Treasuries Curve Steepens to 2015 Levels With a Bump From BOE

Treasuries Curve Steepens to 2015 Levels With a Bump From BOE

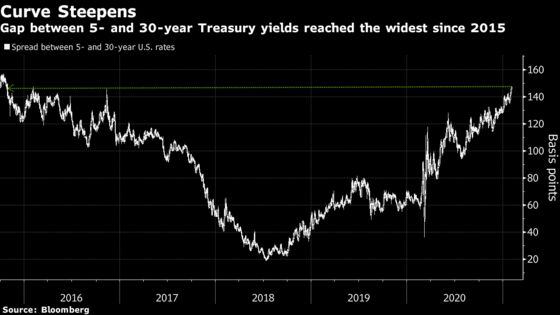

(Bloomberg) -- The reflation trade is revving up again, as a key segment of the Treasuries yield curve steepened further Thursday, taking out yet another historic level as it hit a mark last seen in October 2015.

The latest steepening push -- in which the gap between 5- and 30-year yields approached 148 basis points -- was led by the U.K. bond market, where longer-maturity debt weakened following a Bank of England policy announcement. The central bank said the U.K. economy is heading for a rapid rebound amid a bold vaccination effort.

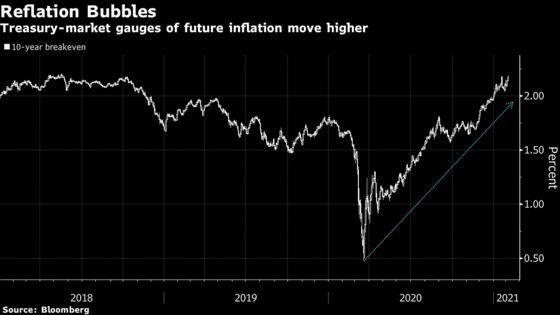

The U.S. curve has been steepening since July, but the momentum picked up early this year. Drivers include improving prospects for another round of pandemic-relief spending as well as rising expectations for consumer-price gains, reflected in higher breakeven rates for inflation-linked debt. Oil’s climb to a one-year high has also fed into the underperformance of longer-maturity debt, which is more vulnerable to the eroding effects of accelerating inflation.

“The reflation trade has been gradually playing out,” said Tracy Chen, a portfolio manager at Brandywine Global Investment Management LLC. “Growth prospects are really gaining momentum. If you look at the gradual rollout of this vaccine, by September we may be able to reach herd immunity. And at the same time we have this upcoming stimulus package, so there’s a lot of good news coming on board.”

The U.S. 30-year yield got within a whisker of 1.95%, exceeding its peak from the market chaos of March to reach the highest since February last year. Ten-year U.S. breakeven rates -- a market proxy for the expected annual inflation rate over the next decade -- touched 2.19%, the highest since May 2018.

Chen predicted long-term yields would keep rising, with the U.S. 30-year yield “easily” getting to 2% this year. Among the ways she’s positioning for quicker growth and inflation is by betting on a weaker dollar.

The rise in long-term U.S. government bond yields is still being tempered by support from the Federal Reserve, which is buying around $80 billion a month of Treasuries. Fed officials this week sent another strong signal that they aren’t close to ready to reduce their bond purchases.

“Rates will be pressured higher here, but to a limit,” said Greg Peters, head of PGIM Fixed Income’s multi-sector and strategy. “My initial call for 10-year yields was for a rise to 1.20% but it could get to as high as 1.5%. But the rise thereafter is not sustainable.”

The overarching reason he sees a limit to the increase: the massive debt overhang that will be the legacy of the pandemic, and the drag he expects that to have on growth and inflation. The 10-year rate was last at 1.14%.

In the U.K. on Thursday, the gap between 5- and 30-year gilt yields widened to 97 basis points, the steepest since 2018.

The Bank of England pushed back market expectations for further monetary easing, stressing a move to negative territory isn’t imminent. Investors also noted Deputy Governor Dave Ramsden’s statement that he sees a slowing pace of bond purchases later in the year.

Thursday’s selloff in Treasuries also came as a report showed applications for U.S. state jobless benefits fell last week to the lowest level since the end of November, a sign that ebbing virus infections may be buoying economic activity. Oil futures, meanwhile, climbed above $56 a barrel in New York after closing at the highest level in more than a year.

“A lot of the move higher in rates is coming from rising inflation expectations,” said Peter Boockvar, chief investment officer for Bleakley Advisory Group. “The market is looking at oil trading at $56, showing that inflation is percolating, and there’s more government spending coming. Growth is also headed in the right direction due to the vaccine.”

©2021 Bloomberg L.P.