Trade Talks Have Two Key Implications for Markets

Trade uncertainty will reverse the calm in equity markets that has stemmed from the Federal Reserve’s dovish pivot in January.

(Bloomberg Opinion) -- This week has marked the resumption of global trade uncertainties, with U.S. President Donald Trump threatening to increase tariffs on $200 billion of Chinese products from the current 10 percent to 25 percent starting Friday. At the same time, China is preparing retaliatory tariffs on U.S. imports should Trump carry out his threat, Bloomberg News reports.

There are two major implications for investors. First, the CBOE Volatility Index, or VIX, is likely to rise after several months of relative calm in the so-called fear gauge as larger-than-normal fluctuations in equities become more common. Second, the perception of higher global risk will prompt more capital flows to the U.S., the ultimate haven, boosting the dollar. It’s possible the Bloomberg Dollar Spot Index exceeds levels reached in the aftermath of Trump’s election victory in November 2016. That implies a more than 6 percent gain in the greenback.

Even though a smaller Chinese delegation is headed to Washington for talks, Trump’s tariff threats will be a high hurdle to any deal. The important concept of “saving face” would preclude visiting negotiators from making sufficient concessions to please the U.S. team and reach an agreement. Crucial areas of differences are likely to be centered on U.S. allegations of forced technology transfers and demands that China lower industrial subsidies that boost the competitiveness of its exporters. Although Chinese negotiators have promised in the past to move on these fronts, specific details have yet to be agreed upon.

And even if Chinese officials do make concessions, Trump has shown that’s he’s willing to walk away from deals that his own officials have negotiated. The form and extent of presidential reaction may depend on the pushback Trump gets from his base to any concessions he may have to make to get a deal done. Trade uncertainty will reverse the calm in equity markets that has stemmed from the Federal Reserve’s dovish pivot in January.

The Bloomberg Dollar Spot Index which reached a high of 1,278 in January 2017 has recently drifted at around 1,200 as markets no longer look for two interest-rate increases in 2019 that Fed Chair Jerome Powell had forecast in December. But the period of relative dollar weakness is likely to end soon.

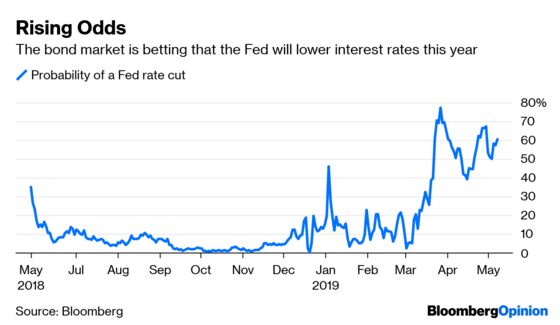

The counter-intuitive reason for the anticipated dollar strength despite a dovish Fed is that global capital flows seek refuge in the perceived safety of U.S. assets – especially Treasury securities – during times of stress. Powell and his colleagues are likely to explain that continuing uncertainties relating to trade could diminish the prospects for U.S. economic growth, justifying rate reductions. Such expressions of caution will prompt additional haven flows into the U.S.

Increased trade tensions may not only provoke a rate cut but also likely speed up the timing of such a move. I expect the first rate to come by the end of June, compared with the end of the year as I had expected.

Add politics to the items playing a role in Fed policy and market volatility. Trump recently demanded that the Fed cut rates immediately by a full percentage point, and Vice President Mike Pence echoed the request on Friday. Even with unemployment at a five-decade low of 3.6 percent, Pence said, the Fed should consider lowering rates. Although the Fed is supposedly independent of the Executive branch, the history of U.S. monetary policy is replete with instances of Fed chairs succumbing to political pressure. (Powell said after the most recent Federal Open Markets Committee meeting on May 1 that he saw no powerful reason to adjust rates now.)

Those investors who consider themselves nimble may find the likely rise in volatility to be positive for their portfolios. But for the majority of market players, especially for the risk averse, it would be opportune to go defensive sooner than they had planned. On the fixed-income front, with Treasuries yielding substantially more than bonds issued by European sovereigns and Japan, a stronger dollar would add to the local currency returns of foreign investors buying the U.S. securities on an unhedged basis.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Komal Sri-Kumar is the president and founder of Sri-Kumar Global Strategies, and the former chief global strategist of Trust Company of the West.

©2019 Bloomberg L.P.