Trade Reality Set to Bite European Exporters Again

Trade Reality Set to Bite European Exporters Again

(Bloomberg) --

A not-so-dovish tone from the Fed had already hit the mood earlier this week, and now with Trump’s latest trade bombshell, European stocks are on track for some serious damage heading into the weekend.

Expectations of central-bank easing have allowed equity traders to brush off the deteriorating macro economic backdrop and trade tensions. But the new tariffs and the lack of improvement in the economic outlook could finally bite. Despite no earnings growth so far this year globally, expectations are still high for the rest of the year, and the consensus looks too optimistic for the fourth quarter, HSBC strategists say.

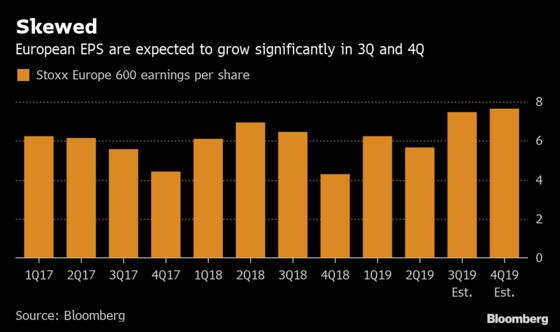

Looking at EPS estimates for the Stoxx Europe 600, the strong earnings figures expected for the second half of 2019 is also at odds with the seasonality observed in the past two years.

HSBC sees the consensus EPS skewed to the fourth quarter, with about 10% growth expected for most regions. Their analysis of 60,000 corporate earnings calls globally paints a gloomy picture, with the impact from tariffs looking worse than originally anticipated. On top of that, the occurrence of the word “destocking” by U.S. firms has reached its highest level since the financial crisis, making a near-term resolution of trade tension a necessary condition to avoid further earnings pressure.

The problem is, the U.S. and China still seem to be playing the blame game, while a fall in global trade volumes is hitting exporters in the U.S. and emerging markets. So far, European exporters have shown some earnings resilience, with estimates standing at 6% growth this year, according to HSBC strategists. This may not last, they say, as a further decline in global trade, autos tariffs and Brexit provide downside risks.

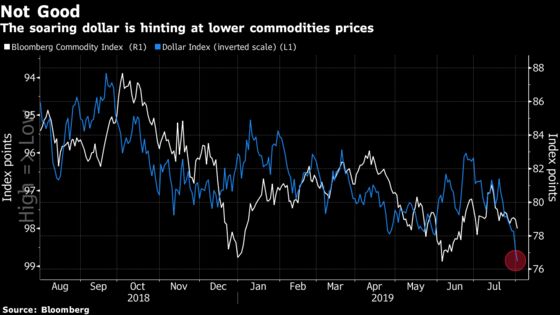

The strong dollar/weaker euro should keep providing some support to European exporters for now, as the Fed doesn’t seem too keen on weakening the currency. The flip side is it may have consequences for miners and oil companies, the biggest underperformers yesterday. Mining stocks need positive trends in commodities prices, and at the moment, the dollar is not supportive. The Dollar index touched a two-year high yesterday and is hinting at further weakness.

Credit Suisse strategists remain positive though, and recommend staying overweight on the mining sector, as China’s manufacturing investment should stabilize and valuations aren’t demanding.

Things could change in the coming months. “There is something exciting about looking at EURUSD these days,” writes Nordea Senior Macro strategist Sebastien Galy. The market is likely to have priced in rate cuts until September, but beyond that, innovative measures from the ECB on bank debt should invert the trend, while falling U.S. inflation could push the euro toward the $1.16 level, he says. It’s just above $1.10 currently.

In the meantime, Euro Stoxx 50 futures are trading down 2% ahead of the open.

- Watch trade-sensitive sectors after President Donald Trump announced a further set of tariffs on $300b worth of Chinese goods not already levied. Watch miners, steelmakers, semiconductors, autos and other cyclical segments like industrials and chemicals.

- Watch the pound and U.K stocks after the Bank of England decision on Thursday left markets confounded and likely only adds further to the uncertainty as the central bank effectively decided not to assume no-deal outcomes in its forecasts, even as markets do just that. Separately, the government’s majority has been cut to one after a special-election defeat.

COMMENT:

- “The new tariffs are doubly difficult for Germany, whose manufacturing sector has been in recession all year, and is especially export dependent,” Michael Hewson, chief market analyst at CMC Markets U.K., wrote in a note. “Faced with the prospect of more trade disruption and a European Central Bank short on remedies, Europe could be facing an existential crisis before the end of the year.”

