Treasuries on the Edge of 2% as Momentum Funds Eye the Exits

Treasuries on the Edge of 2% as Momentum Funds Eye the Exits

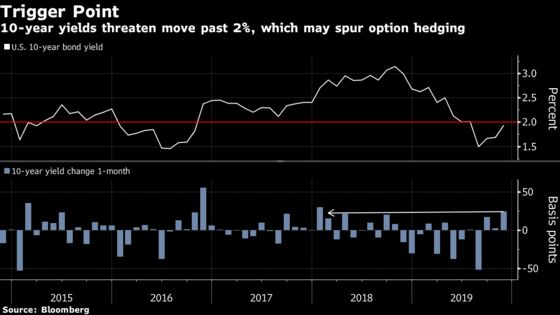

(Bloomberg) -- Benchmark Treasury yields are on the brink of a break above 2% as a global reflation trade gathers pace. Momentum-chasing funds and option hedging could be what puts them over the edge.

The unwinding of long positions by funds commonly known as Commodity Trading Advisors, and hedging activity from investors with mortgage portfolios sent 10-year yields through the 1.9% level last week. Next stop is 2%, a level which could lead to a bigger sell-off, according to Goldman Sachs Group Inc. The benchmark 10-year yield climbed as high as 1.97% last week and was steady at 1.94% in New York trading Tuesday.

“Investors appear to have built up sizable options positions that would be adversely affected by a move higher in yields from current levels,” Goldman strategists including William Marshall wrote in a recent note. “A further sell-off leading to a range break could see a modest mechanical acceleration of the move.”

Renewed optimism for a U.S.-China trade deal, and a dialing back of expectations for more Federal Reserve rate cuts have sparked a sell-off in global sovereign bonds in the past month. That was seen as a trigger for CTA funds to close their long Treasuries positions, built up during the rally earlier this year.

“CTAs are holding a clearance sale on their remaining long futures positions,” Masanari Takada, a quant strategist at Nomura Holdings Inc., wrote in a Nov. 11 note. The break of 1.90% in 10-year Treasuries was key, as this was the average entry level for the funds’ bond purchases since April, he added.

These funds were probably behind the sell-off in Japanese bonds last week, according to positioning data, when yields had surged by the most since 2013.

Convexity Hedging

The bond slump has triggered other market dynamics which are exacerbating the move. Convexity hedging - when mortgage portfolio managers buy and sell bonds to manage their duration exposure -- is back in play.

Unlike earlier in the year however, the flows are going the other way, with the investors needing to sell bonds to lower duration, rather than make purchases as yields fall.

The flattening of the yield curve and widening of swap spreads are evidence that convexity hedging was behind the recent Treasury sell-off, Priya Misra, global head of rates strategy at TD Securities, wrote in a note last week.

“With the Fed no longer buying mortgage-backed securities and allowing more mortgages to move into private hands, convexity hedging needs are much higher than in the past 10 years and should continue to grow,” she said.

--With assistance from Gregor Stuart Hunter.

To contact the reporter on this story: Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen

©2019 Bloomberg L.P.