Tokyo’s Promise of Generational Stock Revamp Draws Skeptics

Tokyo’s Promise of a Generational Stock Revamp Draws Skeptics

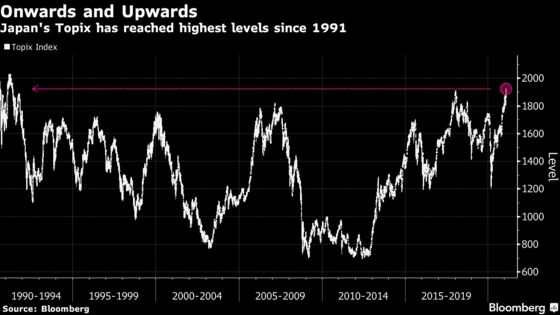

(Bloomberg) -- Japan’s Topix stock benchmark climbed to a three-decade high on Monday, drawing even more attention to its future amid plans for a sweeping market reform.

The Tokyo Stock Exchange is set to undergo a once-in-a-generation shakeup in little over a year. Japan Exchange Group Inc., which owns the bourse, plans to cut the number of market segments, apply new listing criteria and turn five confusing, overlapping divisions into three simpler sections: blue-chips, start-ups, and the rest.

A key goal seemed to have been to overhaul the Topix, whose membership has almost doubled since the 1990s to over 2,000 companies and includes more than half of Japan’s listed firms, into a much slimmer benchmark of top-performing, well-governed firms. But some are already voicing concern that the changes may not result in the dramatic transformation that had been hoped for.

One reason is that Keidanren, Japan’s powerful, industry-heavy business lobby, is likely to oppose significant changes to practices that have long made foreign investors skeptical of Japanese stocks such as cross-shareholdings, in which companies with business dealings own stakes in one another. That’s the view of Nicholas Smith, a strategist at CLSA Securities Japan Co., who wrote a report last month titled ‘Opportunity Missed.’

“It looks likely that vested interests will water down the process, moving the focus to merely ejecting the small caps” rather than corporate governance laggards, Smith said. He compared the interest in the proposed Topix changes to the hype seen for the JPX-Nikkei Index 400 in 2014, which was designed to boost investment in companies providing higher returns on equity, but received little popular pickup.

The reforms are set to funnel companies into one of three new market segments: ‘Prime,’ ‘Standard’ and ‘Growth’. The Prime segment will be equivalent of the current first section of the exchange, from which the Topix is now composed. Among the criteria for entry into Prime is at least 10 billion yen ($94.7 million) in “tradable share market capitalization,” a somewhat opaque term which excludes stock held by large shareholders, treasury shares and other types of stock not freely available.

| Prime | Standard | Growth | |

|---|---|---|---|

| What companies? | Large market cap, attracting institutional investors, higher governance standards | Basic market cap, basic governance standards | High growth potential |

| Tradable shares market cap requirement | 10 billion yen | 1 billion yen | 0.5 billion yen |

| Tradable share ratio requirement | 35% | 25% | 25% |

Source: Japan Exchange Inc. Other requirements also apply.

Ticking Boxes

“Topix will remain 99% the same as before,” Travis Lundy, an analyst at Quiddity Advisors who publishes on Smartkarma, wrote in a note dated Jan. 21. The changes are “in the grand scheme of things, small.”

Being on the TSE First Section carries cachet in Japan -- a name value similar to being listed a Fortune 500 company. “First Section-listed” is a shorthand for a company that’s trustworthy and stable.

Lundy expects few companies would rule themselves out. “It would look bad,” he wrote. “So they will tick the boxes and meet the requirements and Japan will pat itself on the back for a job well done and let’s revisit again in twenty years.”

Not many First Section stocks fall below the 10 billion yen cutoff, Lundy calculates, so that even if 500 or so companies are removed from the Topix, the gauge would still have more than 1,500 members -- “About 3 to 5 times the number of names in any major global blue chip index,” he writes.

While the market restructuring will take effect as of April 1, 2022, transition into the new Topix is a longer process expected to run until early 2025.

‘Significant Message’

Some are hopeful about the changes proposed in the overhaul.

The new calculation methods for tradable shares “do relay a significant message that strategic shareholdings will be targeted,” said Atsushi Kamio, a researcher at Daiwa Institute of Research. “For companies with banks and insurers having a stake, it could lead to share sale in the short-term to meet the new listing requirements.”

The next step toward reform will come in spring, when Japan’s corporate governance code will be revised. A working panel at the Financial Services Agency is discussing revising the code to push companies to have external directors make up one-third of their boards, as well as voluntary goals on female and non-Japanese appointments.

©2021 Bloomberg L.P.