U.S. GDP Report Clears Path for Two More Fed Rate Hikes

(Bloomberg Opinion) -- The U.S. gross domestic product report for the second quarter will almost certainly cement the case for a September interest-rate increase by the Federal Reserve and keep a December hike in play even though there will be a tendency to dismiss the results due to a burst of soybean exports ahead of retaliatory tariffs imposed by China.

What’s important is that the 4.1 percent rate of growth in the April through June period yields a 2.9 percent average for the past four quarters, a number that likely better represents the underlying pace of economic expansion than quarterly readings. It is also well in excess of the median Fed policy maker estimate of the potential growth rate, which is 1.8 percent, but close to the central bank’s 2018 growth forecast of 2.8 percent.

In other words, even after discounting a strong second-quarter number, the trend in GDP growth suggests the economy is close to the Fed’s expectations. Moreover, it is a pace of activity that promises to sustain rapid job growth sufficient to keep downward pressure on the unemployment rate. Fed Chairman Jerome Powell and his colleagues will not be easily dissuaded from their campaign to push policy rates, currently in a range of 1.75 percent to 2 percent, to at least neutral in this environment.

There has been speculation that a budding global trade war will pressure the Fed to shift to a dovish stance in next week’s Federal Open Market Committee meeting. Indeed, in his recent congressional testimony, Powell highlighted the additional uncertainties in the forecast due to trade. And some companies are starting to feel the pain. Home appliance manufacturer Whirlpool Corp. issued disappointing guidance last week in response to tariff-induced higher material costs, and the U.S. auto industry noted similar negative impacts.

I suspect such speculation is premature. The Fed is certainly sensitive to the issue, and it’s more likely to respond to the negative growth effects of trade shocks rather than the positive impacts on prices. That means Powell and his fellow policy makers would look through any inflationary boost as temporary and instead address any slowing growth with a more dovish policy path.

The caveat is that the impact of tariffs needs to be sufficiently large to drag the economy onto a trajectory substantially below the Fed’s expectations. So far, that isn’t happening. The company-specific impacts have yet to make a large macroeconomic impact. Remember, the trade wars are happening in the context of a burst of fiscal stimulus, which mitigates the negative impacts on the macro economy. And the recent truce in the trade dispute with Europe helps prevent further escalation for the time being. The trade situation with China, however, remains fluid.

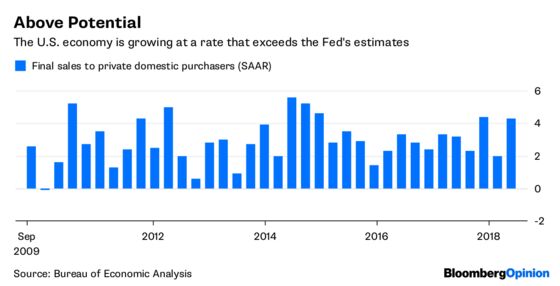

It tends to be that trade is the tail of the U.S. economy, and the tail rarely wags the dog. The disruptions have to grow much larger before that happens. So as much as you are watching what the Fed is saying about trade, watch even more what it’s saying about domestic activity. Real final sales to private domestic purchasers, a measure which excludes government spending, trade and inventory adjustment, grew at a 4.3 percent pace in the second quarter. If these domestic factors remain strong, they will likely outweigh the potential negative trade impacts from a monetary-policy perspective.

Although the Fed may feel compelled to mention trade concerns in next week’s FOMC statement, they will at the same time highlight the domestic economy. Hence, trade concerns will not be sufficient to shift from a balanced assessment of risks. Central bankers will attempt to leave market participants expecting that a worsening trade situation would of course yield a policy shift, but for now the policy remains on the path of gradual increases until rates approach something closer to neutral. The GDP report solidifies this policy path.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Duy is a professor of practice and senior director of the Oregon Economic Forum at the University of Oregon and the author of Tim Duy's Fed Watch.

©2018 Bloomberg L.P.