Two Pillars of the Stock Market Just Became Two Reasons to Sell

Two Pillars of the Stock Market Just Became Two Reasons to Sell

(Bloomberg) -- The conventional wisdom that the Fed’s next move would be down and the trade spat with China would end just got dealt a one-two punch.

Benchmark equity indexes have fallen from record highs since Federal Reserve Chair Jerome Powell pushed back against calls for a near-term rate cut and U.S. President Donald Trump threatened to ratchet up tariffs on imported Chinese goods. The catalysts sparked an ominous sense of déjà vu: In 2018, U.S. markets peaked just before Trump slapped tariffs on $200 billion in Chinese imports and Powell commented on how high rates would need to rise.

These fresh developments – particularly on trade – wrong-footed investors, who had become convinced a trade deal with China was inevitable and increasingly confident the Fed would lower rates in a bid to boost price pressures.

“Increasingly frequent headlines suggesting a deal was forthcoming have been reflected in positive price action to the point that we have felt the market was priced for perfection,” writes Morgan Stanley chief equity strategist Michael Wilson, and such a condition means that “negative surprises can have a greater price impact than fundamentals might dictate.’’

The Fed’s change in tone shaved 0.8 percent from the S&P 500 on Wednesday -- the biggest drop in six weeks -- while Trump’s tweets took the same amount off Monday. If not for the other market pillars -- the economy and earnings -- it may have been worse.

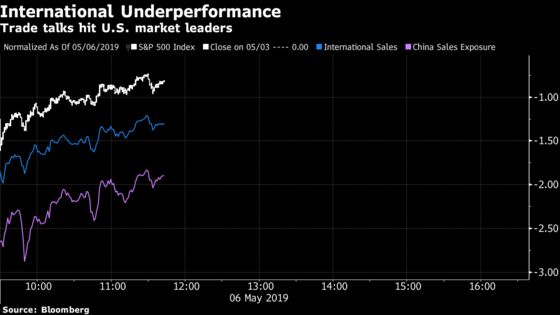

The initial reaction in trade-tied shares was stark. The internationally-geared stocks that have powered the S&P 500’s gains this year opened down 2 percent; U.S. companies with a high share of sales to China were down almost 3 percent at their lows. Those two groups had outperformed the S&P 500 Index by 8 and 10 percentage points year to date, respectively, heading into this week.

If the trade war continues to escalate, it would likely hit U.S. companies’ earnings and in turn further rattle equities. And yet, investors aren’t taking Trump’s salvo very seriously, warned Mandy Xu, head of equity derivatives strategy at Credit Suisse, with “no event risk premium priced in for potential new tariffs on Friday.”

That is, S&P 500 options that expire on Friday don’t have a higher implied volatility than the maturities immediately preceding or following them.

While the Fed is far from a foe for investors, its stance isn’t getting any friendlier. Investors may have underestimated the central bank’s hawkishness late last year, but are now over-estimating its dovishness.

Powell threw cold water on the potential for the Fed to cut rates solely because of sluggish inflation, deeming the recent shortfall in price pressures to be due to temporary factors.

That characterization suggests he “may be missing the forest for the trees,’’ Northern Trust Wealth Management chief investment officer Katie Nixon said. “Consistent with the negative reaction from investors back in October of 2018 to the comment that the policy rate was ‘far from neutral,’ the use of the word transitory left many worried that, once again, the Fed was behind the curve.’’

Even after this equity retreat, fed funds futures imply lower odds of a rate cut in 2019 than they had before the recent decision.

“Discussing even the possibility of a rate hike this year may seem premature, but we can no longer rule it out: A rate hike is a risk,” UBS chief U.S. economist Seth Carpenter wrote. “The Committee may turn increasingly hawkish sooner than anticipated.’’

And that may be an issue for equity bulls, as the S&P 500 Index’s year-to-date rally has been accompanied by a retreat in inflation-protected Treasury yields, which flatters equity valuations.

The Fed “will be jawboning the market to higher yields, which I think will be accompanied by weaker equity markets,’’ writes Peter Tchir, head of macro strategy at Academy Securities.

--With assistance from Lu Wang.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Randall Jensen, Rita Nazareth

©2019 Bloomberg L.P.