These Are the Charts That Scare Wall Street

These Are the Charts That Scare Wall Street

(Bloomberg) -- Halloween’s around the corner, with investors treated to fresh all-time highs in U.S. stocks and nary a trick in sight. But as any scary movie aficionado will tell you, the most formidable frights begin when you’re the most complacent.

This year’s compilation of Wall Street’s chilling charts highlights concern about a debt-laden Corporate America, eerie developments in volatility markets and the ills in industrial sectors of the economy. Here are the ghoulies that petrify the professionals.

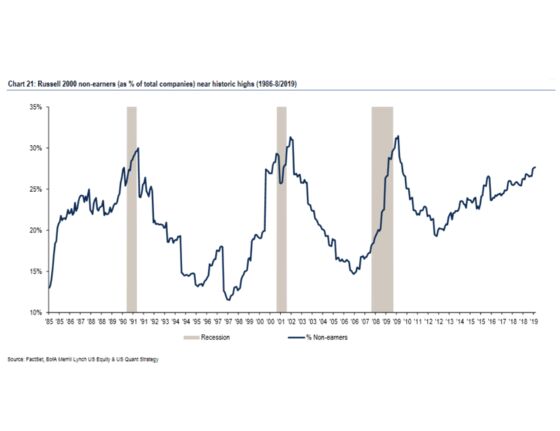

Jill Carey Hall, head of U.S. SMID-cap strategy at Bank of America Merrill Lynch:

Quality has grown increasingly scarce within small caps: the proportion of non-earners within the Russell 2000 has climbed to nearly 30% -- a level typically only seen during recessions. (One key industry driver: the Biotech IPO boom, where the addition of newer/early-stage Biotech companies has increasingly driven up the proportion of non-earners. The lack of profitability for many Energy companies has been another big driver). High quality companies tend to outperform in the current phase of the cycle -- when the U.S. is in a soft patch or downturn -- and in periods of elevated volatility.

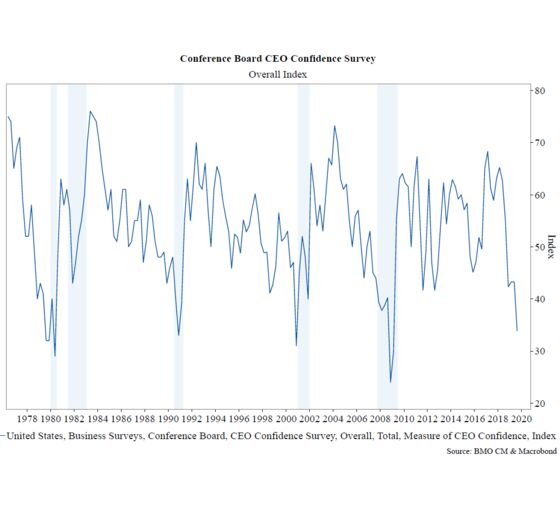

Jon Hill, vice president of U.S. rates strategy at BMO Capital Markets:

Going back to the 1970s, CEO confidence hasn’t been this low without the U.S. either about to enter, or already in a recession. If corporate leadership pulls back on investment and/or hiring, that alone could be enough to trip us into contraction. More worrisome is that borrowing costs being too high are notably absent from the cited headwinds -- “Tariffs and trade issues, coupled with expectations of moderating global growth” -- as a result, the impact of incrementally reducing interest rates may be insufficient to stem the cynical tide.

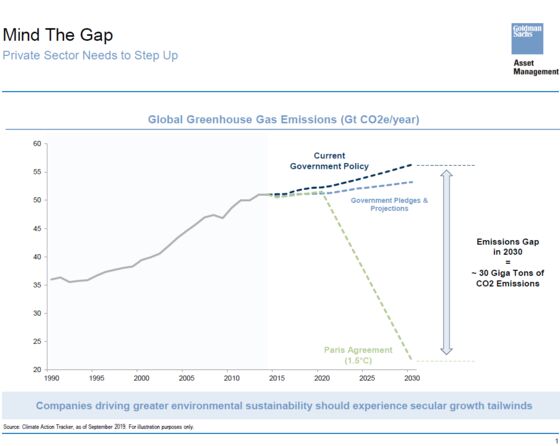

Kathryn Koch, co-head of Goldman Sachs Asset Management’s fundamental equity business:

According to Climate Action Tracker, current government commitments and projections for carbon reduction fall 30 gigatons short of reaching the Paris agreement targets. In order to potentially reach these targets, we believe the corporate sector will need to provide innovative solutions to the challenges the planet faces today. Those corporates that can provide innovation solutions should benefit from secular growth as the focus on environmental sustainability continues to increase.

