Trade-War Scenarios Send Investors Scurrying to Rewrite Playbook

The new plans seem to still be works in progress, written in pencil rather than ink.

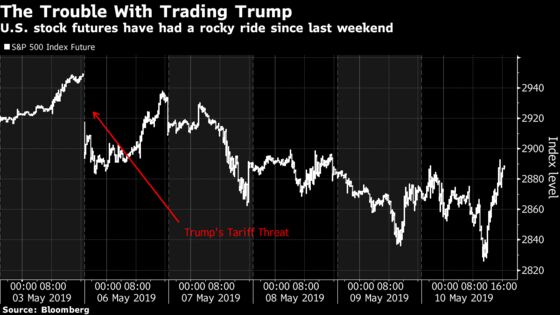

(Bloomberg) -- All it took was two lunchtime tweets last Sunday, sandwiched between posts complaining about the results of the Kentucky Derby and another gripe about “Angry Democrats,” for investors around the world to rip up their playbooks for 2019.

What has replaced those playbooks now that U.S. President Donald Trump has made good on his Twitter threats to boost tariffs on $200 billion of imports from China? Well, the new plans seem to still be works in progress, written in pencil rather than ink.

Exactly what has been priced into markets from the escalation of trade tensions -- and what still needs to be priced in -- is a riddle that investors the world over are urgently trying to solve. And, frustratingly, attempts at answers tend to come in three parts, depending on whether this latest escalation of tensions manages to trigger a trade agreement in the near term, a longer period of back-and-forth brinkmanship, or a full-blown trade war.

“The FX market is pricing trade tensions but not a trade war,” Bank of America economists led by Ethan Harris wrote in a note. “Importantly, the markets could view brinkmanship as similar to a trade war in the short run. By contrast, we think the rates market is already pricing in something like the brinkmanship scenario,” which could continue for weeks.

A U.S.-China agreement in the near term naturally would provide the best chance for traders to pick up the scraps of their old playbooks and tape them back together. Trump offered some hope of that scenario on Friday afternoon by announcing -- on Twitter, of course -- that this week’s talks with China were “constructive” and his relationship with Chinese President Xi Jinping remains “a very strong one.” But the two countries nonetheless remain deadlocked.

The chance of a prolonged period of tensions has strategists conjuring up a wide variety of investment ideas. Credit Suisse suggested a trade that benefits should the iShares MSCI Emerging Markets ETF fall between 4.5% and 8% over the next month, while UBS Global Wealth Management decided to end its recommendation to overweight emerging-market hard-currency sovereign bonds.

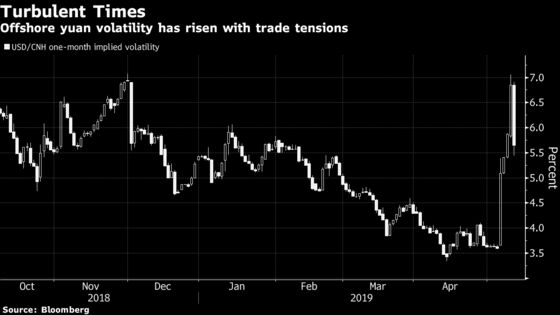

The consensus appears to have gravitated toward the idea that prolonged or escalated tensions would cause this past week’s trends to continue: weakness in emerging-market currencies and global equities, gains in haven assets such as the Japanese yen and U.S. Treasuries, and heightened volatility just about everywhere. China’s yuan, Thailand’s baht and the Philippine peso are the most at risk in a trade war, according to a Bloomberg Intelligence model.

Before the tweets heard ’round the world, a central thesis in markets was that a trade deal and economic stimulus in China would boost riskier assets at the expense of havens, causing Treasury yields to rise in the second half of the year, Jim Caron, fixed-income portfolio manager at Morgan Stanley Investment Management, said in an interview.

“Now the thesis is that, based on what we’re seeing right now, it seems as though China has backed out of a deal and why that’s significant is that this isn’t just something that can be fixed by a tweet -- he just can’t untweet that,” Caron said. Looking ahead, he said, “I’d argue that we have to believe that the surprises in the market are going to be more toward the downside than the upside.”

He’s not the only one bracing for more risk aversion. Investors need to be ready for the trade war to get worse before it gets better, risking further weakness in stocks that were already vulnerable after strong gains to start the year, Shane Oliver, head of investment strategy and chief economist at AMP Capital, wrote in a note. Miller Tabak & Co. equity strategist Matt Maley sounded a similar note of caution and said that a 10% drop in the S&P 500 Index from its recent high would not be out of the question. So far, the gauge has fallen less than 3% from its record high close at the end of April.

“The stock market was already ripe for a pull-back,” Maley wrote to clients. “Now that it’s getting some negative news -- materially negative news -- it’s even more ripe for a larger decline. Therefore, we believe investors should not be trying to figure out whether the market will decline or not. They should be trying to figure out how much it will fall.”

Meanwhile, although U.S.-China scenario analyses dominated the past week, focus could quickly shift. Janelle Woodward, head of fixed income at BMO Global Asset Management, has an eye on the next potential target for tariffs: European automakers. The Trump administration was expected to make a decision on the findings of a probe into the national security risks of European auto imports by May 18.

“We think there are a lot of options as far as extension or asking for a new investigation, but this does seem something that hasn’t gotten a lot of press given the situation with China,” she said.

And that’s a situation that remains far from resolved. With U.S. Treasury Secretary Steven Mnuchin confirming that there are, right now, no fresh talks on the calendar, investors look set to remain at the mercy of left-field pronouncements on trade by Trump and others.

“The uncertainty of policy outcomes complicates the calculus for portfolio managers,” said Matt Peron, chief investment officer of City National Bank, which manages $39 billion in stocks and fixed-income assets. “We know the scenarios, but placing probabilities on outcomes becomes very difficult. In addition, there are retaliatory responses and offsets that make so-called ‘second order’ effects unpredictable.”

To contact the reporters on this story: Michael P. Regan in New York at mregan12@bloomberg.net;Emily Barrett in New York at ebarrett25@bloomberg.net;Vivien Lou Chen in San Francisco at vchen1@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Jenny Paris

©2019 Bloomberg L.P.