The Year Stock Traders Became an Endangered Wall Street Species

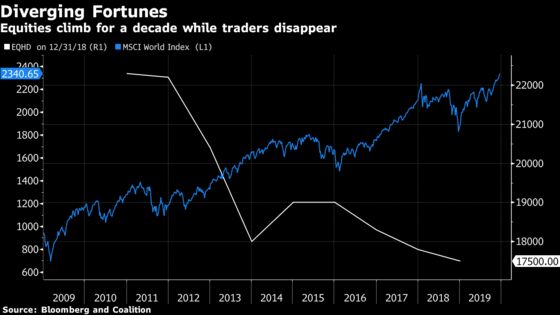

Somehow, the longest bull market in stocks has completely bypassed banks’ equities traders.

(Bloomberg) -- Somehow, the longest bull market in stocks has completely bypassed banks’ equities traders.

Buying and selling shares for clients such as hedge funds, mutual funds and other investors used to be a key business for investment banks. They built up large trading desks during the stock market booms in the 1990s and early 2000s, luring traders with six-figure paychecks and generous bonuses.

But for a decade now, the number of stock traders has steadily declined, even as markets all over the world rallied again to records. The past year was particularly disastrous as several big banks took the axe to their trading units, especially in Europe.

Deutsche Bank AG’s announcement that it will exit equities trading is the biggest single case in point, but HSBC Holdings Plc, UBS Group AG, Macquarie Group Ltd. and Citigroup Inc. also plan deep cuts or have already made them, people familiar with the matter have said. Industrywide, the number of stock traders employed at banks is now the lowest since well before the financial crisis.

There are plenty of reasons for the long decline. The rise of passive investing means less active stock trading through banks and brokers. Electronic trading has squeezed margins and market makers such as Citadel Securities or Virtu Financial Inc. have taken large chunks of business from investment banks. At the same time, new regulations, particularly in Europe, have made trading more costly for lenders.

“It has been a horror year for equities traders at banks,” said Klaus Schinkel, a former executive in Macquarie’s equity capital markets business who now heads the German operations for Edison Group, an investment research firm. “You will see more retrenchment from the small and medium sized banks that try to do it all.”

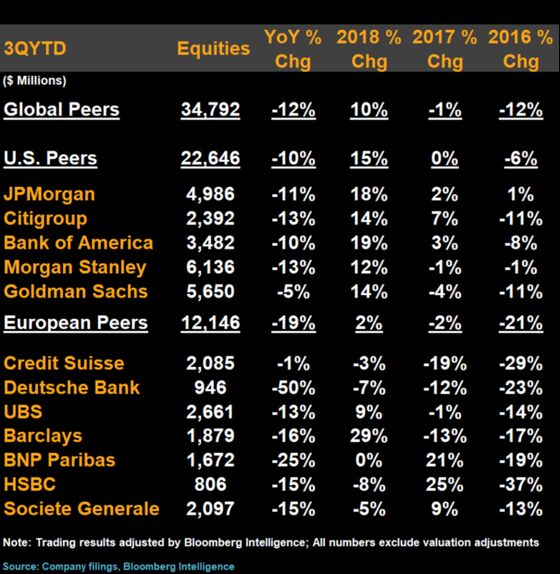

The pain is most severe in Europe, where fragmented financial markets and half a decade of negative interest rates have already pushed many lenders to the brink. For at least four years now, European investment banks have been losing market share to their U.S. rivals, data compiled by Bloomberg Intelligence shows. The year 2019 is no exception, with revenue falling at about twice the rate at the U.S. lenders.

The job losses in equities trading are part of a wider malaise in European banking, with lenders in the region announcing plans to slash their workforces by a combined 63,000 this year. HSBC will provide details on the restructuring of its trading operations in February. It’s not clear yet how many of Societe Generale’s planned 1,600 cuts will hit equities. UBS, meanwhile, is shifting resources away from its investment bank, people familiar with the matter have said.

The trading of plain vanilla stocks -- what the banks call cash equities -- has been particularly hard hit because it’s simple and computers can more easily replace humans. Cash equities traders are on track for some of the harshest bonus cuts, according to predictions from recruiting firm Options Group. The pot could shrink by 15% in Europe.

Regulatory changes have added to the headwinds, especially a European set of rules known as Mifid II. In effect for almost two years, it has multiplied the amount of paperwork banks have to go through before they can complete a deal, making each trade more costly and time consuming. The rule has also forced banks to charge separately for the equities research they provide to clients, prompting smaller banks such as Berenberg, Maquarie and Oddo-BHF to cut staff at the units.

Even some regulators including Germany’s watchdog Bafin now concede that the unintended side effects of those regulations must be reined in. A review is underway though it’s neither likely to conclude anytime soon nor do many people expect it will yield substantial relief.

Still, for Jay Bennett, head of equities at Greenwich Associates, it’s not all gloom.

“I’m not as pessimistic as to say there will be a last man standing but it will be a smaller number, ” he said. “Our sense is most of the cuts are over. The question is what ticks up the equities market in terms of healthy volumes and those are known unknowns.”

--With assistance from Harry Wilson.

To contact the reporters on this story: Viren Vaghela in London at vvaghela1@bloomberg.net;Steven Arons in Frankfurt at sarons@bloomberg.net

To contact the editors responsible for this story: Dale Crofts at dcrofts@bloomberg.net, Christian Baumgaertel

©2019 Bloomberg L.P.