This Is No February VIX Redux: ETPs Aren't Their Old Selves

This Is No February VIX Redux: ETPs Are Shadows of Former Selves

(Bloomberg) -- Stock traders are reciting the most ominous mantra in finance -- this time it’s different.

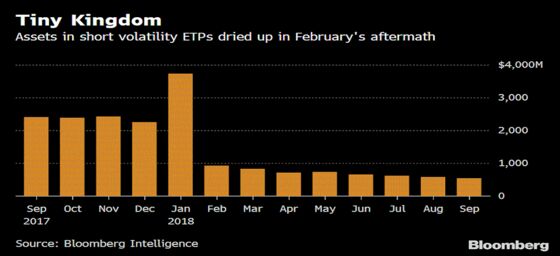

As equity volatility surges, one key ingredient that dished up February’s vol-pocalypse is missing: Exchange-traded products that fuelled the record rout are a shell of their former selves.

Short-volatility products held just $527 million at the end of last week versus $3.43 billion preceding the VIX spike on Feb. 5. And investors may have been prescient in donning protection ahead of this week’s storm, with $2.5 billion held in equivalent passive instruments with long-volatility bets.

That’s a big deal.

Earlier in the year, volatility-related ETPs scrambling to rebalance their holdings snapped up VIX futures in the grip of the meltdown, effectively pushing up the price of the contracts -- and eventually the underlying index, the now-famous theory goes.

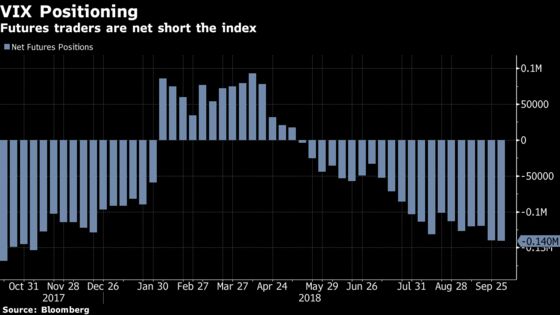

“The main difference between now and Jan/Feb is the VIX ETP space which is a fraction of its former size and positioned net long,” Patrick Hennessy of IPS Strategic Capital, an investment-management firm, tweeted.

The so-called fear gauge surged to 23.82 on Thursday compared with a sub-15 reading last Friday.

In February, products betting on low equity-price swings such as the now-deceased XIV were widely blamed for exacerbating one of the most violent moves in U.S. equities in history, having swelled to a large enough size to potentially move the underlying futures market.

That’s not to say that all traders were showing a long bias in the lead-up to Wednesday’s equity meltdown. Speculators were net short VIX futures as of Oct. 2, CFTC data show.

“The short VIX product “suite” of XIV and SVXY that contributed to February’s spike in VIX (and perhaps equity selloff) is now largely irrelevant, with only a tiny fraction of its old risk, and can be safely ignored,” Pravit Chintawongvanich, equity derivatives strategist at Wells Fargo Securities, wrote in a note.

--With assistance from Luke Kawa.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Cecile Gutscher

©2018 Bloomberg L.P.