Treasury Yield Spike Risks Sparking Domino Effect in Markets

One of the year’s biggest spikes in Treasury yields has investors mapping out the impact of rising rates on markets.

(Bloomberg) -- One of the year’s biggest spikes in Treasury yields has investors mapping out the impact of rising rates on markets ranging from stocks to corporate bonds.

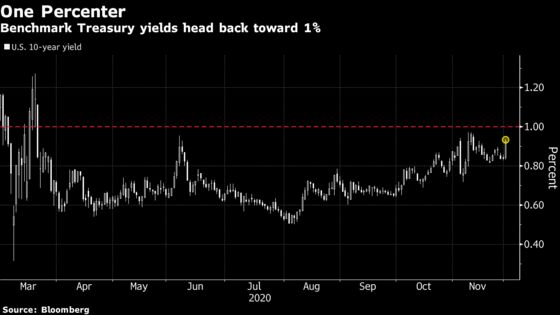

Renewed optimism about U.S. stimulus talks pushed the benchmark 10-year yield to a high of 0.96% on Wednesday, a move which if continued could spark a domino effect across risk assets trading at all-time highs thanks to low interest rates. At issue is whether the jump in yields is accompanied by an economic recovery and moderate levels of inflation that would allow the Federal Reserve to keep rates low.

So far it seems investors are positioning for that scenario, with the Treasury curve -- often a gauge of growth expectations -- steepening and U.S. stocks holding near record highs. Ten-year breakevens -- a market-based gauge of inflation expectations -- though highest since May 2019 remain well below last year’s 2.2% peak.

A 10-year yield of 1% to 2% “is certainly possible, and it would have wide implications across everything from emerging Asian currencies to commodities,” said Vishnu Varathan, head of economics and strategy at Mizuho Bank Ltd. in Singapore. “It’s likely a matter of when -- not if -- yields will climb.”

Ten-year Treasury yields rose about 2 basis points to 0.94% Wednesday as of 2 p.m. in New York.

Benchmark yields have tripled from their March lows on bets of a global economic recovery and a “return to normal” from the pandemic with the help of vaccines. A Bank of America survey last month found a record 73% of investors expected a steeper yield curve.

Here’s a look at what higher Treasury yields could mean for various asset classes:

Skyrocketing Stocks

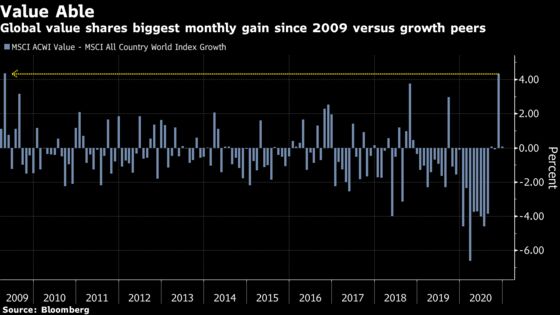

One of the clearest winners from a modest rise in Treasury yields could be equities, particularly those most exposed to a reflating economy. The MSCI AC World Index is at a record, and rotation to cyclical shares such as industrial and materials names accelerated last month.

“To the extent yields rise, it’s likely to be on higher inflation expectations,” said Andrew Sheets, cross-asset strategist at Morgan Stanley. “Periods where yields were rising and the yield curve is steepening -- those are some of the best periods for the stock market.”

But key to the bullish outlook for stocks is inflation remaining under control and economic growth returning. A return to the dreaded stagflation of the 1970s, for example, would quickly derail any rally in risk assets.

“You cannot rule out inflation returning -- it could creep up on us through 2021, 2022,” said Stephen Miller, an adviser at GSFM, a unit of Canada’s CI Financial Group. “Yields will climb further and make it harder for central banks to control their yield curves, which will certainly create headwinds for equities and make them vulnerable to a reasonably significant correction.”

No Fear for EM

While higher Treasury yields have traditionally triggered a selloff in emerging market bonds and currencies, 2021 may prove different, according to strategists. Because the recent climb is linked to improved economic prospects, it’s also positive for developing nations, said Khoon Goh, head of Asia research at Australia and New Zealand Banking Group Ltd. in Singapore.

