The Secret of How Top Japan Fund Beat 99% of Peers

Top Japan Fund Beats 99% of Peers Focusing on Skin in the Game

(Bloomberg) -- When a years-long father-daughter feud over who took leadership of a Japanese furniture retailer threatened to drive the company into the ground, one top-performing fund manager took it as a reason to celebrate.

That’s not because he was shorting the stock, but because the negative publicity would temporarily damage the image of firms in his niche area of investing, and give him opportunities to go against the crowd.

Jumpei Kitahara invests only in Japanese companies whose management owns at least five percent of the outstanding shares. He says these owner-managed or family-run firms already have a bad reputation among Japanese investors, and the drama at Otsuka Kagu Ltd. only gave him more chances to buy.

"You can’t win unless you do what others aren’t doing," the 38-year-old fund manager for Tokio Marine Asset Management Co. said in an interview in Tokyo.

Kitahara’s strategy seems to be working. The Tokio Marine Japan Owners Fund has beaten 99 percent of peers since it was established in 2013, with a 26 percent annualized return over that time, according to data compiled by Bloomberg. The fund, which is targeted to Japanese individuals, has more than $140 million in assets.

The fund is aligned with a broader push by Prime Minister Shinzo Abe’s administration to make management more attuned to shareholders. Abe’s government also wants the country’s legions of so-called salarymen managers to have more skin in the game. Two years ago, the Ministry of Economy, Trade and Industry removed taxes on restricted stock -- a form of management compensation tied to a company’s long-term performance -- aiming to achieve just that.

Gut Assessment

Kitahara combines quantitative screening for factors such as valuation and risk with a gut assessment of management’s leadership ability. He whittles down the universe to about 100 companies, from which he picks the roughly 33 firms that he has in his fund.

"I need to fully understand what the company’s aiming to do," Kitahara said, explaining how he and his company regularly meet chief executive officers to talk about their company vision. "I don’t invest in companies that I can’t understand."

Kitahara gives the example of Japan’s largest furniture retailer, Nitori Holdings Co., which the fund has invested in since its inception. It’s helmed by Akio Nitori, who has set out a goal of reaching 3 trillion yen ($26.4 billion) in sales and opening 3,000 stores by 2032.

Nitori’s shares have surged more than fourfold since the fund started. The only risk lies in Akio Nitori’s advancing age of 74 and the question of who will succeed him. Kitahara says the fund may sell the stock if Nitori steps down.

Though Kitahara’s portfolio is relatively concentrated for a mutual fund, he says that less is more, and having fewer stocks doesn’t necessarily increase risk for investors.

“It’s better to pick good companies that you really know about, rather than investing in 2,000 firms that you don’t even know,” he said, talking of the benchmark Topix index.

Kitahara said the idea to invest in management-owned companies came during the financial crisis, when firms such as Fast Retailing Co. and Nitori thrived as others struggled.

Companies with owners at the helm can work to longer-term goals and make decisions faster than their peers, he said.

"If you’re a hired, salaryman CEO, you only serve for about three years," he said. "Owner-managers are guaranteed to lead for a decade, even two."

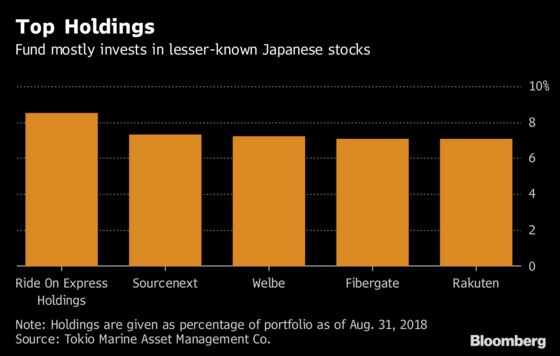

The fund has taken some big bets on companies that are unloved by the broader market. One example is Rakuten Inc., whose shares have fallen about 30 percent in the past year. The e-commerce retailer founded and run by Hiroshi Mikitani will eventually succeed in its plan to expand into the mobile-phone business, Kitahara said. In his view, the company is extremely undervalued.

Changing Goals

Of course, the fund doesn’t always get it right. It once invested in a company that operates a chain of used-car dealerships. But Kitahara became wary of the management when it deviated from its original goal and started to voice thoughts of venturing into new businesses including information technology and car sharing. "They had never even done Internet-related business before," he recalls. The fund soon sold its shares.

On the other hand, he says, owner managers can be quick to determine when a business is failing and needs review. "Even at times of sudden change, they can be flexible," Kitahara said.

But there’s no easy way to spot the kind of managers who can do this, he said. It all comes down to experience examining the top echelons of companies.

"It’s expertise that you have to build up," Kitahara said. "You can’t quantitatively measure the qualities of good management."

To contact the reporter on this story: Shoko Oda in Tokyo at soda13@bloomberg.net

To contact the editors responsible for this story: Chua Baizhen at bchua14@bloomberg.net, Tom Redmond, Sarah Wells

©2018 Bloomberg L.P.