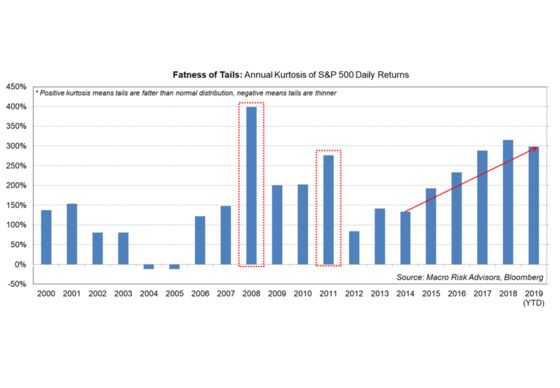

Maxwell Grinacoff, derivatives and quantitative strategist at Macro Risk Advisors:

FRAGILE: Handle with Care – Looking at just top-line realized volatility gives a simplified picture of actual market fragility. In statistics, the frequency of unusual moves is measured via kurtosis. In the below chart, we calculate the 1Y kurtosis of S&P 500 daily returns, attempting to measure the frequency of tail moves and quantify the ‘fragility’ of the index by year over the past two decades.

We note that S&P 500 fragility has been steadily increasing over the past 5Y and is on pace to meet/possibly surpass last year’s metrics (think drawdowns like February and October-December 2018). Even in the doldrums of 2017, a 40 basis point move dictated a one standard deviation move in the index (based on an average 20-day realized volatility of sub-7%). That said, a 50-100 basis point move in the S&P was considered outsized at the time! Worth noting that 2017 witnessed >0.50% daily returns ~20% of the year.

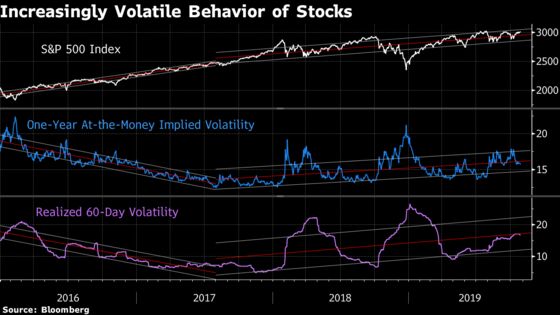

Patrick Hennessy, head trader at IPS Strategic Capital:

Taking a look at the bigger picture the trend higher in the S&P 500 remains intact. The primary difference between 2016/2017 and the last two years is the change in trend in realized and implied volatility. All three have trended higher since August of 2017 due to the increasingly volatile behavior of the S&P 500. Historically, it’s more likely to see this dynamic near markets tops than market bottoms.

Megan Miller, portfolio manager at Analytic Investors:

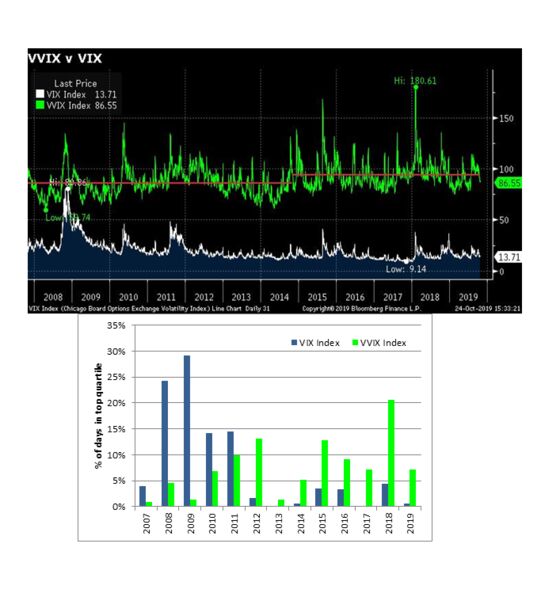

The market’s “Fear of Fear” is increasing and appears to be in a new regime. CBOE’s VVIX Index provides the industry with a useful measure of volatility of volatility or “fear of fear.” The value represents the implied volatility of near-term VIX options. 2018’s “Volpocalypse” was peak “vol of vol” with the VVIX closing at 180%. What jumps out at me, though, is that the VVIX reached the top quartile in the last five years, with the largest frequency in 2018. However, the top quartile of the original fear gauge, the VIX Index, occurred mostly during the global financial crisis. If you compare the VVIX with VIX, you see almost a mirror image of extremes. The average “vol of vol” of the last five years is higher, yielding a higher VVIX regime than in earlier years. The opposite is true for VIX.

