U.S. Bond Raters Win More Access to China’s $14 Trillion Market

U.S. credit rating firms are emerging as some of the winners in the trade deal signed between Washington and Beijing.

(Bloomberg) --

U.S. credit rating firms are emerging as some of the winners in the trade deal signed between Washington and Beijing.

The agreement means debt graders such as Moody’s Corp. can join S&P Global Inc. in rating debt in China’s 95 trillion yuan ($14 trillion) bond market as part of a deal on financial services.

“China commits that it shall continue to allow U.S. service suppliers, including wholly U.S.-owned credit rating services suppliers, to rate all types of domestic bonds sold to domestic and international investors,” according to the text of a trade agreement signed Wednesday in Washington. Moody’s Chief Executive Officer Raymond McDaniel participated in the ceremony.

The move shows progress in China’s promise nearly three years ago to open the door for overseas ratings firm as a way to speed up reform and foster competition. S&P last year became the first wholly owned international firm to rate domestic bonds, while Moody’s efforts to expand its onshore presence were held up.

“China has taken important steps on credit rating agency market opening,” McDaniel said in a statement. “The U.S.-China Phase I Agreement acknowledges and enshrines those commitments in a bilateral trade agreement, which we support.”

The first phase of the trade deal signed by Vice Premier Liu He and President Donald Trump commits China to accelerate its planned opening of its $21 trillion capital market by eight months, swinging the door open for global investment banks. Wall Street will be allowed to apply to form fully owned units to do a broad array of investment banking and securities dealing in the Communist Party-ruled nation.

China has over the past two years embarked on an unprecedented policy of leveling the playing field for international finance. But despite rule changes, including allowing majority stakes in domestic joint ventures, foreign entities say they still face hidden barriers such as lengthy and opaque regulatory approval process as they try to gain increased access to the market.

Moody’s shelved a plan last year to take control of China Chengxin International Credit Rating Co., the nation’s largest ratings company, amid regulatory inaction and U.S.-China trade tensions, people familiar with the matter said. Its application for a wholly owned unit wasn’t approved either.

“Each party shall allow a supplier of credit rating services of the other party to acquire a majority ownership stake in the supplier’s existing joint venture,” according to the agreement.

By bringing in international rating agencies, China hopes to meet global investors’ demand for various yuan-denominated assets and improve the quality of credit assessments in the world’s second-largest bond market.

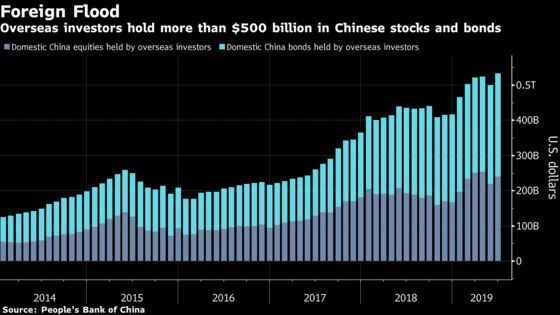

Foreign investors hold a combined $533 billion in Chinese debt and equities, accounting for 2.2% of the country’s overall bond market and 3.1% of the stock market, according to the People’s Bank of China. BNP Paribas predicted last year that the share would reach 15% of the bond market within seven years, while the stock market would hit that mark sooner.

China’s credit rating sector has been plagued by inflated ratings as agencies vie for businesses and debt raters were slow to anticipate a surge in defaults. About 66% of non-financial company debt instruments in China were rated of AA+ or above as of the end of last September, according to a Dec. 6 statement from the National Association of Financial Market Institutional Investors, which oversees China’s interbank bond market.

--With assistance from Caleb Mutua.

To contact Bloomberg News staff for this story: Evelyn Yu in Shanghai at yyu263@bloomberg.net;Tongjian Dong in Shanghai at tdong28@bloomberg.net

To contact the editors responsible for this story: Candice Zachariahs at czachariahs2@bloomberg.net, ;Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Jonas Bergman, Alan Goldstein

©2020 Bloomberg L.P.

With assistance from Bloomberg