Pension Managers Reveal Why They Love or Hate Private Credit

Pension Managers Reveal Why They Love or Hate Private Credit

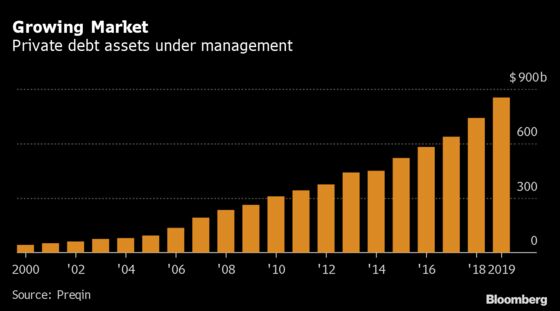

(Bloomberg Markets) -- With some $4 trillion to invest—and returns depressed by ultralow interest rates—U.S. public pension funds have been dipping their toes into private credit. The relatively new asset class had grown quickly, attracting almost $1 trillion, before it was hit by March’s pandemic-driven collapse.

So how do pension fund managers feel about this burgeoning asset class now? Bloomberg Markets talked to officials at nine pension systems of different sizes and in different parts of the country to get their views on how these investments are working out. We heard a wide range of reactions, presented here from the smallest fund to the largest:

San Diego County Employees Retirement Association

Stephen Sexauer, chief investment officer

Size: $11.9 billion

Serves: More than 44,000 members

Private credit allocation: Less than 0.5%

Performance in the lockdown: Too soon to judge

Target allocation: Unchanged

LOOKING BACK: “Why would pension plans get in the banking business and start making loans to corporations?” asks Sexauer, who inherited the private credit allocation from his predecessor. He says the first quarter market sell-off showed him there were more opportunities in the traditional fixed-income markets that don’t involve signing a multiyear contract with a private investment firm and paying the fees that come with such an arrangement.

LOOKING AHEAD: “Our allocation is under a half a percent. We don’t see a lot out there that would change that. Our takeaway right now is it’s a bull market strategy that’s a medieval marriage to generate fees for the private debt managers.” There are likely fewer than a dozen pensions in the U.S. and Canada with the in-house expertise to do the sort of credit work necessary to analyze these deals, Sexauer says. “It doesn’t sound like a scalable business to me. You’re not going to know what the results are for a long time. We’ll see how the returns are in six or seven years.”

School Employees Retirement System of Ohio (SERS)

Farouki Majeed, chief investment officer

Size: $14.5 billion

Serves: More than 200,000 nonteacher school employees

Private credit allocation: 1.3%

Performance in the lockdown: Performed well

Target allocation: 5%

LOOKING BACK: “We have for the most part avoided the sectors most impacted, including hospitality, retail, and energy. Our managers were able to opportunistically deploy capital during the depths of the crisis in March and early April.”

LOOKING AHEAD: “The Covid pandemic has heightened the risks in this space but also presented new opportunities. Since we will be increasing our exposure post-Covid, we feel good about the entry point for new commitments. SERS has committed several hundred million dollars to new funds that are expected to take advantage of the prolonged recovery. We are expecting that new commitments in this period will generate higher returns.”

OTHER STRATEGIES: “Currently we have a small exposure to asset-based leasing/lending strategies in the opportunistic portfolio. We have no plans to increase that exposure at this time.”

Connecticut Retirement Plans & Funds

Shawn Wooden, state treasurer

Size: $36 billion

Serves: 212,000 state and municipal employees

Private credit allocation: 0.4%

Performance in the lockdown: As expected

Target allocation: 5%

LOOKING BACK: “Our view is that private credit is an attractive asset class for us. An important point was trying to expand our access to a wider credit opportunity set that would be more complementary to the more liquid fixed-income strategies. That was our view prior to this; that remains our view today. In February we created the 5% bucket [for private credit], and the crisis hit. The crisis is obviously bad and terrible, but with respect to our greater focus on private credit [the timing] was in many respects perfect. Those private credit opportunities did perform as expected, and we’re pleased with the performance.”

LOOKING AHEAD: “We’ve found that there’s tremendous opportunity.”

OTHER STRATEGIES: “Some of these more niche strategies, such as pharmaceutical royalty, are attractive due to the lower correlation of the exposure and return factors vs. other asset classes. In addition, some of these strategies provide the opportunity to generate attractive absolute and relative returns due to the more niche market opportunity and expertise required by the best investment managers pursuing these strategies. While we do not expect these will be a core component of the allocation, we do have the flexibility to invest in these strategies.”

Arizona State Retirement System

Al Alaimo, senior fixed-income portfolio manager

Size: $41 billion

Serves: More than 500,000 current and retired employees

Private credit allocation: About 15%

Performance in the lockdown: Down less than 1%

LOOKING BACK: “We’re very pleased with how it performed. It helped that our portfolio was well-diversified—with multiple strategies targeting different markets in the U.S. and Europe. We also had very little exposure to energy and retail, two industries particularly hard hit in the economic downturn.”

LOOKING AHEAD: “Since Covid-19, all of the credit markets—both public and private—have repriced, so everything has gotten more attractive, and every new dollar a manager can put to work has higher expected returns today than at the end of last year.”

