Fed’s Best Effort to Guide Rates Market Undone by Trade and Tantrums

Hopes that the central bank could guide markets to a cool-headed assessment of the U.S. economy now look precarious.

(Bloomberg) -- Any reassurance markets got from the Federal Reserve in Jackson Hole on Friday was wiped out within minutes. A volley of acrimonious presidential tweets and a nastier turn in the trade war sent Treasury yields, stocks and the dollar skidding into the weekend.

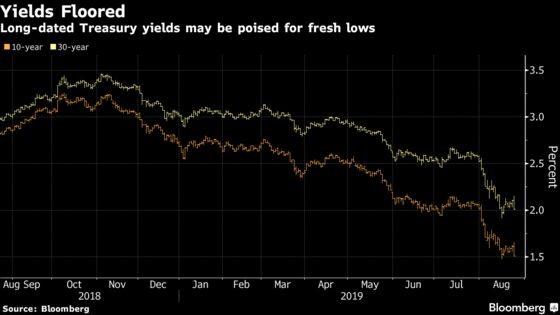

Hopes that the central bank could guide markets to a cool-headed assessment of the U.S. economy now look precarious. Chairman Jerome Powell had barely finished speaking at the Fed’s annual event when President Donald Trump unleashed a Twitter tirade against his appointed Fed chief. The 10-year yield slid back to 1.5%, stocks tumbled and the greenback sank toward its 2019 lows versus the yen.

The moves came as the leader of the world’s largest economy took to social media to order U.S. companies to start looking for alternatives to making products in China. Markets shuttered for the week just before the president announced another ramp-up in tariffs on China. The drama could escalate further this weekend in France, with what could be another tense Group-of-Seven gathering.

“One hundred percent of the focus for the next few days is going to be on the trade war,” said Gary Cameron, head of the U.S. rates team at Garda Capital Partners. “There’s going to remain a bid in U.S. Treasuries. It’s paid to buy the dip all year long.”

At this rate, the fixed-income portfolio manager expects that the Fed policy rate is headed to zero. He says markets are calling the path right for this year. Futures are priced for the Fed’s target to fall about 64 additional basis points by the end of December.

And in Cameron’s view it’s not just the weight of global events dragging yields lower -- investors are also increasingly worried about cracks in the U.S. economy.

The risks were on display this week with U.S. purchasing managers indexes suggesting factory output may now be shrinking, and the dominant services sector barely expanding. That’s got investors worried about the rest of the year.

This is a tough set-up for what was starting just days ago to look like an auspicious time for investors calling the bottom in U.S. yields. The searing rallies of mid-August took long-dated yields to multi-year lows, including an all-time record for the 30-year. The action sent the 10-year yield below that on the two-year, an inversion that’s reliably signaled recession is on the way. That portion of the curve ended the week roughly flat.

“It’s hard to get rates much higher in the near-term really,” said Priya Misra, head of global rates strategy at TD Securities in New York. “Global growth and trade uncertainty seem to be here to stay.”

What to Watch

- The Group of Seven meets in Biarritz, France, for a weekend gathering that will spill over into an appearance by the U.S. president early Monday New York time

- Fed commentary is thin post-Jackson Hole

- Aug. 28: Richmond Fed’s Thomas Barkin speaks in West Virginia; San Francisco Fed’s Mary Daly addresses conference in New Zealand

- Here are some of the highlights of the economic calendar

- Aug. 26: Chicago Fed activity index; durable, capital goods orders; Dallas Fed manufacturing activity

- Aug. 27: Home price indexes; Richmond Fed manufacturing index; Conference Board consumer confidence

- Aug. 28: MBA mortgage applications

- Aug. 29: GDP; trade balance; retail, wholesale inventories; initial jobless claims; Bloomberg consumer comfort; pending home sales

- Aug. 30: Personal income, spending; PCE deflator; MNI Chicago PMI; U. of Mich. sentiment

- On the auction block

- Aug. 26: $45 billion 3-month bills, $42 billion 6-month bills

- Aug. 27: $40 billion 2-year notes

- Aug. 28: $18 billion 2-year floating-rate notes reopening; $41 billion 5-year notes

- Aug. 29: 4- and 8-week bills; $32 billion 7-year notes

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum

©2019 Bloomberg L.P.