The Year Australia’s Central Bank Was Dragged into QE Fold

The Year Australia’s Central Bank Was Dragged into the QE Fold

(Bloomberg) --

As the coronavirus ricocheted from China through South Korea, Iran and Italy in late February, Reserve Bank of Australia Chief Philip Lowe knew his economy wouldn’t be spared.

“I thought, gee, if that was happening in three such diverse economies at the same time, this is going to be a global problem,” Lowe recounted a couple of weeks ago. “I remember talking a lot with the treasurer that evening about the potential implications of this and I said, ‘This is going to come to Australia and it’s going to be a very big deal’.”

So it proved. Within a month, Australia was locking down and the RBA was turning to tools it had never used before as its economy veered toward its first recession in almost 30 years.

In its final meeting of the year on Tuesday, the RBA kept its key interest rate and three-year yield target at 0.10%. Lowe said the jobless rate was still likely to be around 6% at the end of 2022 -- from 7% now -- and that the board would keep the size of its A$100 billion ($73.7 billion) bond purchase program “under review.” He reiterated that the bank was prepared to do more if needed.

The governor heads into 2021 having prepared the ground for the government and households to spend up big over the summer months, powering a domestic demand-led recovery.

But in the background is an increasingly worrying relationship breakdown with China, which takes around 35% of Australia’s exports. It has slapped tariffs on goods from Down Under, is refusing to take calls from ministers in Canberra, while gloating over alleged Australian war crimes. The RBA can’t do much about those China risks, so engineering a strong domestic economy becomes all the more important.

2020 Review

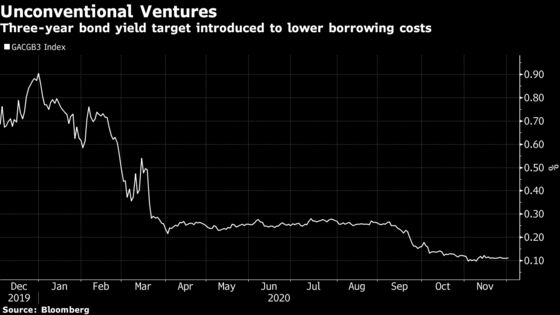

The RBA sprang into action on March 19, when it cut the cash rate to 0.25%, set up a lending facility for banks and established a three-year yield target of 0.25%. The yield control was geared to Australia, where most fixed-term borrowing has short horizons, but it also doubled as forward guidance, with the RBA saying rates wouldn’t rise for at least three years.

Globally, credit markets calmed in the weeks that followed and in Australia, the yield curve quickly fell into line with the RBA’s new guidance. The scale of Australia’s lockdown brought the government to the fore too. It abandoned a planned budget surplus and opened the fiscal spigots to support households and firms through the pandemic.

But as unemployment climbed, criticism of the RBA emerged for its failure to go even harder to help the government by pushing borrowing costs as low as possible -- or even negative.

“The Reserve Bank is way behind the curve in supporting the government in its budgetary funding measures,” former Prime Minister Paul Keating wrote in late September. “The RBA should return its eye to the Reserve Bank Act. Its job is to help the government meet the task of full employment. Price stability has been more than achieved.”

The RBA expanded a new lending facility to banks in September -- a move it tried to spin as a significant addition to its easing. Then it sat tight in October as the government announced a budget that sent deficit and debt to peacetime records.

In the meantime, a fresh wave of the virus had rocked Melbourne and forced the state of Victoria into a new lockdown. The RBA knew that lowering interest rates even further wouldn’t do much to unleash spending if people were physically banned from leaving their homes.

As the virus fog cleared with Melbourne’s lockdown proving effective in squashing the virus, it was time to act again.

In November, the bank cut its cash rate, three-year yield target and bank lending rate to 0.10% and announced a quantitative easing program over six months. The goal was to narrow the spread of Australia’s longer-term debt to that of global counterparts and contain a currency that had surged more than 25%.

So it was that in the eight months to November, a one-time rockstar economy that didn’t do recessions and didn’t need to buy bonds was now in its deepest slump since the Great Depression and running yield curve control and QE.

©2020 Bloomberg L.P.