(Bloomberg Opinion) -- When it comes to private equity, governments nationwide and their retirees may not actually be getting what they pay for. That at least is the conclusion of a new study that questions whether pension fund managers’ recent infatuation with private equity is wise.

The study, by three professors from Brigham Young University and one from Ohio State University, found that the big returns investors think they are getting from private equity funds are really just the result of leverage and the bull market. Exclude that stuff, the authors say, and the excess returns provided by private equity funds — commonly called alpha in the investment management business — is “not significantly different from zero.” The same or better return can be achieved just by levering up a typical S&P 500 Index fund. The study found this is essentially true for both buyout and venture capital funds, though it is slightly less true for the VCs.

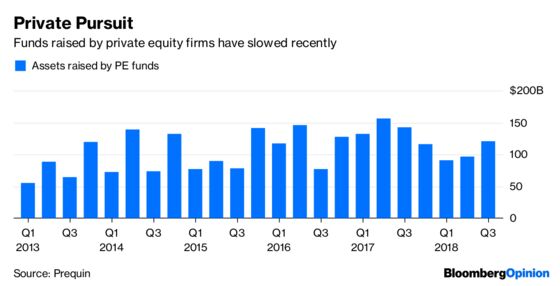

If the study, which was posted last week on the National Bureau of Economic Research’s website, is correct, it’s clear that many people who play a big role in determining whether there will be enough money to pay what has been promised to public workers in retirement — and the burden that will be on the rest of us if there isn’t — have not thought deeply enough about private equity returns and where they come from. More and more pension funds have recently been plowing more and more money into private equity funds. New York City recently reported that its five pension funds paid Wall Street $1 billion in management fees last year, the first time those fees reached 10 figures. A big reason was an increase in allocation to higher-fee private equity funds.

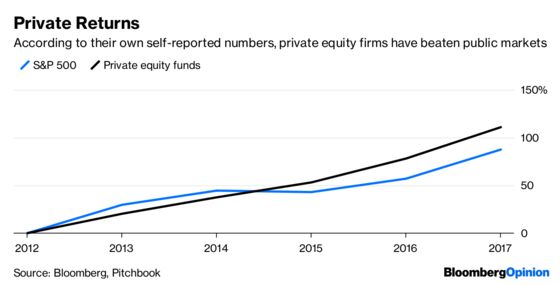

The returns provide little justification for that. New York City said in its report that its private equity portfolio since inception in the late 1990s had returned about 3 percentage points less a year — 10.3 percent compared with 13.1 percent — than if that money had been invested in public markets. Private equity firms, which often show returns that exceed public markets, say this is not the point. Like so many other types of investors, they say their returns are better because they are “lower risk” and “uncorrelated” to the market. Those magic words apparently always get you far on Wall Street.

The study suggests that logic is flawed as well. To prove that, the authors came up with a novel way to calculate private equity returns. Most existing private equity indexes are based on the net asset values that private equity firms self-report, which tend to reflect the market as well as where those managers value the investments, which is likely to be higher than the market — the reason they made the investment in the first place. To get around this, the authors created their own index of returns based on how stakes of private equity investments traded on the secondary market. What the authors found is that the market’s view of the value of those portfolios, as measured by the price at which the stakes were being bought and sold, swung much more widely, and much more in lockstep with the S&P 500 and other public market indexes, than those self-reported NAVs suggested. That suggested that much more of those private equity returns were market-related. Add in leverage, and there is remarkably little return left to attribute to skill — in fact almost none, in the authors’ calculations.

Pension fund investors do seem to be realizing that investing in private equity funds is not as good as it looks. Inflows into PE funds have slowed a bit. But they are coming to this conclusion for the wrong reason. Many pension funds seem to think high fees are the problem. Recently, several of them have begun investing in private companies directly, or doing their own buyouts. Some states like California are forcing private equity firms to better disclose their fees. But the point of the study is not that the fees are too high, but that trying to beat the market with lower risk is impossible.

Private equity executives have done a good job convincing many investors that they have a secret recipe for supercharged returns. And with interest rates at historic lows, it’s no surprise that pension fund managers have turned to alternative investments to meet their projections. The problem is it’s difficult to back up the private equity sales pitch.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2018 Bloomberg L.P.