Treasury Rally Gets Supercharged by Pension, Insurer Hedge Flows

Treasury Rally Gets Supercharged by Pension, Insurer Hedge Flows

(Bloomberg) -- This year’s blockbuster rally in Treasuries has been driven by a plethora of factors from haven demand to hedging flows. One of the most important in the latest leg has been hedging from pension funds and insurers.

These so-called liability-driven investors have been stung into action as the slide in longer-maturity bond yields has been mirrored by lower swap rates. As pension funds and insurers typically discount their future liabilities by using swaps, the decline in swap rates has increased the present value of their liabilities, unbalancing their asset-liability mix.

One way to fix this is to enter the swap market and receive swaps -- i.e. collect fixed rates and pay floating ones -- which enables the funds to boost income without spending a large amount of cash, which they would need to do if they bought cash Treasuries. The downside is these new swap transactions have in turn helped drive down swap rates and U.S. Treasury yields even further.

This feedback loop may last for a while yet. “The strategic asset allocation flows from liability-driven investors may still have a long way to go,” Bank of America New York-based strategists Carol Zhang and Olivia Lima wrote in a research note last week.

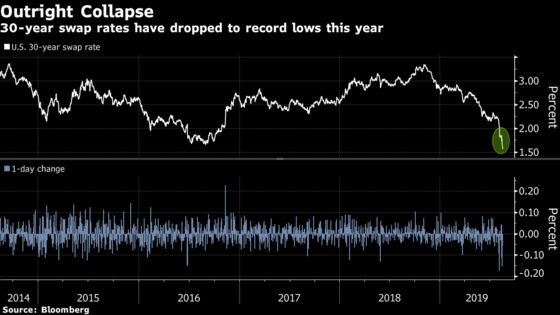

Record Lows

Thirty-year Treasury yields slid to a record-low 1.91% on Thursday from as high as 2.67% in the middle of July. The rate on the U.S. 30-year swap has tumbled even faster, dropping to an all-time low 1.51% from last month’s high of 2.34%.

The larger move in the swap rate than the Treasury yield is a footprint left from flows in swap markets, and is a sign that liability-driven investors such as pension funds and insurers are behind the move.

This is one way in which this month’s Treasury rally differs from that seen in the first quarter. The earlier episode was led by the five-year sector and was partly driven by investors using swaps to hedge positions related to mortgages and interest-rate volatility.

That earlier move had caused the U.S. yield curve to steepen, whereas now the curve has flattened to such an extent that the two- to 10-year spread became inverted this week for the first time since 2007.

--With assistance from Todd White and Elizabeth Stanton.

To contact the reporter on this story: Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Nicholas Reynolds, Cormac Mullen

©2019 Bloomberg L.P.