We hypothesize increased volatility of volatility indicates market fragility. If that’s the case, then are we in a latent volatility regime on the verge of cracking?

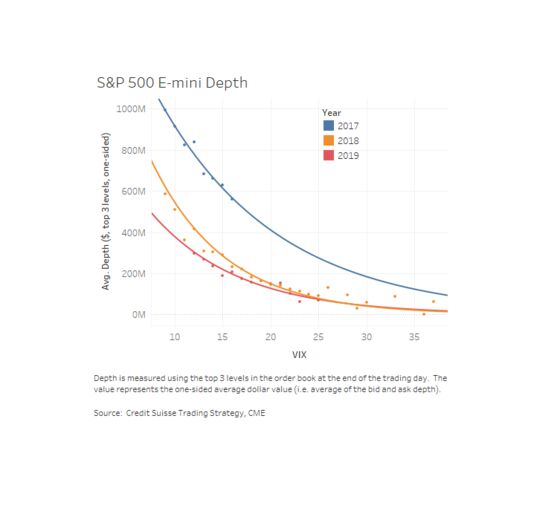

Victor Lin, equity trading strategy at Credit Suisse:

Despite the S&P 500 being back near record highs, market depth remains extremely shallow. If that wasn’t concerning enough, depth is significantly lower than previous years at similar levels of the VIX, reflecting increased sensitivity to risk. This usually makes it more difficult to trade in size and also potentially leaves the market more susceptible to extreme moves.

Ben Emons, managing director of macro strategy at Medley Global Advisors:

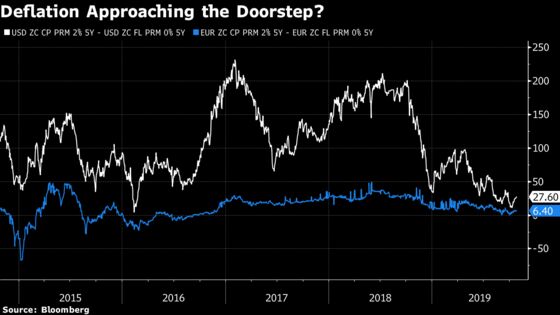

Mario Draghi’s farewell bid has left the Eurozone near deflation risks. Despite three rounds of quantitative easing, markets price in Europe will have inflation below 1% for the next decade. The U.S. fortunately has higher inflation and the Fed remains confident the inflation target will be met. That said, inflation swap markets see this differently.

The premium of the inflation “cap” struck at 2% is just 26 basis points higher than the inflation “floor” struck at 0%. This says, inflation markets see little scope for the U.S. to reach the target, with possible downside risks of deflation. More worrisome is the difference between U.S. inflation caps and floors has moved closer to Europe, which sees only 6 basis points difference between caps and floors. This signals inflation markets expect neither the Fed nor the ECB will be able to fend off the risk of deflation sometime in the next decade.

Subadra Rajappa, head of U.S. rates strategy at Societe Generale:

Both market-based and survey-based measures of inflation are at or near the lowest level in two decades. Secular trends like globalization and technological efficiencies, the so-called “Amazon effect”, continue to keep a lid inflation. Rate cuts thus far have had little impact on inflation expectations. Conventional monetary policy seem inadequate to address this issue. What can the Fed do to reverse the trend? Lower for longer, inflation averaging, price-level targeting are ideas, will any work?