COMPANY NEWS AND M&A:

- Allianz Second-Quarter Operating Profit Beats Highest Estimate

- Credit Agricole Posts 2Q Net In Line With Ests.; 2Q Rev. Beats

- BP Has $13B Assets It ‘Can Sell’ to Reach Disposal Target: CFO

- IAG 2Q Adj. Op. Profit Beats Est.; BA to Appeal ICO Fine

- Lanxess Second Quarter Adjusted Ebitda 1.8% Above Estimates

- Saipem Enters JV for Arctic LNG2 With Project Quota About EU2.2b

- Vonovia 1H FFO Rises; Still Sees 2019 FFO EU1.17-1.22b

- Rio Tinto Awards Over A$250M of Contracts for West Angelas Mine

- Mercedes Bests BMW for the First Time in Months, Narrowing Race

- Telecom Italia Second Quarter Revenue 1.1% Below Estimates

- Natixis Fixed Income Trading Rebounds as Riahi Caps Tough Year

- Natixis CEO Riahi Says H2O Funds Performance Remains ‘Very Good’

- Enel 1H Adjusted Net Rises to EU2.28b, Guidance Confirmed

- Balfour Beatty Signs $780M Construction Pact in Ft. Lauderdale

- Pirelli Cuts FY Revenue Growth View, 1H Revenue Matches Est. (1)

NOTES FROM THE SELL SIDE:

- Pirelli’s reduction of 2019 guidance on revenue, Ebit margin, price mix and net financial position indicates further slight consensus downgrades but won’t shock market completely, Morgan Stanley (overweight, PT EU7) writes in note.

- SocGen shares could re-rate amid progress in commercial and investment banking, and on capital generation and costs, according to analysts at Citi; upgrades to buy from neutral (PT EU28).

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 397.9 (May 2018 high); 403.7 (2018 high)

- Support at 383.5 (50-DMA); 374.5 (61.8% Fibo)

- RSI: 51.1

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,549 (July high); 3,596 (May 2018 high)

- Support at 3,445 (50-DMA); 3,403 (61.8% Fibo)

- RSI: 50.1

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Equinor upgraded to neutral at Goldman; Price Target 210 Kroner

- Kone Oyj upgraded to neutral at JPMorgan; PT 48.50 Euros

- LSE upgraded to add at AlphaValue

- SocGen upgraded to buy at Citi

DOWNGRADES:

- BAE downgraded to hold at SocGen; PT 5.93 Pounds

- Fresnillo downgraded to hold at HSBC; PT 6.90 Pounds

- Galp downgraded to sell at Goldman; Price Target 18 Euros

- MS Industrie downgraded to hold at Montega; PT 3.30 Euros

- Pirelli Downgraded to Neutral at Mediobanca SpA; PT 6 Euros

- Premier Oil cut to equal-weight at Barclays; PT 1.20 Pounds

- Scibase downgraded to hold at Pareto Securities; PT 6.40 Kronor

- Vinci cut to sell at Insight Investment Research; PT 113 Euros

INITIATIONS:

- Digital Value rated new outperform at Mediobanca SpA

- Fevertree Drinks rated new neutral at Citi; PT 26 Pounds

MARKETS:

- MSCI Asia Pacific down 1.4%, Nikkei 225 down 2.1%

- S&P 500 down 0.9%, Dow down 1%, Nasdaq down 0.8%

- Euro down 0.02% at $1.1083

- Dollar Index up 0.01% at 98.38

- Yen up 0.2% at 107.13

- Brent up 2.2% at $61.9/bbl, WTI up 1.9% to $55/bbl

- LME 3m Copper down 1.2% at $5831/MT

- Gold spot down 0.9% at $1432.6/oz

- US 10Yr yield little changed at 1.89%

ECONOMIC DATA (All times CET):

- 9am: (SP) July Unemployment Change, est. -22,500, prior -63,805

- 10am: (IT) June Industrial Production MoM, est. -0.3%, prior 0.9%

- 10am: (IT) June Industrial Production WDA YoY, est. -0.8%, prior -0.7%

- 10am: (IT) June Industrial Production NSA YoY, prior -0.7%

- 10:30am: (UK) July Markit/CIPS UK Construction PMI, est. 46, prior 43.1

- 11am: (EC) June PPI MoM, est. -0.3%, prior -0.1%

- 11am: (EC) June PPI YoY, est. 0.8%, prior 1.6%

- 11am: (EC) June Retail Sales MoM, est. 0.3%, prior -0.3%

- 11am: (EC) June Retail Sales YoY, est. 1.3%, prior 1.3%

- 11am: (IT) June Retail Sales MoM, prior -0.7%

- 11am: (IT) June Retail Sales YoY, prior -1.8%

* For a wrap on developments in Europe’s equity capital markets, click here.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editor responsible for this story: Blaise Robinson at brobinson58@bloomberg.net

©2019 Bloomberg L.P.