Three Reasons EMEA Stocks May Lead 2019 Emerging-Market Rebound

Three Reasons EMEA Stocks May Lead 2019 Emerging-Market Rebound

(Bloomberg) -- It’s where the big sell-offs begin and the big rallies arrive last. But after living in the shadows for years, the emerging Europe, Middle East and Africa region is at last coming into its own.

Since 2010, either Asia or Latin America was the star of the show whenever emerging-market equities made gains. The EMEA region was mostly the underdog, failing to lead the pack in both advances and declines. That may change this year.

Earnings Estimates

The rebound in emerging-market stocks is fragile and Asia remains a pocket of weakness. Analysts have cut their earnings estimates for the region’s companies by almost 13 percent since early April because of the uncertainty surrounding the U.S.-China trade war and less-heady expectations for technology companies. In Latin America, an election super-cycle has just ended, but there’s uncertainty around the policy directions of the new governments.

In this environment, the EMEA region -- including countries such as South Africa, Turkey and Russia -- seems relatively stable, especially compared to a tumultuous 2018. Analysts are raising its profit projections by the fastest pace of the three emerging-market zones.

Relative Valuations

Developing-nation stocks in EMEA have jumped 15 percent from a low in October. While that has sent absolute valuations to near a five-month high based on the ratio of price to estimated earnings, the region’s equities are becoming cheaper relative to the other two territories. That’s because an improving profit outlook is making current price levels attractive.

EMEA equity valuations relative to Asian companies fell to the lowest since the Taper Tantrum in 2013, boosting the case for bargain hunting.

Currency Cushion

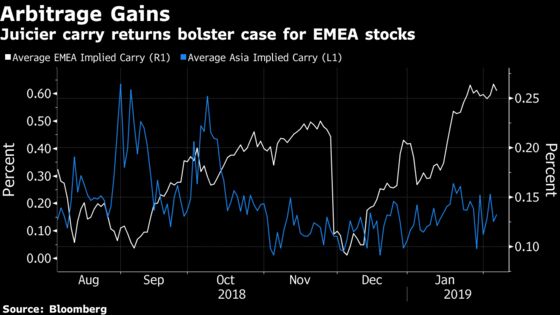

Global investors betting on EMEA stocks have often burnt their fingers because of currency volatility. But signals from forwards and options markets suggest that currencies in this part of the world may be more stable than their peers.

The potential risk-adjusted carry-trade from EMEA currencies, on average, is near the highest in 18 months, while the same measure for Asia and Latam is either falling or languishing at lower levels, based on one-month interest-rate arbitrage and implied volatility measures. This may give confidence to equity investors considering exposure to the region’s companies.

To contact the reporter on this story: Srinivasan Sivabalan in London at ssivabalan@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Alex Nicholson, Constantine Courcoulas

©2019 Bloomberg L.P.