The Worse Value Stocks Perform, the More Rob Arnott Likes Them

The Worse Value Stocks Perform, the More Rob Arnott Likes Them

(Bloomberg) -- Value stocks have been frustrating fans for a decade, testing their patience with year after year of subpar returns. But Rob Arnott says now is exactly the wrong time to bail on them.

In research published Wednesday, the Research Affiliates co-founder reiterates the case against quitting before the miracle. The 13-page paper, “Standing Alone Against the Crowd: Abandon Value? Now?!?” examines how the cheap-stock strategy has behaved over time, particularly after periods following severe underperformance. Arnott has stood by the strategy through years of struggle, and isn’t changing his stance now.

“We’re value investors, we see clients becoming uneasy,” Arnott said in a phone interview. “We owe it to our clients to remind them of an extremely basic fact, and that is when something is getting cheaper, its performance is disappointing. That doesn’t mean sell, it means buy.”

Arnott is occasionally called the “godfather” of smart-beta investing and his firm specializes in value strategies, so he’s not an unbiased commentator. And for better or worse, he’s talking his book. His RAFI Fundamental Index strategy -- which sorts under-priced stocks using weightings other than market-cap -- leans further into value when the strategy is “abnormally cheap,” as it is today.

Across U.S., developed, global, and emerging markets, value is trailing growth at a rate that falls within the worst decile in history, according to Research Affiliates. In the U.S., the disparity has only been larger twice before -- for a short period during the Global Financial Crisis and more than a year at the peak of the dot-com bubble, Arnott said.

While bad news if you’ve owned them, it’s a good setup for a recovery. Deeper underperformance often leads to a swifter rebound, and Arnott estimates current levels of relative valuation on average see value beat growth by 6% a year in the period that follows.

“A growth-dominated market over the past decade has served as a headwind and a gift in the form of a potential opportunity for the long-term contrarian investor,” Arnott and Research Affiliates’ Amie Ko and Jonathan Treussard write in the paper. “The RAFI strategy is positioned to experience a performance snapback when the cycle turns once again in favor of value investing and to recoup the accumulated shortfall in astonishing short order, achieving a swift and powerful recovery for the patient investor.”

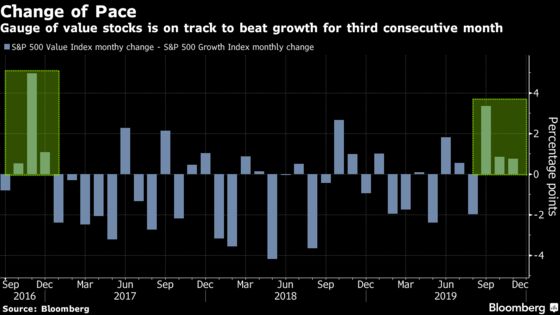

Lately, value has shown a few signs of life. As a proxy, the S&P 500 Value Index is on track to outpace its growth counterpart for the third straight month in November, a feat not seen since 2016. That’s left Wall Street shops including Bank of America Corp. and Sanford C. Bernstein advising a greater allocation to the style.

Even AQR Capital Management’s Cliff Asness, who’s spent his career warning against factor timing, wrote a paper this month arguing that investors should consider upping their holdings of value stocks.

Arnott says the style currently has healthy fundamentals and attractive qualities, including higher dividends and more tangible company sales for every dollar invested.

“If you’re getting a more profitable flow from these companies and they’re coming back into favor, then you get the best of all possible worlds,” Arnott said by phone. “A revaluation in a portfolio that’s already priced to give you a higher return, even if it doesn’t mean-revert.”

Still, even while AQR’s Asness has advised timing the value factor, the Research Affiliates team says that there’s a chance this time might not be any different than the past decade. “We can’t promise that tough times are behind us,” they write.

Arnott, Ko, and Treussard outline a cautionary tale. In March 2000, Julian Robertson, the famed investor who built Tiger Management into one of the world’s largest hedge funds, sent a letter to investors and closed his fund, lamenting that profits and price had taken a “back seat to mouse clicks and momentum.”

“He gave up on value at exactly the wrong time!” writes the Research Affiliates team. “Perhaps, similar to the new paradigm of the 1990s, things once again are not so very different this time.”

To contact the reporter on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.