OTHER STRATEGIES: “In 2019, we really built out our credit asset class and added a number of new managers. Several were in what we call ‘other credit,’ which are private strategies. They include litigation finance, life settlements, risk-sharing transactions, and leasing. Those are niche strategies, but they tend to be very attractive. They also tend to be relatively limited in terms of being able to deploy capital.”

Los Angeles County Retirement Association

Jon Grabel, chief investment officer

Size: $56.8 billion

Serves: More than 165,000 members

Private credit allocation: 2%

Performance in the lockdown: 1.8% net for illiquid credit in the quarter ended in March

Target allocation: Up to 5%

LOOKING BACK: “Some may view illiquid credit or private credit as very distressed-oriented—that, in effect, you use debt securities to get equitylike returns. That is not our strategy. We are not looking for this to be a private equity replacement.

“We made some recent commitments over the last several months. Those commitments have been more single-investment, separate-account-type structures as opposed to drawdown vehicles.”

LOOKING AHEAD: “We are under target. We will continue to evaluate opportunities, but we’re sensitive to markets. The stimulus and intervention from the Fed has impacted credit dramatically.”

Pennsylvania Public School Employees Retirement System

Steve Esack, press secretary

Size: $55.8 billion

Serves: 256,000 active and 234,000 retired school employees

Private credit allocation: 8.5%

Performance in the lockdown: Down 11.3% in first quarter

Target allocation: 10%

LOOKING BACK: “While the portfolio outperformed its benchmark on a relative basis, absolute performance was worse than expected, driven by a couple of outliers. For example, energy investments within the real assets credit allocation were heavily impacted by negative supply-demand dynamics given the uncertainty of OPEC+ production cuts and the collapse of demand due to the global pandemic.”

LOOKING AHEAD: “While there are benefits and drawbacks of private credit vs. other asset classes, we continue to believe the benefits prevail. Compared to public high yield for example, private credit should benefit from its seniority in the capital structure, yield pickup from illiquidity premium, less price volatility, technical-driven selling, and covenant protection. We view private credit as a long-term asset class that shouldn’t be evaluated quarter over quarter.”

OTHER STRATEGIES: “Our current private credit [investment policy statement] provides ample flexibility to consider numerous private credit substrategies. [These include] direct lending, mezzanine, distressed [and] special situations, specialty finance, structured credit, real assets credit, and real estate credit.”

State of Wisconsin Investment Board

Chris Prestigiacomo, portfolio manager

Size: $101.5 billion

Serves: 642,000 participants

Performance in the lockdown: As expected

LOOKING BACK: “There was some volatility in mid-March when things started to unravel a little bit, but that started to come back in early Q2. It was really the Fed’s actions that allowed the credit markets and equity markets to snap back very, very quickly.”

LOOKING AHEAD: “There are a lot of plans out there that, when they see a big downdraft, have to sell at unfortunate times. We don’t have to do that. We can play a volatile cycle. I would say today we’re still very interested in private credit. The spreads haven’t returned to pre-Covid levels, which is good. I think there’s some consensus within our shop that the back half of this year, there will be some more volatility, which we think will bring some good opportunities for us.”

OTHER STRATEGIES: “Within our privates group, excluding hedge funds, we’re predominantly lending to operating businesses across various industries. If you look in our hedge fund book as well as our multiasset book, they participate more in some of the newer strategies: asset-backed, royalty lending, distressed credits—those areas. So we are looking at those kind of ‘niche-y’ areas. As the risks subside and strategies become more developed, that’s when you would see other participants come in and bid up pricing and lower returns. And that’s probably a time where we would be a seller, if we had the ability to exit.”

North Carolina Total Retirement Plans

Dale Folwell, state treasurer

Size: $103.9 billion for the defined benefit plan

Serves: More than 332,000 payees

Allocation: 7% for opportunistic fixed income

LOOKING BACK: “We were finding [credit] more appealing until a big competitor showed up: the Federal Reserve. I’m not criticizing the Fed’s actions, I’m just saying that when they come in and make these multitrillion announcements, obviously spreads narrowed tremendously. It takes time to analyze these deals and in some instances, there wasn’t enough time to analyze them before spreads started tightening.”

LOOKING AHEAD: “I don’t think we have fully witnessed some of the timeless impacts that this virus is going to have on the credit markets.”

State Board of Administration of Florida

Trent Webster, senior investment officer in charge of alternative investments

Size: $160.7 billion in defined benefit retirement assets

Serves: Almost 648,000 active members

Private credit allocation: 2% to 2.25%

Performance in the lockdown: As expected

Target allocation: Likely to grow

LOOKING BACK: “For a couple of years we had gotten quite cautious on credit. We thought spreads had gotten too tight for the most part. We thought the lack of covenants was very unappealing. A lot of money had flowed into the market searching for yield. In March and April, we saw spreads blow out, and we put money to work pretty aggressively where we could.”

LOOKING AHEAD: “The amounts that we have been looking to commit over the first and second quarter of this year are greater than we have committed in the past. We’re watching to see if this rally is justified based on the future economic fundamentals. We do think that in certain parts of the economy there will be very interesting opportunities on the stressed and distressed side, regardless of what the market does.”

Akinnibi covers municipal finance and Butler covers private credit for Bloomberg News in New York.

©2020 Bloomberg L.P.