“With the Fed expected to keep policy very accommodative for some time, there is nothing for EM to fear at this stage,” Goh said.

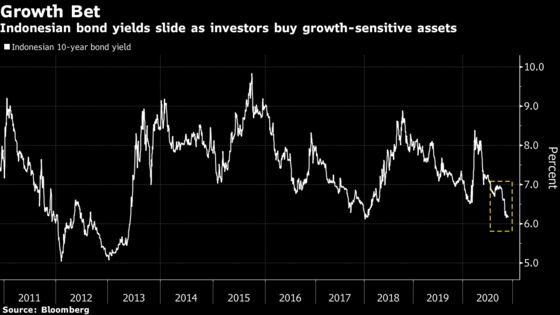

Case in point is Indonesia, whose 10-year bond yield plummeted to a 2018 low last month as investors snapped up higher-yielding and growth-sensitive assets. The rupiah is also Asia’s best-performing currency over the past month, rallying more than 3.6% against the dollar.

Most Asian currencies are also likely to “face a limited impact or even strengthen against the dollar,” said Mitul Kotecha, a senior emerging-markets strategist at TD Securities in Singapore. “Higher U.S. yields could be a reflection of stronger U.S. economic prospects, which would be beneficial to Asian economies, but would be less supportive of the dollar.”

Gold Hold

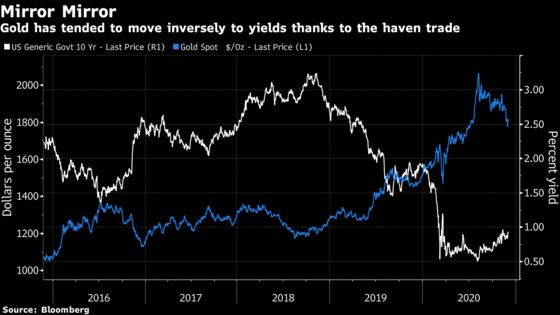

The outlook is a little less certain for gold.

If a rise in Treasury yields to 1% or higher “is due to a reflation trade, then inflation breakevens -- gold and gold miners, commodities, will do well usually,” according to Societe Generale SA strategist Sophie Huynh.

But further gains in yields might also hurt the yellow metal as demand for haven assets wane, according to Ken Peng, head of Asia investment strategy at Citigroup Inc.’s private-banking arm.

“Say we go to 1.5% on the 10-year yield, then you’re likely to see gold below $1,800, closer to $1,700,” Peng said. Gold gained a second day to trade just above $1,820 an ounce on Wednesday.

Credit Bonanza

Like equities, the credit market may also stand to gain from higher Treasury yields.

Debt investors have been clamoring for longer-term U.S. corporate bonds as stimulus spending bolsters risk appetite, sending spreads on notes maturing in 10-years or more to their tightest since February.

Credit spreads should remain tight as long as the move higher in Treasury yields is due to a reflation trade, SocGen’s Huynh said.

Dollar Hit

Higher Treasury yields could end up weighing on the world’s reserve currency.

Should the U.S. yield curve steepen as inflation expectations rise, “this will incentivize investors to currency hedge,” Citigroup Inc. strategists including Calvin Tse wrote in a recent note. Moves by investors to shield from currency fluctuations in U.S. investments could see the dollar fall by as much as 20% next year, they said.

Goldman Sachs Asset Management’s James Ashley, who also sees potential for more curve steepening, is forecasting a weaker dollar against emerging currencies such as China’s yuan.

Fed Reaction

The Fed is currently buying about $120 billion in Treasuries and mortgage-backed bonds every month, partly aimed at lowering borrowing costs for businesses and households.

Longer-term bets around Treasuries and their ripple effects on other asset classes may hinge on “how the Fed communicates,” said Citi’s Peng. “There’s a huge amount of inertia in terms of positioning that’s prevented higher yields -- that’s fine when we’re in a recession, but not when we’re in proper recovery mode.”

©2020 Bloomberg L.P.