There’s a Wall of Cash Eager to Buy Treasuries on Any Price Dip

Investors overseeing trillions of dollars are plowing money into U.S. government debt like never before.

(Bloomberg) -- Investors overseeing trillions of dollars are plowing money into U.S. government debt like never before, in a wave that’s only gaining strength as the spreading coronavirus casts doubt on the global growth outlook.

Evidence of the insatiable demand can be found across the fixed-income universe. Pensions, which have been ramping up bond allocations for more than a decade after a change in regulations, now hold a record amount of longer-dated Treasuries. Bond mutual funds saw a historic inflow of money last year, with no sign of a slowdown. Even hedge funds have piled in.

The wall of cash is a boon to American taxpayers as the federal deficit swells. It’s keeping Treasury yields, a benchmark for global borrowing, near all-time lows. With buyers ready to pounce, even surging stocks, record auction sizes and the tightest labor market since the 1960s can barely make a dent in bond prices.

“Treasuries are a resilience play that makes sense,” said Scott Thiel, chief fixed-income strategist at BlackRock Inc. “And so far, people have been rewarded for coming in and buying when yields get to the high end of the range.”

Just weeks ago, global economic reflation and the seeming inevitability of higher yields were the buzz among strategists and investors. The virus’s onslaught is unraveling that narrative, which already faced skepticism from those who argue that persistently low inflation and shifting demographics will pull yields lower.

“I expect the Treasury 10-year yield to fall to zero, perhaps within two years,” said Akira Takei, a global fixed-income fund manager at Asset Management One Co., which oversees more than $450 billion. “I’ve been overweight U.S. Treasuries. That’s based on my view that developed economies are facing a combination of aging demographics and falling birth rates, slow growth and low inflation.”

Investors snapping up Treasuries as an insurance policy have turned the U.S. yield curve on its head. With inflation still subdued and concern mounting that the spreading illness will damage an already fragile global economy, traders have boosted bets on Federal Reserve rate cuts in 2020. That prospect is in turn supporting equities.

The appetite for debt has extended to sovereign obligations of all flavors. One example: Greek 10-year rates once near 45% slid below 1% this month. The country’s junk rating is proving little deterrent with the world’s pile of negative-yield debt climbing above $13 trillion amid the latest global bond rally.

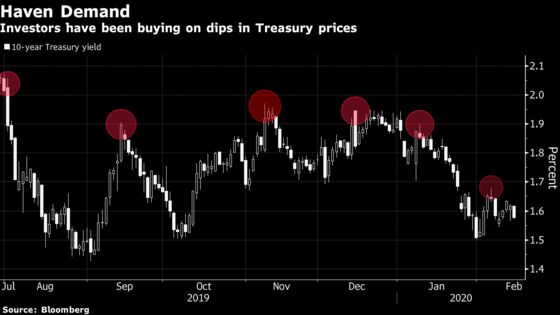

Benchmark 10-year U.S. yields have dropped to around 1.6%, from a 2020 peak of 1.94% in the first week of the year. The world’s biggest bond market has earned about 2.2% this year, after a 6.9% return in 2019 -- the best performance since 2011.

| Read More |

|---|

|

“You still need a duration ballast and shock absorber,” said Con Michalakis, chief investment officer of retirement fund Statewide Superannuation Pty., which manages about $7 billion in Adelaide, Australia. “And I don’t see yields moving materially higher from here.”

The likely economic hit from the virus reinforces that view. Fed Chairman Jerome Powell last week cited the outbreak as a risk. Goldman Sachs Group Inc. predicts it will subtract two percentage points from annualized global growth this quarter.

“If the Fed is staying super-accommodative -- basically in reflation mode -- then you want to buy equities, credit and, strangely, you also want to buy Treasuries,” said Ralph Axel, an analyst at Bank of America Corp.

The demand for Treasuries in some corners has been building for years. U.S. corporate pensions, for example, have been big buyers since the federal Pension Protection Act, passed in 2006.

For the top 100 funds, with combined assets of more than $1.4 trillion, the fixed-income allocation surged to about 49% at the end of 2018 from 29% in 2005, as equities’ share fell by half to 31%, according to Milliman Inc., a pension and risk advisory firm. JPMorgan Chase & Co. strategists estimate the debt portion topped 50% as of December.

An up-to-date read on retirement funds’ demand can be seen in the record surge in Strips, which are created when Treasuries are split into principal- and interest-only securities. Pensions tend to favor these assets, which have longer duration, or sensitivity to interest-rate changes, to match the length of their liabilities.

Soaring stocks are also spurring buying of bonds on price declines.

U.S. public pensions, with total assets of over $4 trillion, have kept holdings steady over the past five years, at about 25% in fixed income, 50% in public equities and the rest in alternative investments, according to data from the Pew Charitable Trusts.

As equities have climbed, the funds have needed to buy more debt to keep the breakdown stable, said Greg Mennis, director of public sector retirement systems at Pew.

Veteran bond manager Dan Fuss says he’s been been buying Treasuries as a safety play. He points to last week’s 10-year auction as a sign that yields won’t bust higher anytime soon. A measure of demand for the $27 billion sale was the highest since March.

“When you look at the bids for the 10-year notes, you’d have thought, ‘Wow, the government was giving out free ice cream’,” said Fuss, vice chairman of Loomis Sayles & Co. “There’s just more money available to invest than there’s marketable investment opportunities, and no risk of inflation at this time.”

--With assistance from Masaki Kondo and Matthew Burgess.

To contact the reporters on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net;Ruth Carson in Singapore at rliew6@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, ;Tan Hwee Ann at hatan@bloomberg.net, Mark Tannenbaum, Jenny Paris

©2020 Bloomberg L.P.