Turmoil Makes the Search for Yield More Relevant

Turmoil Makes the Search for Yield More Relevant

(Bloomberg) -- European stocks just recorded their worst week since mid-October, and the absence of a real bounce on Friday was a reminder that investors have turned cautious. Since trade negotiations could drag on for longer, and with interest rates likely to remain low for some time, the search for yield has put dividends back into focus as a safer way to keep exposure to equities.

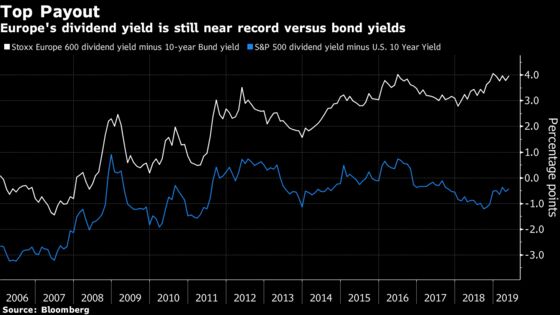

Dovish central banks are giving some visibility on the rate front, and investors could take advantage of the current situation. The spread between European dividend yields and bund yields is still at record levels, in contrast with the spread in the U.S.

A season with growing or resilient earnings per share (EPS) could also mean dividends are safer. The median EPS is set to rise 1% for the first quarter, and the proportion of companies beating estimates stands at 54%, the highest in the past seven quarters, according to Deutsche Bank.

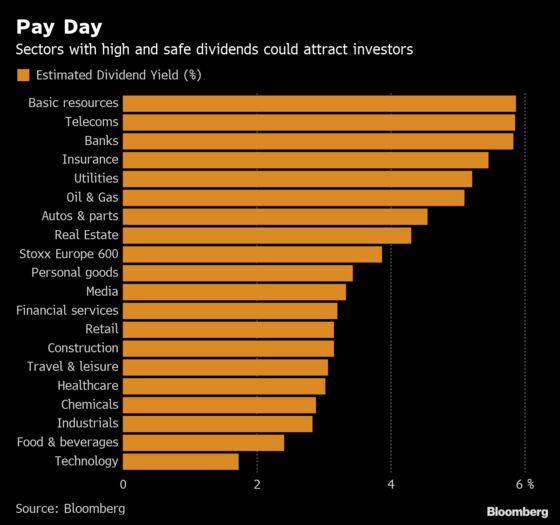

Several sectors offer high payouts, although macro uncertainties may push investors to be wary of banks, miners or autos. Societe Generale strategists said sectors with good cash-flow generation, such as oil & gas and insurance, are better plays.

Within the oil sector, Morgan Stanley upgraded Royal Dutch Shell last week in anticipation of a dividend hike.

| Stock | Est. Dividend Yield |

| Royal Dutch Shell | 6.0% |

| Repsol | 6.6% |

| BP | 6.0% |

| ENI | 5.9% |

| Total | 5.6% |

| Source: Bloomberg |

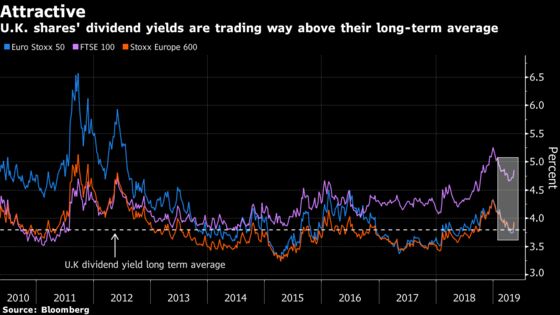

“It’s simple: markets track dividends,” Citigroup strategists write in a note, saying that global equities have risen 7% a year since 2010 mostly because returns have grown similarly over the period. Tactically, buying equities when they’re cheap against their average payout yield has been a good trade, and the current situation favors the U.K. market, Citi said.

In recent years, investors have preferred U.S. equities in a search for dividend growth, despite their low yields. That may change as Citi forecasts lower returns for U.S. stocks in the next two years.

After further trade jitters over the weekend, Euro Stoxx 50 futures are trading 0.9 percent lower from their last trade on Friday, while S&P 500 futures are down 1.1%.

- Watch autos following a report out of Japan that Renault has made a formal merger proposal to Nissan. Watch automakers including Volkswagen, BMW, Daimler and Peugeot for any reaction to the report.

- Watch trade-sensitive sectors after the divide appears to be deep and trust has been eroded between the U.S. and China, meaning any short-term prospect of a deal appears remote.

