Hedge Funds, U.S. Banks Target Europe's Top Rated CLO Debt

U.S. Banks, Hedge Funds Dive Into Europe's Triple-A CLO Debt

(Bloomberg) -- U.S. investors have stepped up their pursuit of European collateralized loan obligations as the yield on offer has become more attractive compared to what they can get at home.

Banks’ treasury departments and institutional investors based in the U.S. are hunting for top-rated CLO notes from Europe, say managers and arrangers. Hedge funds, using leverage to lift their returns, are after the same paper.

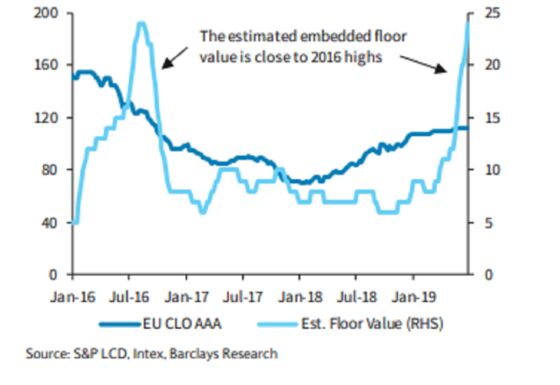

Their appetite is partly down to the fact that European CLOs offer a boost to returns because the spread they pay is over a Euribor floor that’s set at 0%. The value of that floor has increased on the back of expectations that European interest rates will remain in negative territory for longer.

Increased interest from U.S. buyers could result in pricing on European CLO debt moving tighter again. Spreads on triple-A notes have already been compressing in recent weeks, and U.S. demand could take them to their tightest levels of the year. That would be a boon to the next batch of issuers, which include Ares European Loan Management LLP, Sound Point Capital Management LP and Barings (U.K.) Limited.

Floor Managers

For U.S. buyers, moving into European CLOs means they can take advantage of a pick-up in yield when swapping between currencies, which can be further bolstered by as much as 35 basis points by the 0% Euribor floor.

"European triple-A CLO paper looks attractive to U.S. buyers due to the cross currency euro/dollar relative value, especially when considering the value of the embedded Euribor floor," said Geoff Horton, CLO strategist at Barclays Bank.

Looser ECB Policy to Bolster Value of CLO Floors: Fair Oaks

Even though U.S. CLOs currently pay a fatter spread, there is still attractive relative value in buying European assets. Spreads on U.S. new-issue triple-A notes range from 128 to 143 basis points, according to JPMorgan in a July 12 research note. In Europe, recent new-issue triple-As have priced as low as 110 basis points.

In the context of other investing opportunities, the yield pick-up on triple-A CLO notes versus other investment grade credit is more attractive in Europe than it is in the U.S, Horton added.

Horton is among those forecasting additional tightening of European triple-A spreads to 100 basis points by the end of the year. He notes other factors that could feed into a reduction in spreads including the possible re-engagement of the big Japanese buyers of top-rated paper, and a reduction in new-issue supply after the summer.

New issue volume amounted to 14.7 billion euros in the first half of 2019, up 10% on the year. July is on track to be the busiest month of the year, with nearly 3 billion euros of paper already priced and another four managers lining up deals.

Nochu-Watch

If Europe’s CLO spreads do tighten again, aided by these U.S. buyers, it begs the question of what the market’s biggest investor, Japan’s Norinchukin Bank, might offer as and when it looks to return to the European market.

Earlier this year, the anchor investor moved its pricing on triple-A notes wider, from 108-108.5 basis points to 113 basis points, as it eased back from its previously dominant position.

To return to the market, Nochu would need to offer competitive pricing, say managers who have worked with the Japanese buyer in the past, and that could potentially mean inside where it was investing earlier in the year.

Norinchukin Needs to Woo CLO Managers to Re-Enter Europe Market

(Sarah Husband is a leveraged finance strategist who writes for Bloomberg. The observations she makes are her own and not intended as investment advice.)

To contact the reporter on this story: Sarah Husband in London at shusband@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Ruth McGavin

©2019 Bloomberg L.P.