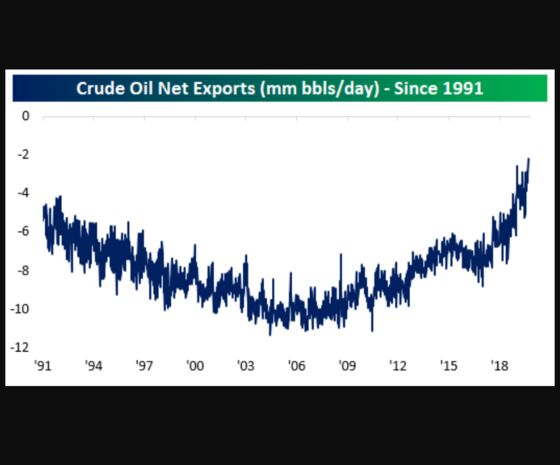

George Pearkes, macro strategist at Bespoke Investment Group:

In the most recent weekly data reported by the EIA, the U.S. imported only about 2.2 million barrels of crude per day, net of exports. The rise of shale has meant that fewer U.S. dollars are flowing abroad in exchange for crude. Add on what might happen as electric vehicle deployment ramps up, and the prospects for a net crude trade surplus in the near future mean one major source of dollar liquidity for resource-heavy global markets is drying up.

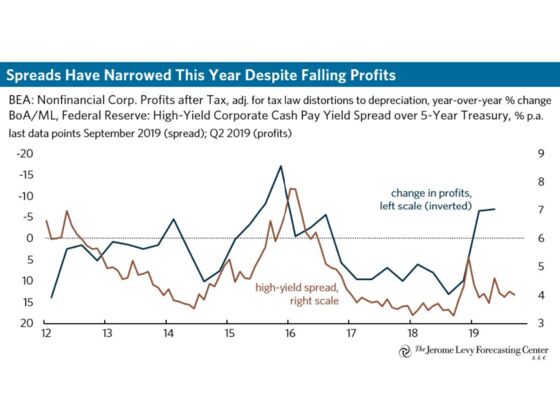

Robert C. King, senior economist at The Jerome Levy Forecasting Center:

One cause for worry is falling earnings, which will make already elevated leverage ratios look much worse. The third-quarter earnings season may be an important reality check for investors who have been told all year that a rebound in earnings is just around the corner.

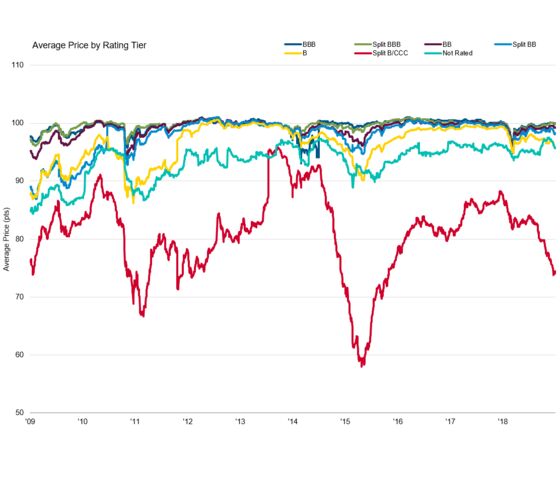

Erin Browne, portfolio manager at Pimco:

The deterioration in the corporate credit quality year-to-date highlights a vulnerability in markets and is a reason why PIMCO remains defensive on broader corporate credit. Leveraged loans, for example, are one corner of the market showing cracks, with corporate income growth now expected to be negative, marking the first time since 2016, while debt levels are high, particularly among weaker credits. Lower-rated high-yield bonds are showing similar pressures.

While historically, leveraged loans have offered recovery rates considerably higher than high yield bonds in default, investor protections for loans are much weaker today than they were at the peak of the last credit cycle in 2007 and loan-only issuance without high yield bond cushion has exploded. For this reason, we expect loan recoveries to be lower than historical averages, but still higher than high yield during the next cycle. In addition, ratings downgrades, slack in demand, continued deterioration amongst the weakest credits, and a preference from buyers for higher quality issues, all make loans, especially the weaker, loan only issues, one of the most vulnerable segments of corporate credit into a late cycle macro environment. I am watching whether the weakness in the distressed B/CCC credits starts impacting higher rated credit issues or adjacent credit markets.