- Watch stocks volatility as traders flee higher-risk stocks for the safety of the dollar, gold, Treasuries and the yen.

- Watch the pound and U.K. stocks after polls showed Nigel Farage’s Brexit Party surging, adding pressure on Prime Minister Theresa May. Talks with Labour are stalling, although currency strategists think there is a cheap chance to snap up some pound volatility and bet that a deal will get done eventually.

COMMENT:

- “As we have noted previously, U.S. equities typically see modest sell-offs of 3-5% every 2-3 months,” Deutsche Bank strategists write in note. “The 25% rally since late December running for over 4½ months has run very long without one (91st percentile on duration) and strong (96th percentile on size). Equity positioning was also getting extended, albeit not unanimously so, while flows had gravitated towards bonds and out of equities.”

COMPANY NEWS AND M&A:

- Renault Makes Formal Merger Proposal to Nissan, TBS Reports (1)

- EON 1Q Adj. Ebit Falls 8%, Slightly Beats Estimates

- Thyssenkrupp Open to Partnerships, Asset Sales: Handelsblatt

- BHP Is Likely to Push Ahead on Jansen Potash, Ord Minnett Says

- Metro Bank Exploring Sale of More Than GBP1b Worth of Loans: FT

- Vodafone May Sell Tower Firm Stake to Redeem Pledged Shares: ET

- Norway Won’t Require 2/3 Majority for Oslo Bors Takeover: NA

- Euronext to Buy Oslo Bors by End-June After Norway Clearance

- Nasdaq Approved by Norway as Suitable Owner of Oslo Bors VPS

- Red Electrica to Carry Out Reorganization, Expansion Reports

NOTES FROM THE SELL SIDE:

- Marks & Spencer is “making itself more relevant for the next decade” with structural changes including the U.K. retailer’s joint venture with Ocado, Citi says in note. Upgrades M&S to buy and says investment case is evolving.

- Citi recommends to buy Rolls-Royce, stay neutral on Safran but sell MTU Aero, after comparing the three engine manufacturers, saying look at long-term cash generation and not profits.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 382.7 (50-DMA); 392.7 (July 2018 high)

- Support at 374.5 (61.8% Fibo); 369.4 (200-DMA)

- RSI: 33.5

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,399 (50-DMA); 3,516 (76.4% Fibo)

- Support at 3,309 (50% Fibo); 3,276 (200-DMA)

- RSI: 36.6

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Getinge upgraded to reduce at AlphaValue

- Hochtief upgraded to outperform at Macquarie

- Marks & Spencer upgraded to buy at Citi

- Shell upgraded to buy at HSBC; PT 27.40 Pounds

DOWNGRADES:

- Air France-KLM cut to underperform at Bernstein; PT 7 Euros

- Ambu downgraded to hold at ABG; PT 155 Kroner

- Evraz downgraded to underweight at Morgan Stanley; PT 5 Pounds

- Heidelberger Druck downgraded to hold at HSBC; PT 1.60 Euros

- Intu downgraded to underweight at JPMorgan; PT 94 Pence

- MTU Aero downgraded to sell at Citi

- Man Group downgraded to neutral at Goldman; PT 1.50 Pounds

- Tyman downgraded to add at Peel Hunt

- Verkkokauppa.com cut to accumulate at Inderes; PT 4.40 Euros

INITIATIONS:

- Medica rated new reduce at Peel Hunt; PT 1.43 Pounds

MARKETS:

- MSCI Asia Pacific up 0.2%, Nikkei 225 down 0.8%

- S&P 500 up 0.4%, Dow up 0.4%, Nasdaq up 0.1%

- Euro down 0.04% at $1.1229

- Dollar Index up 0% at 97.33

- Yen up 0.18% at 109.75

- Brent up 0.4% at $70.9/bbl, WTI little changed at $61.7/bbl

- LME 3m Copper down 0.6% at $6089.5/MT

- Gold spot down 0.1% at $1285/oz

- US 10Yr yield down 3bps at 2.43%

MAIN MACRO DATA (all times CET):

- 8:35am: (GE) Bloomberg May Germany Economic Survey

- 8:40am: (FR) Bloomberg May France Economic Survey

- 8:45am: (IT) Bloomberg May Italy Economic Survey

- 8:50am: (SP) Bloomberg May Spain Economic Survey

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Celeste Perri at cperri@bloomberg.net, Jon Menon, Blaise Robinson

©2019 Bloomberg L.P.