This Year's Stock Market Got Too Hard for Anyone to Figure Out

This Year's Stock Market Got Too Hard for Anyone to Figure Out

(Bloomberg) -- It took the better part of a decade for Americans to warm to a stock rally that has created $20 trillion in wealth. Could it take just one brutal quarter and a trade war to undo their trust?

For individuals who spent the first part of the year bailing from one of the best rallies ever, the answer has often seemed like yes. Bruised by a fourth-quarter rout and made dizzy by months like May, they’ve pulled $135 billion from mutual funds and ETFs and sent most of the cash to fixed income.

On the surface, it’s a strange year to be giving up. The S&P 500 is up 11% in less than six months and sits not too far off a record, with big sell-offs usually followed by rallies.

But what has looked easy has felt harrowing -- particularly lately. Lashed by trade headlines, day-to-day market swings are getting weirdly extreme. In two different weeks this month, the Cboe Volatility Index spent time both above 21 and below 15. Before May, that had never happened in the same month, according to data compiled by Twitter user OddStats and Bloomberg.

“This has been a very good year for equity investors, but when I talk to people, I don’t hear a lot of bullishness,” said Katie Nixon, chief investment officer at Northern Trust Wealth Management, which manages about $294 billion. “In general, the individual investor is very concerned about the landscape.”

To be sure, as rough as it’s been, equities haven’t fallen apart. How, is a point of debate. Buybacks may explain it -- though they couldn’t keep $5 trillion from being blown up in December. Whoever is bidding, they’re doing it with just enough enthusiasm to keep prices aloft, making life miserable for anyone waiting for a collapse.

“They think, ‘Well, we’re just waiting for the next 50% drop,”’ Kevin Miller, the chief executive officer of Minnesota-based E-Valuator Funds, said in an interview at Bloomberg’s New York headquarters. “Bull markets don’t die of old age, but then trees don’t grow to the sky either. The No. 1 problem there is people are trying to time the markets.”

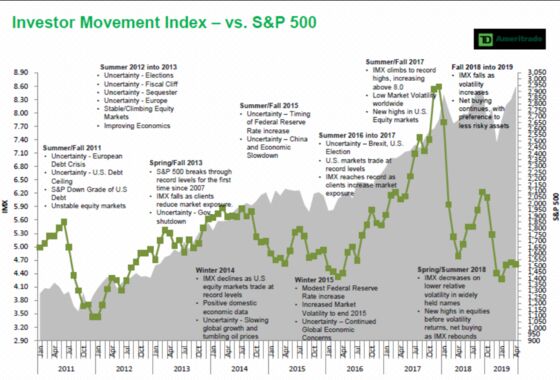

Whatever it is -- the fourth quarter massacre, when 19.9% came out of the S&P 500, or memories of earlier routs -- something has convinced investors to stay away. A measure of TD Ameritrade Holding Corp. clients’ exposure to the market remains near the lowest levels since 2016.

At E*Trade Financial Corp, customers added just 135,000 accounts in the three months ended in March, down roughly 90% from the previous quarter. In Charles Schwab Corp.’s first-quarter earnings release, the company’s chief executive officer acknowledged the toll geopolitical, economic and monetary-policy risks have had on “investor sentiment and activity.”

By some measures, the fast money has acquitted itself no better. In an analysis of 855 hedge funds with more than $2 trillion of total equity positions, Goldman Sachs found that net leverage, a measure of industry risk appetite, now sits below levels seen at the start of the year. While hedge funds were 56% net long at the end of the fourth quarter equity rout, that’s since declined to 52%.

Knowing whether to buy, sell or hold is never easy -- but seldom as hard as in a market whose recent history features one three-month, 5,000-point plunge in the Dow and a three-month rebound in which it clawed it all back. Add to that the impossibility of assessing outcomes in a trade dispute being fought publicly with an air of nationalistic zeal, and it’s easier to understand the reluctance to commit.

“In one world, these China and U.S. trade tensions ease, the global economy does better, the trade tensions clear out the way, risk assets do quite well. The other world is much more dark,” Alex Dryden, a global market strategist at JPMorgan Asset Management, said on Bloomberg Television. “It’s very hard to take any high conviction views one way or another when you have such dependence on these two views and so much uncertainty over which path will be taken.”

That doesn’t make the hazards any less real. A study by Bank of America Corp. on market peaks since 1937 shows that being uninvested in the last year of an advance meant foregoing one-fifth of the rally’s overall return. Sure, hindsight is 20/20, but anyone who believed last September marked the top now knows they were wrong. Missing out on the subsequent gains was painful.

One answer has been to try to limit the pain. What little flows have gone to ETFs have been dominated by a preference for funds that preach security. Low-volatility ETFs took in more than $7 billion in the first quarter, more than any other factor group, data compiled by Bloomberg show. Funds that focus on quality companies with strong free cash flow and are supposed to fare better in downturns also saw hefty inflows, to the tune of $2.7 billion. But it all pales next to fixed-income ETFs, which have added more than $40 billion this year.

“The money is sitting in bonds, the money is not sitting in cash,” Lori Calvasina, head of U.S. equity strategy at RBC Capital Markets, said in an interview at Bloomberg’s New York headquarters earlier this month. An “argument that’s kind of driving me crazy recently is this idea that there’s this wall of money sitting on the sidelines just waiting to come back into equities. We do not see it.”

To contact the reporter on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.