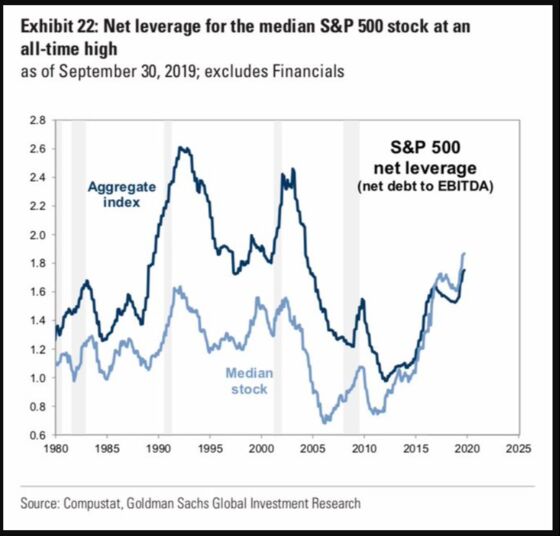

David Schawel, chief investment officer at Family Management Corporation:

Net leverage for the median stock is at an all time high. If earnings growth continues to slow, we could see even more pressure on corporate balance sheets which have been stretched of late.

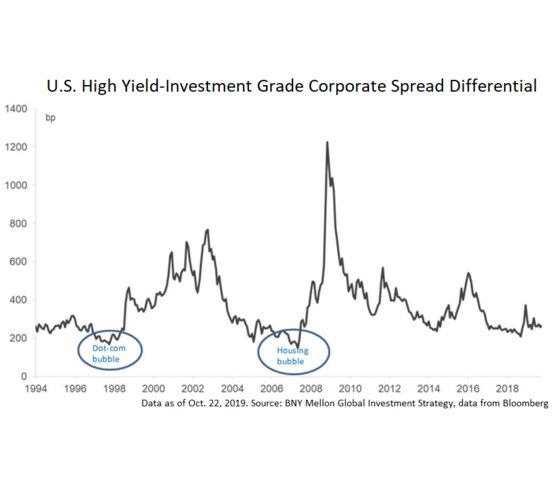

Alicia Levine, chief strategist at BNY Mellon Investment Management:

U.S. high yield spread differential to investment grade is near the tightest level ever, suggesting heightened market complacency that resembles historical pre-crisis bubbles.

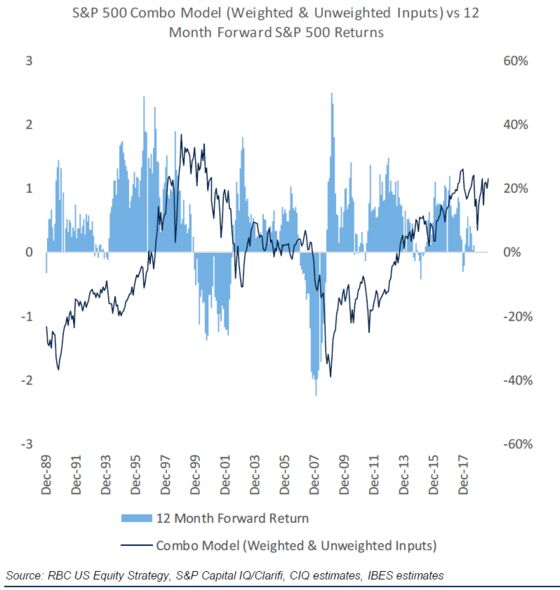

Lori Calvasina, head of U.S. equity strategy at RBC Capital Markets:

One chart that we consider to be a clear negative or overhang for the stock market at the moment is our valuation model. This model was 1.1 standard deviations above its long-term average as of mid-October, well above average and close to the peaks of the current cycle. Each cycle tends to have a different ceiling. The ceiling of the current cycle is a bit above the pre-financial Crisis ceiling, and a bit below the tech bubble ceiling. This model is essentially bumping up against the highs of April/June 2019, August/September 2018, and 4Q17/Jan 2018. It’s also a range historically associated with 12 month forward returns in the S&P 500 in the low single digits.

The blue line on the chart summarizes a number of different valuation metrics, both market cap weighted multiples (more representative of the broader market) and median multiples (more representative of the opportunity set of portfolio managers and sell-side analysts). It’s comprised of things like P/E, but also includes things like price to sales, price to book, price to operating cash flow, and EV to EBITDA, so it gives you a sense of how stocks and the broader market look across a variety of valuation multiples.

It’s telling us the U.S. equity market is very overvalued right now, and at a level that it’s simply not been able to break through.

