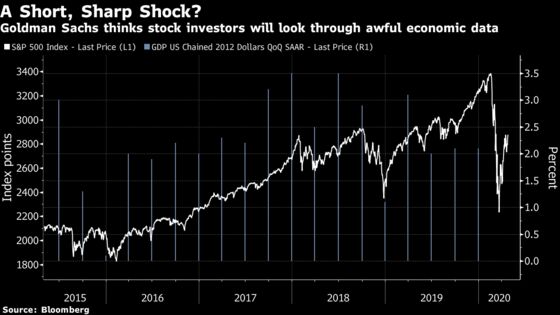

(Bloomberg) -- U.S. stocks may be able to look through a dismal earnings season or two, and the deepest economic contraction in modern history, according to analysis by Goldman Sachs Group Inc.

That’s based on historical analysis that suggests equities price in macroeconomic performance over a two-year horizon. As long as projections are -- as they indeed are now -- for the economy to rebound after the current and coming period of pain, then stocks don’t need to fall, the Wall Street bank concluded.

“Investors usually discount at least the next two years of macroeconomic performance, suggesting markets may continue to look through bad news over the near term if it can reasonably be expected to reverse in the coming quarters,” Zach Pandl, co-head of global FX and EM strategy, wrote in a research note Monday.

Stocks have recovered globally over the past month as governments lay out plans to ease shutdowns to fight the Covid-19 outbreak. The S&P 500 is up 29% from its March 23 close, though remains 15% off the February record high.

To be sure, not all strategists share the optimism that a V-shaped economic course is on the cards.

“Economies will be operating well below capacity for an extended period, with unknown GDP/EPS impact,” UBS Group AG strategist Stuart Kaiser wrote in a note Monday. “Risk markets have moved past systemic risk and worst-case virus outcomes to now focus on the depth and duration of the economic shock.”

Goldman’s analysis used consensus GDP expectations as a guide. Early April, the expectation was for a 4% decline in U.S. gross domestic product, with an expansion of about 4% seen for 2021 and 3% for 2022, Pandl wrote. That marks an unusual pattern for a recession, when economists typically downgrade coming year expectations as well as current-year ones, he noted.

“Metrics that focus only on growth over the next one year (e.g., multiples based on next-12-month earnings expectations) will overstate current valuations, given the large rebound expected beyond this year,” Pandl wrote. “For similar reasons, more disappointing data over the near-term may not affect market pricing if activity is expected to snap back relatively quickly.”

©2020 Bloomberg L.P.