U.S. Stock Outlook Hinges on Battle Between Humans and Machines

U.S. Stock Outlook Hinges on Battle Between Humans and Machines

(Bloomberg) -- A war is brewing between man and machine in U.S. equity markets.

One one side are computer-driven strategies poised to dump billions of dollars of stocks if the recent tumult fails to subside. On the other are the legions of human investors who missed out on the so-called flowless rally that propelled the S&P 500 Index to record highs this year and now have their first real opportunity to buy a meaningful dip.

The winner may determine the near-term direction for a U.S. stock market that’s wavering under the strain of an escalating trade war.

Bank of America’s clients were certainly putting money to work amid the recent sell-off, with the bank reporting the largest equity inflows of the year during the worst week for the S&P 500 in 2019. The buying was robust with institutional and retail clients snapping long selling streaks, according to equity and quantitative strategist Jill Carey Hall.

But signs of weak global economic activity may deter discretionary investors from further boosting their stock holdings. Chinese data released overnight underwhelmed, and U.S. equity futures extended their slump after retail sales posted a surprising contraction in April. The S&P 500 then proceeded to erase losses and turn positive after a report that U.S. President Donald Trump was delaying a decision on whether to impose auto tariffs.

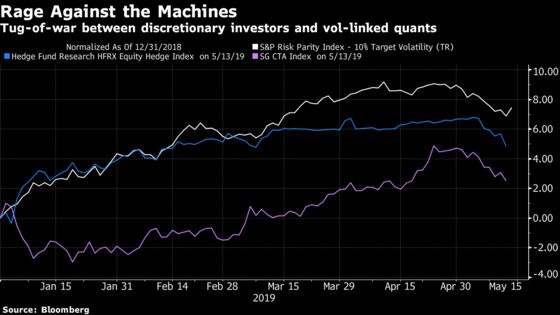

Deleveraging Drive

Billions of dollars in assets are invested in strategies -- such as volatility control -- that base buying or selling on how much an asset class gyrates. A similar strategy is seen with commodity trading advisers (CTAs), quantitative funds that take their cues from the market’s short-term direction. The recent market tumult means these major players will be de-risking, potentially exacerbating the downside for U.S. stocks.

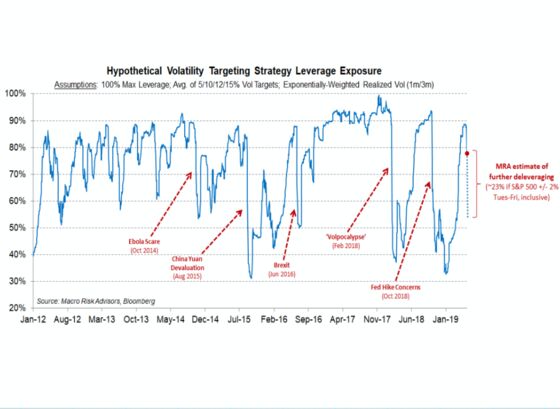

“Volatility-control funds appear to have begun deleveraging as realized volatility has picked up over the past few trading sessions,’’ wrote Maxwell Grinacoff, a quantitative strategist at Macro Risk Advisors. “Deleveraging from these types of funds could beget more selling if we see a succession of 1%-2% down days continue.’’

Macro Risk Advisors estimates that equity selling from this space could approach $60 billion in the coming days should U.S. stocks continue to post big moves -- in either direction. The most damaging scenario would be a massive spike that would compel funds with different risk tolerances to shed exposure all at once.

Ten-day volatility for U.S. stocks is highest since January, when it was on its way down as markets shook off the fourth-quarter risk rout. As the S&P 500 hit all-time highs at the end of April, price swings were below their average level in 2017, the calmest year on record.

Pravit Chintawongvanich, Wells Fargo’s equity derivatives strategist, has a lower estimate for combined selling from volatility-linked funds and CTAs but agrees the deleveraging is on the way.

“There is typically a lag between calculating a new target allocation and adjusting the portfolio, meaning that $20 billion of selling should actually occur over the next few days,’’ he wrote Tuesday. The exodus should still only be “a small amount’’ compared to the October 2018 selloff, in which vol-control and trend followers sold more than $100 billion in short order.

Human Touch

The saving grace for the U.S. equity market may be the swath of investors who have long doubted its advance, but will be converted into bulls thanks to improved valuations.

Sophie Huynh, a cross-asset strategist at Societe Generale, suggested investors who missed the rally could be enticed to enter now, since an economic recession doesn’t appear imminent. Meanwhile, corporate share repurchases would serve as another buffer against “any nasty snowballing effect of the trade war on U.S. equities.’’

“The flowless recovery in U.S. equities since the start of the year, corporate share buybacks and the ‘Fed put’ will be important drivers, and enough to stabilize the S&P 500 in the near-term, despite the trade war background,’’ she said.

Benn Eifert, the chief investment officer at QVR Advisors, has observed investors stepping into the breach during the market retreat to buy the stocks they wish they would have added to their portfolio before the massive rally from the Christmas Eve lows.

“Investors were very underpositioned and underleveraged before this sell-off, so there’s no imminent danger that they’re out of balance sheet,’’ he said. “At some point, the effect gets exhausted if markets keep suffering, but I don’t think we’re there yet.’’

But for Masanari Takada, a quantitative strategist at Nomura, investors should take the “go away’’ portion of the investing cliche about this month to heart.

“Stock-selling pressure is still ramping up,’’ he writes. “For the rest of May, investors should be wary of the downside risks to U.S. equities given the risk of CTAs going short and the imminent rebalancing by risk-parity funds.’’

--With assistance from Justina Lee.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Brendan Walsh

©2019 Bloomberg L.P.