Conor Sen, portfolio manager at New River Investments

With factor investing being all the rage, people should be wary about what their factor ETF’s hold. Someone owning the iShares momentum factor ETF, MTUM, might think they’re getting exposure to hot growth stocks. But the #1 holding of MTUM right now is Procter & Gamble, which trades at a historically high valuation on an enterprise value to sales basis. In momentum investing, all that matters is price movement. Defensive stocks like Procter & Gamble have attracted interest as investors look for stability in this tumultuous macro environment and with interest rates being so low. Crowding into defensive stocks might not turn out so well for momentum investors if either the global growth environment improves, causing interest rates to rise, or if those defensive stocks end up reporting disappointing earnings.

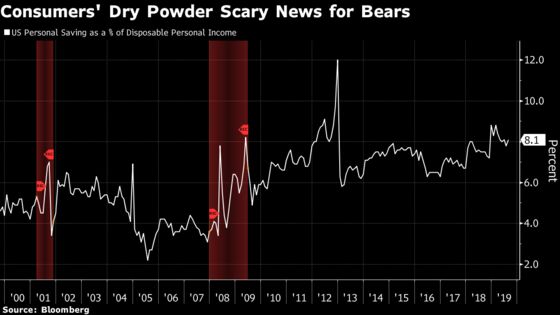

Neil Dutta, head of U.S. economic research at Renaissance Macro Research:

The most worrisome chart is the personal saving rate. But not for the growth bulls, for the bears. The saving rate is elevated as it is despite pretty healthy consumption growth in recent quarters. Assuming the negative news flow clears up and consumers draw down their precautionary savings, consumption will surge and the bearish economic prognosticators will have to move onto something else.

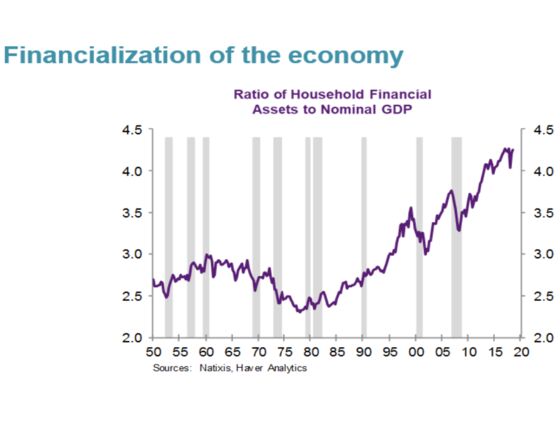

Joseph LaVorgna, chief economist for the Americas at Natixis:

The financial market (stocks and bonds) is at a near record-size relative to the broader economy. The tail now wags the dog, as the Powell Put is alive and well.

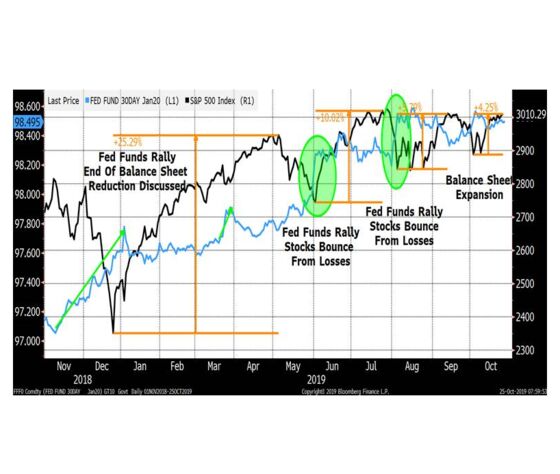

Peter Tchir, head of macro strategy at Academy Securities:

Yes, lots of other things have influenced markets, but it is impossible to argue that in 2019 -- at least four times, between balance sheet adjustments and talk of easing -- the Fed didn’t play a major role not only in propping the market up, but specifically stepping in at almost any sign of weakness. How long can that go on?

I expect a neutral position from the Fed this week and that doves will be thoroughly disappointed. Since each dovish action from the Fed seems to have less impact on markets, that is real cause for concern, or, in the spirit of Halloween, it is scary.

