Trade Fears Are Robbing Stocks of Their Tax-Cut Gains

“Tariff Man” Donald Trump is close to squandering all of the gains of his tax cut, at least as far as the market is concerned.

(Bloomberg Opinion) -- “Tariff Man” Donald Trump is close to squandering all of the gains of his tax cut, at least as far as the market is concerned.

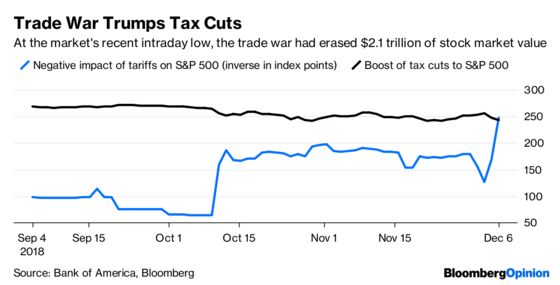

At the stock market’s low on Thursday, when the S&P 500 Index was down about 3 percent, the president’s trade war had zapped as much as $2.1 trillion in collective market cap from the companies in the index, which are nearly all of the largest corporations in America, according to estimates from Bank of America. That’s about $100 billion more than the amount many have estimated the tax cuts would boost the economy in a decade. It is also nearly the same amount that the tax cuts appear to have boosted the stock market, according to my estimates.

Stocks rallied Thursday afternoon on anticipation that the Federal Reserve may put off future interest rate increases, and shares ended down less than 1 percent, putting the net impact of Trump’s two signature economic policies back in positive territory. But another leg down in the stock market could quickly flatten any lasting remnant of the Trump Bump. What’s more, it makes clear just how much damage investors think the trade wars could be doing to the economy.

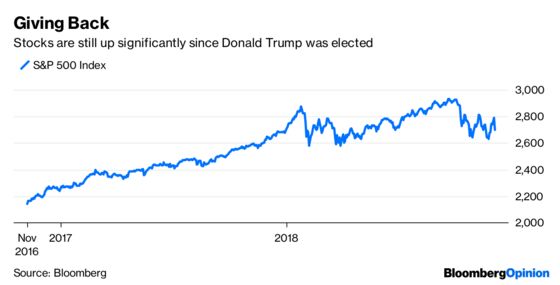

When Trump was elected, it was clear to most strategists that his mix of calls for fiscal stimulus — like tax cuts and infrastructure spending — and protectionism — like tariffs and immigration restrictions — could pull the market in different directions. Early on, investors were eager to bet that Trump would either not follow through on his protectionist urges or that the impact of the tax cuts would outweigh them. Recently, that looks to have been a bad bet. The stock market has plunged 7.5 percent in a little more than two months, as measured by the S&P 500, though stock prices are still up significantly from when Trump was elected. However, much of that is most likely due to higher earnings, not Trump’s policies. The multiple that investors are willing to pay for stocks is significantly lower than it was when Trump won office.

The entire drop in the stock market can’t be attributed solely to trade fears, of course, but they appear to be a significant driver. A counterargument can be made that investors are underestimating the benefits of the tax cut and exaggerating the drawbacks of the trade war. For instance, tax cut proponents have pointed to this year’s uptick in companies that have pledged to increase capital expenditures, which could bolster the economy’s productivity. But on a call with reporters on Thursday, Bank of America’s co-head of global economic research, Ethan Harris, said that a number of companies have put those capital expenditures on hold in light of trade tensions. Harris estimated that as much as half of what has been pledged may not get spent.

In June, former Goldman Sachs executive and White House economic official Gary Cohn predicted that tariffs and trade disputes could wipe out all of the gains of the tax cuts. At the time, that seemed like an overly dire prediction. Now he appears prescient, and stock investors should heed his warning.

To determine the tax-cut boost, I calculated how much of this year's earnings gains have come from the lower corporate rate based on analysts' estimates before and after the tax cut. That turned out to be $15 of the $159.40 that S&P 500 companies are collectively expected to earn per share in 2018. I multiplied that $15 by the current price-to-earnings multiple of the S&P 500 based on 2018 earnings. As of the market's low on Thursday, the tax cut still appeared to be providing the S&P 500 with a 243-point boost.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2018 Bloomberg L.P.