This Stock Research Is Paid For By the Company. Do You Trust It?

This Stock Research Is Paid For By the Company. Do You Trust It?

(Bloomberg) -- Inspired by MiFID II, a practice that’s long been commonplace in credit is rapidly gaining traction in equities -- and that’s making some investors uneasy.

With new European financial regulations shrinking buy-side wallets for research and brokers slashing their coverage list, many companies have found they have to pay to stay on the radar. That’s prompted financial firms from SEB AB to Kepler Cheuvreux to offer sponsored analysis, which the company being analyzed pays for.

While some would say investment banks’ equity research has always been mired in conflicts of interest, sponsored reports make that explicit. But undeniably it is filling a void in the wake of the EU’s Markets in Financial Instruments Directive, which indirectly shrank analyst coverage by making investors pay for research separately.

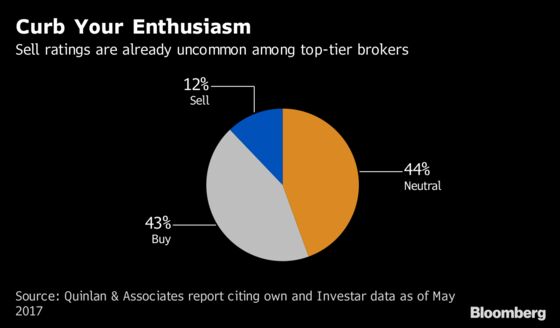

“It’s outsourcing investor relations,” said Benjamin Quinlan, chief executive officer of financial-services consultancy Quinlan & Associates, who harbors concerns over how impartial sponsored research can be. “When you get to the point where the company is paying you money to write a report about them, I just have no idea how you can write anything that puts a knife in the business model.”

Sponsored reports are mostly upfront about the fact that they were paid for by the company in question. Many don’t contain price targets or ratings, though some, such as Kepler Cheuvreux’s, do. An exemption in MiFID II allows sponsored research to be distributed to investors for free, making such reports possibly more widely available than an investment bank’s purportedly independent one may be. The European Securities and Markets Authority didn’t reply to an email seeking comment.

To companies, especially smaller ones, the fear is that as such analysis dwindles, liquidity will decline along with investor interest. Paying for coverage is a way to salvage that.

“By having paid-for research you add to that pool of the conversations going on about your stock,” said David Lloyd-Seed, chair of the Investor Relations Society in London. “I don’t think investors mind whether it’s paid for or they pay for it because what they are after is information about the company to help them make their own decision.” The material is typically intended for institutional investors, he said.

Here’s what firms offering sponsored research are saying:

- Kepler Cheuvreux, a French brokerage, has seen the number of corporates covered by sponsored research grow from 60 at the start of the year to 100 currently, and it plans to double the number within the next two-to-three years, according to Mathieu Labille, deputy global head of research. He says Kepler maintains the same distribution of ratings on companies that commission analysis as on those that don’t.

- French bank Oddo BHF says it has been offering sponsored reports for several years and MiFID II has allowed it to raise prices, according to head of research Matthias Desmarais. It has about 20 clients using the service, and its reports contain ratings. Desmarais says some stocks covered by sponsored research do have sell ratings.

- Edison Investment Research Ltd., one of the largest sponsored research houses, says more larger companies are now turning to it. Revenue growth after MiFID has been the strongest in recent memory, according to CEO Fraser Thorne. Edison charges companies about 50,000 pounds a year for such services.

- Hardman & Co.’s CEO Keith Hiscock says revenue from its sponsored segment has grown 50 percent in the first half from the previous year. It charges up to 45,000 pounds annually.

- AlphaValue, a French independent research provider, is offering sponsored research to 10 small-cap clients for about 20,000 euros ($23,530) a year, head of marketing Maxime Mathon says.

- In Scandinavia, SEB AB, Nordea Bank AB and DNB Markets have all revealed plans for sponsored research. SEB has signed up about 10 corporate clients for the business since launching it in April, according to Nicklas Fharm, who runs the unit. The market rate is about 50,000 to 60,000 euros a year for each stock, he added, while declining to comment specifically on SEB’s prices. SEB doesn’t do ratings or price targets on the research.

These firms say their business model doesn’t mean the analysis is necessarily biased, since their credibility is on the line, and at least they’re transparent about it. Hardman and Edison, which only conduct sponsored research, say they allow their clients to review the report mostly to ensure factual accuracy before publication -- but not alter the analysis. The clients can then demand that the report be canned, which does not affect their payments to the research houses, though both say this is very rare.

“We’re not a broker, so we’re not making recommendations, which gives us an ability to be much more long-term,” Edison’s Thorne says. “Actually, we have far fewer conflicts in our business model than brokers do.”

In a way, equity analysis has never been entirely independent. Investment banks and brokerages have an incentive to be on good terms with companies in order to manage their deals or share sales or to arrange investor meetings with corporate management.

For Shore Capital Group Ltd., a U.K. firm that doesn’t offer sponsored research but does act as house broker, corporate retainers for brokerage services have grown this year on the understanding that companies now need to pay more to maintain coverage, according to Chairman Howard Shore.

To some investors, sponsored research is decidedly more conflicted than the existing sell-side model.

“The conflict of interest in that specific configuration will be unavoidable,” Luc Mouzon, head of European equity research at Amundi SA, Europe’s largest asset manager, said in an email. He added that his team would be reluctant to use such services and is leaning toward using more independent providers.

Others concur:

“The trouble this causes is it’s not seen as independent,” said Graham Clapp, a fund manager at RWC Partners Ltd. in London, who has been managing European equities since 1991. “Companies will have to get better at talking to investors directly. I think ultimately the longer-term implication of MiFID is going to be a disintermediation impact.”

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Paul Jarvis, Celeste Perri

©2018 Bloomberg L.P.