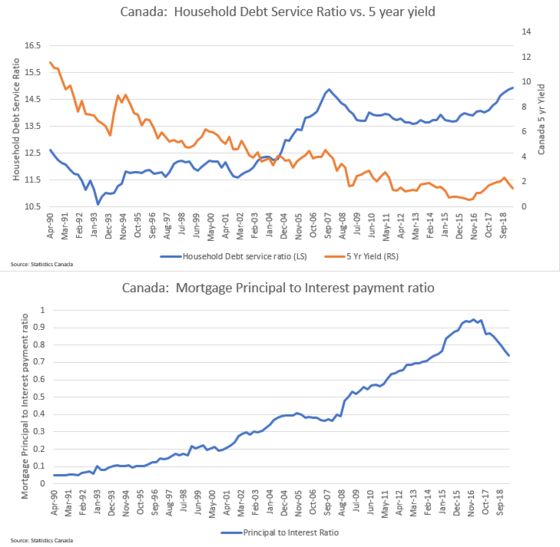

James Price, director of capital markets products at Richardson GMP:

Canadian households’ debt-service ratio hits all-time highs despite very low borrowing rates. In particular, the last three quarters of measurement have continued higher despite rates dropping since the beginning of Q4/2018.

This chart suggests that, given low interest rates (sub 2% for most of the last 5 years) that debt service costs have strongly accelerated recently, with the bottom panel showing the portion of that payment going to pay down principal has started to decline…quickly. Historically, the Principal/Interest ratio has a strong negative correlation to yields (-0.90 over 30 years), but that correlation has turned positive over the past two years.

This shows exhaustion in Canadians’ ability to take on more debt despite the past year of declining rates.The concern is that small changes in employment rates could have an outsized impact in the ability to make mortgage payments, and lower yields might not help. Since we Canadians do not like to default on our mortgages, pressure on investment properties and other spending first is highly likely.

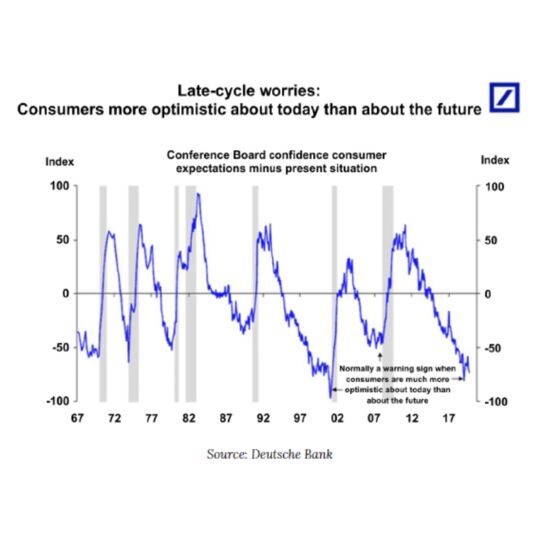

Jay Pelosky, chief investment officer and co-founder of TPW Investment Management:

Given the manufacturing slowdown, as evidenced by the ISM under 50, the U.S. economy is very dependent on continued consumer health and spending. The chart below shows real consumer concern about the future vs the current pretty good star of affairs (record low unemployment, decent wage gains, etc). Should those concerns lead to a pullback in 2020 consumer spending the U.S. economy could weaken further regardless of whether the Fed continues to cut rates or not. This would challenge the forecasted 2020 S&P 10% EPS growth and thus the potential for higher U.S. stock prices.

Benn Eifert, chief investment officer at QVR Advisors:

This is probably boring and repetitive, but I find the below chart scarier than any charts I see from volatility land.

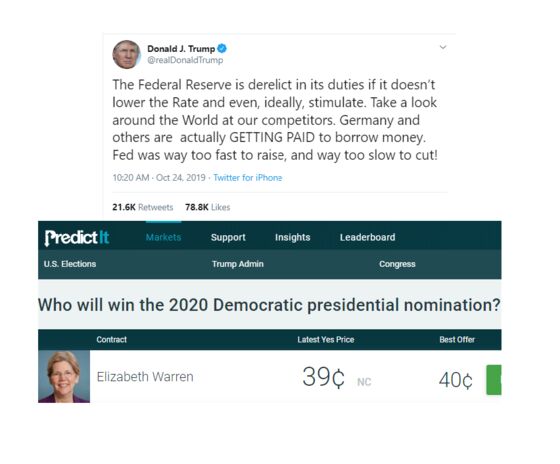

Gina Martin Adams, chief equity strategist Bloomberg Intelligence:

I’d just put up a picture of Trump’s twitter account, especially something where he is bashing the Fed, or tweeting out a tariff, or a picture of Elizabeth Warren campaigning. It seems the distractions of Washington are Wall Street’s greatest fears this year.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Dave Liedtka, Rita Nazareth

©2019 Bloomberg L.P.