Everything That Goes Wrong When Stocks and Bonds Fall Together

U.S. equity and Treasury co-movement is at weakest in years.

(Bloomberg) -- The biggest post-crisis shift in the investment landscape may be looming, threatening more pain for investors besieged by an uptick in real interest rates and cross-asset volatility.

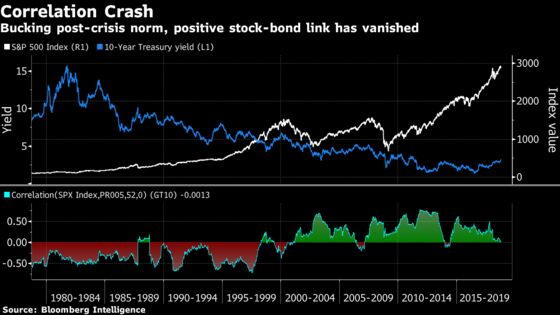

Bonds and equities are doing something they don’t usually do -- fall in unison -- with the latest move driving their normal inverse correlation to the weakest levels of the past two decades. The relationship has come completely apart only three times in that period, and each episode was followed by an equity market slump, including the last one, in 2014.

More synchronized weakness could also leave investors exposed, upending diversification strategies that helped them hedge losses in either market.

Saying what’s going on is easy. The harder part is pinpointing why. A variety of forces are helping to lift bond yields, from Federal Reserve interest-rate hikes to record government borrowing and concern that the economy could be heading into inflationary overdrive, potentially eroding returns. Some of these factors, combined with the resulting increase in Treasury yields that pushes up borrowing costs across the economy, can also weigh on company profitability and stock prices.

“It’s always hard to judge at what point you hit an inflection point where the correlation between yields and stocks goes into reverse,” says Liz Ann Sonders, chief investment strategist at Charles Schwab & Co. “One of the markers to when that happens is typically when you move from a deflationary era or at least a deflationary mindset to more of an inflationary mindset.”

It’s potentially a big deal.

An enduring rupture in positive correlations -- yields moving up along with stocks -- would signal a break in the weak-growth, low-interest regime seen over much of the past decade. Markets driven by negative tandem moves -- yields up, shares down -- have tended to be in the grip of inflationary pressure or potential economic over-heating.

“The correlation between stocks and bond yields has been positive for the better part of the past 20 years,” Bloomberg Intelligence equity strategists Gina Martin Adams and Aditya Kalgutkar wrote in a note on Tuesday. “Each flip to a negative correlation (2006-07, 2013-14) preceded a significant equity-market correction.”

Bond Rout

The dynamic has entered center stage in the past few days, after the yield on the 10-year benchmark raced to a seven-year peak, while the S&P 500 Index has fallen for the past week and on Wednesday touched its lowest level in a month. Those moves could be just a taste of what’s to come.

“Don’t be lulled by how well the stock market has weathered rising yields and creeping inflation thus far,” Leuthold Group’s James Paulsen wrote in a research note this week. “Wall Street’s Overheat Mindset (as signified by the stock/bond yield correlation) appears to be on the cusp of greater anxiety.”

Paulsen reckons investors’ yield-risk sensitivities have been dulled, but that as Wall Street worries more about inflation, stocks will show an increasing reaction to rising rates. While both price growth and yields remain low by historic standards, he expects “overheat pressure” to become a more dominant force, potentially triggering further adverse equity moves.

That would mark a departure from the post-crisis era -- barring 2013’s Taper Tantrum -- in which bonds picked up the slack as stocks tumbled. That dynamic has juiced vanilla 60/40 portfolios and risk-parity strategies along the way.

Not everyone thinks we’re there. So far, inflation remains consistent with a broader environment of strengthening growth -- a positive backdrop for equities, says Schwab’s Sonders. In her view, price pressures are still relatively benign. “Rates are coming up from an incredibly low level. It’s going to take a while before they start to bite.”

Reverberations

Diversification-minded investors have plenty of reasons to take solace. If price pressures are set to spur a shift in market regimes, some investors haven’t got the memo.

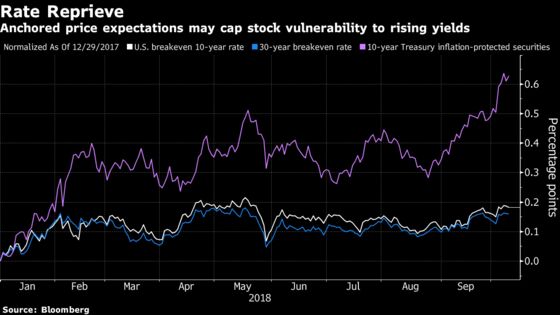

The recent Treasury rout has been driven by an uptick in real yields rather than market-derived inflation expectations.

What’s more, the yield curve has been gripped by bear steepening lately -- an advance in longer-dated yields outpacing the shorter end.

That’s typically a boon for financials and cyclicals, helping benchmark stock indexes to rally, according to Pravit Chintawongvanich, equity derivatives strategist at Wells Fargo Securities.

“It’s important to remember that when the correlation was negative (yields up/stocks down) and rates were very high, inflation was the primary concern for rates,” he wrote in a note. “We think the weakness in stocks and jump higher in the VIX reflects higher risk premium across the board -- the unexpected jump higher in rates and rate vol reverberating through to the equity market.”

To contact the reporters on this story: Sid Verma in London at sverma100@bloomberg.net;Emily Barrett in New York at ebarrett25@bloomberg.net;Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Jeremy Herron

©2018 Bloomberg L.P.