Hedge Fund Titans Aurelius and Elliott Clash in Distressed Deal

Hedge Fund Titans Aurelius and Elliott Clash in Distressed Deal

(Bloomberg) -- Years after leaving the New York-based hedge fund Elliott Management Corp., Mark Brodsky often found the firm he later started, Aurelius Capital Management, aligned with his old employer. The two fought side by side in many high-profile trades including a grueling, decade-long battle with Argentina over defaulted bonds.

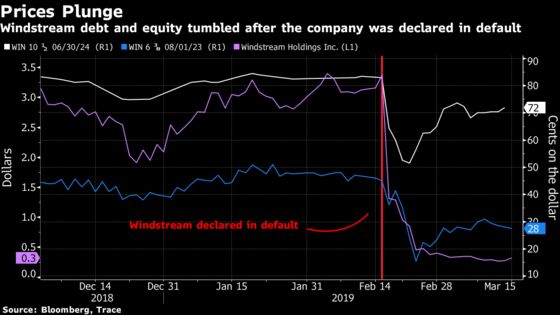

But now Brodsky finds himself at odds with Elliott -- and his former boss there, Paul Singer -- in a new controversial default saga. This one centers on Windstream Holdings Inc., a U.S. telecom company that suddenly sank into default last month after Judge Jesse Furman ruled in favor of Aurelius’s lawsuit against the company for breaking bond covenants.

Aurelius is believed by market participants to have bought derivatives insuring against a Windstream default, with Elliott taking the other side of that trade. That would hand Aurelius a payout on the contracts, known as credit-default swaps, while Elliott could be faced with losses. Moreover, as Windstream begins to navigate bankruptcy proceedings, Aurelius and Elliott have what would appear to be very different agendas.

Aurelius, which started the year with $2.4 billion in assets, likely remains focused until the auction on preserving its CDS return. Elliott, which manages about $34 billion, holds a position in Windstream’s secured debt that gives it leverage in bankruptcy negotiations.

“Given the sophistication of the players -- Aurelius and Elliott -- I think the interesting stuff starts now,” said Erik Gordon, a professor at the University of Michigan’s Ross Business School. “Nobody will do a more sophisticated analysis than these two and nobody will be more willing to fight than these two.”

Representatives for Aurelius and Elliott in New York, as well as Little Rock, Arkansas-based Windstream declined to comment.

Squaring Off

With the two hedge funds seemingly on course to sit at separate ends of the table in the bankruptcy, it puts Elliott in the position to potentially focus on recapitalizing Windstream in exchange for assets or equity. Meanwhile, Aurelius could look to challenge that move -- possibly as part of a bigger group -- and pursue its own claims against the estate. It could alternatively tender its unsecured bonds in the CDS auction scheduled for April 3 and quit while it’s ahead, opting out of the bigger bankruptcy fight.

“They can declare moral victory thanks to Judge Furman’s opinion, but you can’t declare investment victory until you actually make some money,” Minor Myers, a professor at Brooklyn Law School who specializes in corporate finance, said by phone. “And if they do that with the CDS resolution, what’s the point of fighting Elliott?”

Windstream’s 10.5 percent second-lien notes due in 2024, issued last year in a debt swap involving Elliott, have fallen about 11 cents on the dollar in the wake of the default ruling, while its shares have slid about 90 percent. The 6.375 percent unsecured notes due 2023 that were at the center of the default trial are trading around 28 cents on the dollar.

Elliott proposed a loan to keep Windstream out of bankruptcy, according to people with knowledge of the matter, and the company outlined a financing proposal it received from financial institutions for up to $1.5 billion, contingent on Windstream meeting several conditions, according to court filings.

But it was too little, too late. Windstream filed for Chapter 11 last month, just 10 days after Judge Furman ruled that a spinoff of Uniti Group Inc. in 2015 violated its bond contracts, awarding a $310 million judgment to Aurelius. Windstream accused Aurelius of forcing the company into bankruptcy through an act of “predatory market manipulation” to benefit its CDS position, while the hedge fund claimed vindication.

“The Aurelius case shows the system working better than it might have without CDS, but it is leading to a puzzling situation here,” Myers said. “In general, you want people to be enforcing bond covenants.”

The court win for Aurelius also amounted to a triumph for Brodsky, who worked for Elliott for almost a decade before leaving to start his own firm. In addition to being among creditors awarded a $4.65 billion payout fighting Argentina’s 2001 sovereign debt default (they were together branded “financial terrorists” by the country’s former president), the two funds were involved in the bankruptcy of Oi SA, a Brazilian telecom provider, Peabody Energy Corp., and in an obscure bet that brought them outsized recoveries in the bankruptcy of General Motors.

Still, in the relatively confined world of distressed debt, firms can often find themselves aligned one day, and squaring off the next.

Neighbor’s Table

At Windstream’s first-day hearing in its bankruptcy, Milbank’s Dennis Dunne, counsel for a group of Windstream second-lien creditors, echoed the company’s sentiments, arguing that Aurelius was a bad actor that had “scoured the landscape to find a default it could prosecute.”

"It’s one thing to say I’m going to buy insurance on my neighbor’s house, it’s another to burn it down,” Dunne said. “It’s a third thing to collect a ton of money on that insurance and then expect to be welcomed at my neighbor’s table.”

Windstream is scheduled to be in court March 25 for a motion to stop utility providers from shutting off service. It will return April 16 for a hearing on a broader range of motions, including the final approval of a $1 billion loan it will use to fund itself during bankruptcy.

--With assistance from Josh Saul, Katia Porzecanski and Nabila Ahmed.

To contact the reporters on this story: Allison McNeely in New York at amcneely@bloomberg.net;Eliza Ronalds-Hannon in New York at eronaldshann@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, ;David Papadopoulos at papadopoulos@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.