(Bloomberg Opinion) -- Americans reading gloomy headlines about the trade war with China could be forgiven for wondering what all the fuss is about.

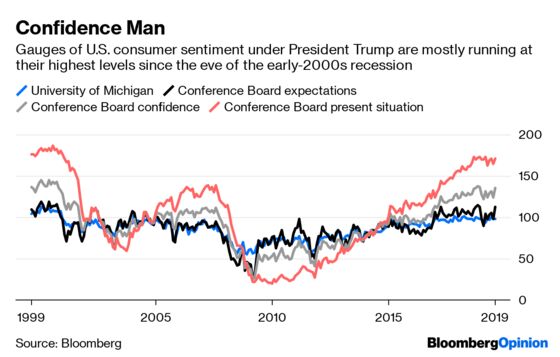

Bloomberg’s consumer comfort index, a weekly phone survey conducted since 1985, is running at its highest levels since 2000. Similar gauges of the household sector, such as the University of Michigan’s consumer sentiment index and the Conference Board’s various consumer confidence surveys, are posting the best results since the eve of the early 2000s recession.

That’s a stark contrast to what’s happening in industry. The ISM Manufacturing Index eased to its lowest level since President Donald Trump’s election, and the Markit Manufacturing PMI is flirting with outright contraction with its weakest reading since September 2009 in July. Measures of industrial production are barely growing and the Conference Board’s leading index in June fell at the fastest pace since early 2016.

One explanation for what’s happening is that households haven’t yet felt the impact of U.S.-China tensions. Trade Representative Robert Lighthizer has been careful to spare them by exempting most retail products from the 25% tariffs he’s imposed on $250 billion of goods so far. With Trump’s promise Thursday to add a 10% levy on the remaining goods trade between the two countries from Sept. 1, that’s about to change.

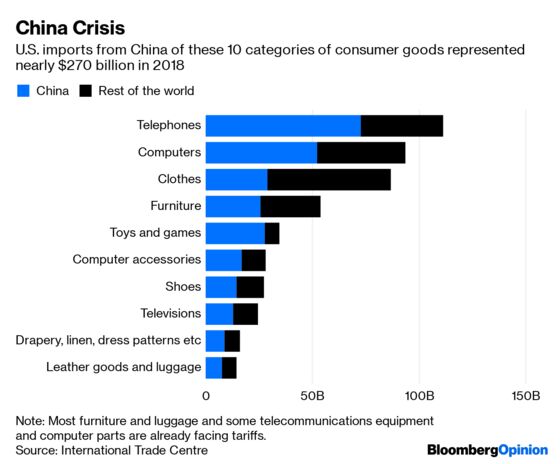

There’s a range of popular consumer products for which America is still deeply dependent on Chinese imports. As my colleague Shira Ovide notes, Apple Inc. could be one of the biggest victims: Telephones (mostly mobile handsets like the iPhone) and computers are the two biggest categories of U.S. imports from China.

Other goods where China accounts for more than half of U.S. imports include toys and games; computer accessories; shoes; televisions; drapery and linen; and leather goods and luggage. That large share of the total is important, because one of the best ways of minimizing the risk of higher prices for consumers is for imports to diversify to other countries such as Mexico and Vietnam. When China makes up more than 50% of the import market, rejigging supply chains becomes extraordinarily challenging.

Federal Reserve Chairman Jerome Powell could take some of the edge off the pain by further cutting interest rates, after lowering them this week for the first time in a decade. Three-month overnight interest swaps are trading at 2.05%, indicating that traders expect a further quarter-point cut before Thanksgiving.

Still, it would be a mistake to think the impact of such a move would be straightforward. Powell’s initial shift away from raising rates helped spark a fall in the Chinese yuan against the dollar of about 3.9% between mid-April and mid-May as currency traders bet on a relative strengthening of the U.S. economy. The renminbi is now just a fraction above its weakest levels in a decade. But that’s still not enough to offset a 10% tariff, and most of the effects of exchange-rate movements aren’t passed through to consumer goods anyway.

After the trade-related shocks of the past year, the ebullient state of the American consumer is potent testimony to the resilience of the U.S. economy. But even that has limits. A one-tenth hike in the price of regularly purchased items like clothing, toys and consumer electronics risks exhausting households’ patience, especially as the decade-long fall in unemployment rates starts to bottom out.

There’s likely to be feedback effects, too. To the extent that industrial conditions are still mildly positive at the moment, that probably owes a great deal to the fact that consumers are in an extremely good mood. By threatening to bring the trade turmoil to U.S. households, Trump risks upsetting that delicate balance.

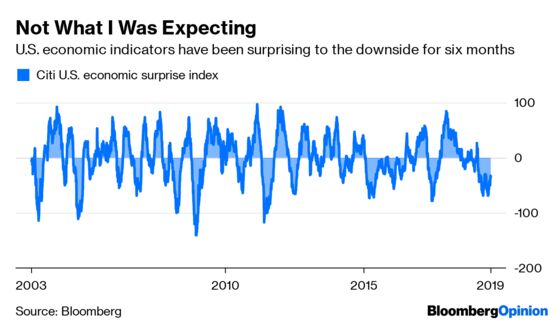

Equity markets are still in a bullish state, but beneath the surface the American economy has been disappointing expectations for the past six months. Further imposts on the consumer aren’t going to help it turn that corner.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.