Best-in-a-Decade Canada Bond Rally Leaves Some Pockets of Yield

Best-in-a-Decade Canada Bond Rally Leaves Some Pockets of Yield

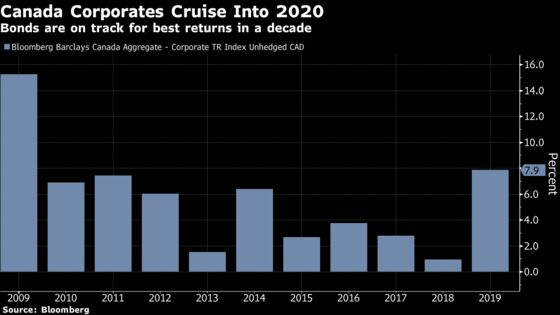

(Bloomberg) -- The best performance in a decade for Canadian corporate bonds may be hard to beat in 2020, but there’s still yield to be found in parts of the market, according to some of the country’s biggest money managers.

Corporate debt has returned 7.9% his year, according to Bloomberg Barclays Canada indexes. Hybrid bonds, including debt that can be converted into equity, and the first rung of the investment-grade ladder may present investors with the best risk-return opportunities next year, with energy companies favored in the category.

“These companies are a natural monopoly with take or pay contracts and utility-like cash flow profile,” said Nicholas Leach, a portfolio manager at CIBC Asset Management, the C$134 billion ($101 billion) investing arm of Canadian Imperial Bank of Commerce.

Faced with rate cuts from some central banks, global investors have snapped up more than $2.4 trillion of new issues across all currencies this year. That’s pushed up valuations that are unlikely to be sustained as an improving global economy puts further monetary easing on the back burner.

Hanif Mamdani, head of alternative investments at Royal Bank of Canada’s RBC Global Asset Management, which has $345 billion under management, is also betting on hybrid bonds, including pipeline company Enbridge Inc. and natural gas firm Keyera Corp., he said from Vancouver.

As the debt is subordinated, ratings firms take a conservative approach and assign a non-investment grade rating. That prohibits some institutional investors from investing in the notes, despite the companies’ stable revenue and cash flow, according to CIBC’s Leach.

“High-yield investors that don’t face those restrictions can take advantage of that,” he said. “Although the bonds are subordinated claims, they rank senior to equity, which represents an enormous value cushion for even the subordinated bondholders.”

Recession Risk

Elsewhere, debt rated just above junk looks cheap. Bonds rated BBB, the lowest investment-grade rating, are yielding about 3.18%, compared with 3.51% for bonds with a BB rating, the highest tier of junk. That leaves just a 0.33 percentage-point spread between the two, versus 1.74 points last December.

For Mamdani, a recession later in 2020 is the biggest risk for credit assets.“We are protecting ourselves as much as we can by moving up in quality and shortening durations to reduce the spread-widening impact,” he said.

That’s a strategy that Sue McNamara at Beutel Goodman & Co., which oversees C$42 billion of assets is also taking. The firm expects a “credit spread-widening event” in 2020 related to a pullback in the stock market, an economic slowdown, a reset on earnings expectations or a credit-specific event that causes a reassessment of risk, McNamara said in an interview.

Despite the temptation of going into riskier corners to get extra yield, it will pay to hold Canada government bonds due in 10 or 30 years as a hedge against declines in both stocks and bonds, according to Alexandra Gorewicz, portfolio manager at CI Investments. Canadian government bonds have returned 13% this year, the most since 2014, according to the Bloomberg Barclays Long Total Return Index.

“We’re not excited about any asset class for 2020, because everything has performed so well this year,” she said.

To contact the reporter on this story: Paula Sambo in Toronto at psambo@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, ;David Scanlan at dscanlan@bloomberg.net, Jacqueline Thorpe

©2019 Bloomberg L.P.